-

July 2, 2026

-

BySteffy A

Foreign Exchange Transactions: Purpose and Scope of Form 15CA

Introduction

Foreign Exchange Transactions often involve payments to non-residents or foreign companies, making tax compliance an important part of the remittance process. Form 15CA is a declaration filed before making certain foreign remittances to ensure compliance with the applicable tax provisions. Under the Income-tax Act, 2025, Form 15CA has been renumbered renumbered as Form 145, while Form 15CB is renumbered as Form 146.

In this article, we explain the purpose and scope of Form 15CA, its applicability, the role of Form 15CB, the impact of DTAA, and the key filing requirements for foreign remittances.

Understanding Foreign Exchange Transactions

Foreign exchange transactions refer to cross-border transactions involving the exchange of one currency for another or payments between residents and non-residents. These include imports, exports, investments, professional services, royalties, education expenses, and other international remittances. In India, such transactions are regulated under FEMA, RBI regulations, and the Income-tax Act to ensure proper reporting, foreign exchange control, and tax compliance.

Such Foreign Exchange Transactions may also involve royalty payments, technical service fees, overseas investments, and other taxable remittances requiring reporting under the Income-tax Act.

What is Form 15CA?

Form 15CA is a declaration furnished by the remitter before making specified payments to a non-resident or a foreign company. It enables the Income-tax Department to collect information relating to foreign remittances and verify tax compliance.

What is the purpose of Form 15CA?

The primary purpose of Form 15CA is to furnish information regarding payments made to a non-resident (other than a company) or to a foreign company before the remittance is made. Form 15CA is filed by the person responsible for making the remittance for each applicable foreign payment. In specified cases, a Chartered Accountant’s certificate in Form 15CB is also required before filing Form 15CA.

It also helps the Income-tax Department monitor specified Foreign Exchange Transactions and verify that tax has been deducted wherever required under Section 195.

Confused about the difference between Form 15CA and Form 15CB? Read our detailed guide to understand when each form is required before making a foreign remittance.

What is the scope of Form 15CA?

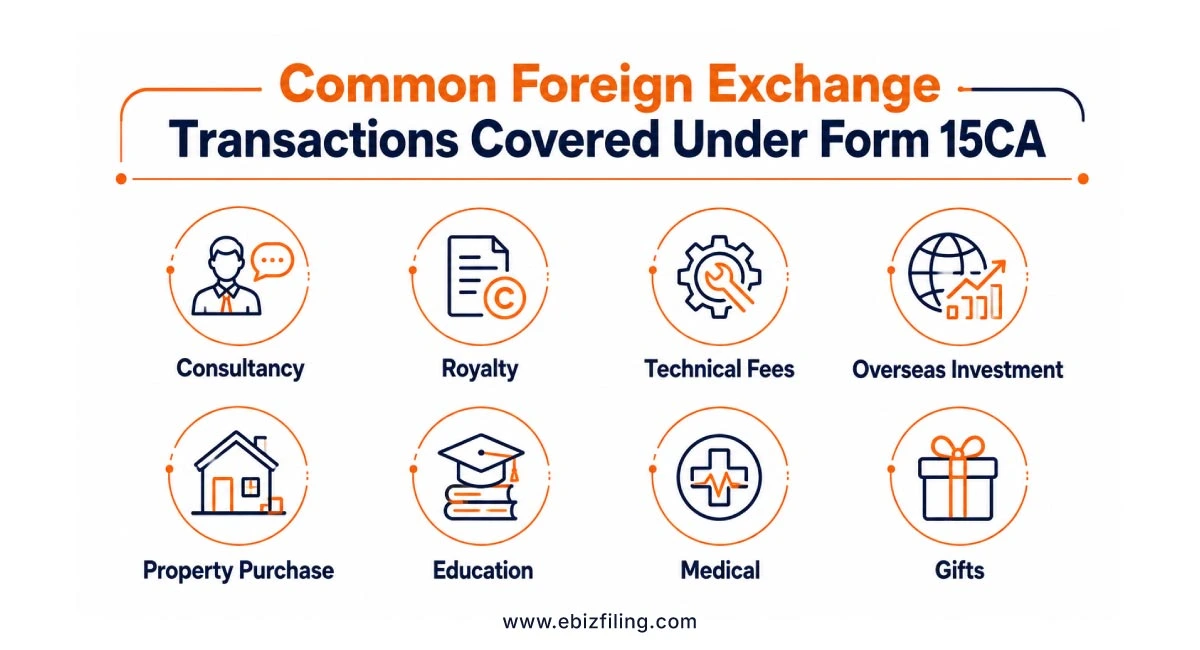

Form 15CA covers a wide range of Foreign Exchange Transactions, such as:

- Payments for the acquisition of foreign assets: Form 15CA may be required, depending on the taxability of the remittance and the applicable provisions of Rule 37BB.

- Business payments to non-residents: If a business makes payments to a non-resident, such as consultancy fees, technical services, or royalty, where the remittance is chargeable to tax and the applicable conditions under Rule 37BB are satisfied, Form 15CA is required to be furnished.

- Travel and education-related remittances: Certain overseas travel, medical treatment, maintenance of relatives abroad, or education-related remittances may require Form 15CA where applicable. However, many such transactions are specifically exempt under Rule 37BB.

- Gifts and donations to non-residents: Form 15CA may be applicable for certain gifts or donations made to non-residents, depending on the nature of the remittance and the applicable provisions.

|

Type of Foreign Remittance |

Is Form 15CA Generally Applicable? |

|

Professional or consultancy fees |

Yes, where applicable |

|

Royalty payments |

Yes |

| Technical service fees |

Yes |

|

Purchase of foreign assets |

Yes |

| Overseas investments |

Depends on the taxability of the remittance. |

|

Education remittances |

Generally exempt under prescribed conditions |

| Medical treatment abroad |

Generally exempt under prescribed conditions |

|

Gifts to non-residents |

Depends on the nature of remittance |

How does Section 195 apply to Foreign Exchange Transactions?

Section 195 of the Income-tax Act governs the deduction of tax at source (TDS) on payments made to a non-resident or a foreign company that are chargeable to tax in India. Before making such foreign remittances, the remitter must determine whether the payment is taxable and deduct tax at the applicable rate, wherever required. The applicability of Form 15CA is closely linked to these withholding tax provisions, as the form is used to report specified foreign remittances and ensure compliance with the prescribed tax requirements. In certain cases, a Chartered Accountant’s certificate in Form 15CB may also be required before filing Form 15CA.

To learn more about TDS provisions for payments made to non-residents in detail, read our guide on Section 195 of the Income-tax Act.

What is the DTAA Agreement and how does it relate to Form 15CA?

DTAA (Double Taxation Avoidance Agreement) helps prevent the same income from being taxed in both India and another country. The provisions of the applicable DTAA may affect the taxability of a foreign remittance and the tax to be deducted at source before making the payment.

Where a remitter claims the benefit of a DTAA, they may be eligible for a lower withholding tax rate or other applicable relief, subject to fulfilling the prescribed conditions. In such cases, documents such as a Tax Residency Certificate (TRC) and other prescribed declarations, wherever applicable, should be obtained and considered while filing Form 15CA.

Need Assistance with Form 15CA Filing?

Filing Form 15CA requires careful evaluation of the remittance, its taxability, and the applicable compliance requirements. Whether your payment requires only Form 15CA or both Form 15CA and Form 15CB, Ebizfiling can assist you throughout the process.

- Determine whether Form 15CA applies to your foreign remittance.

- Review the required documents before filing.

- Assist with Form 15CA filing and coordinate Form 15CB certification, wherever applicable.

- Help ensure timely filing to avoid delays in processing your foreign remittance.

- Provide support for business and individual foreign remittance compliance.

Need assistance with Form 15CA filing? Contact Ebizfiling today and let our experts help you complete your foreign remittance compliance accurately and on time.

Conclusion

Foreign Exchange Transactions involving payments to non-residents require compliance with the applicable tax and reporting provisions. Although Form 15CA is not required for every foreign remittance, it remains an important compliance requirement. Under the Income tax Act, 2025, Form 15CA and Form 15CB have been renumbered as Form 145 and Form 146, respectively. Understanding Rule 37BB, Section 195, and DTAA provisions helps ensure accurate and timely foreign remittance compliance.

Suggested Reads:

FEMA vs other foregin exchange transaction laws

US Stocks tax implications for Indian Investors

Frequently Asked Questions

1. Who is required to file Form 15CA for Foreign Exchange Transactions?

Any person responsible for making a specified payment to a non-resident or a foreign company may be required to file Form 15CA, depending on Rule 37BB and the taxability of the remittance.

2. Is it mandatory to submit Form 15CB?

Form 15CB is required only in specified cases, including where the remittance or aggregate of remittances exceeds ₹5 lakh during a financial year and the prescribed conditions under Rule 37BB are satisfied.

3. When is Form 15CA filing mandatory for Foreign Exchange Transactions?

Form 15CA filing becomes mandatory for specified Foreign Exchange Transactions where reporting is required under the Income-tax Act and Rule 37BB. Whether the declaration is required depends on the taxability of the remittance and the applicable compliance provisions.

4. What is the difference between Form 15CA and Form 15CB?

The main difference between Form 15CA and Form 15CB is that Form 15CA is a declaration submitted by the remitter, whereas Form 15CB is a certificate issued by a Chartered Accountant in specified cases to certify the taxability of the remittance and the applicable TDS provisions.

5. How does Rule 37BB determine Form 15CA applicability?

Rule 37BB specifies when Form 15CA applicability arises for foreign remittances and identifies the situations where Form 15CB is also required. It also provides a list of remittances that are exempt from furnishing these forms.

6. How does Section 195 apply to Foreign Exchange Transactions?

For taxable Foreign Exchange Transactions, Section 195 foreign remittance provisions require tax to be deducted at source on payments made to non-residents. These provisions also help determine whether Form 15CA must be filed before making the overseas remittance.

7. How do DTAA and Form 15CA work together for foreign remittances?

The relationship between DTAA and Form 15CA is important because an applicable tax treaty may allow a lower withholding tax rate on eligible foreign remittances. To claim treaty benefits, the remitter may also need documents such as a Tax Residency Certificate (TRC) and other prescribed declarations.

8. Which part of Form 15CA should be selected for a foreign remittance?

The correct part of Form 15CA depends on the nature and taxability of the remittance, whether Form 15CB is required, and whether any certificate or order has been obtained from the Income-tax Department. If you are unsure, Ebizfiling can help determine the correct reporting requirement before filing.

9. What documents are required for Form 15CA filing?

Before starting Form 15CA filing, keep details of the remitter and recipient, the purpose and amount of the remittance, supporting invoices or agreements, tax deduction details, and any applicable documents such as a TRC or Form 15CB. Ebizfiling can assist in reviewing these documents to help ensure a smooth filing process.

10. What has changed for Form 15CA under the Income-tax Act, 2025?

Under the Income-tax Act, 2025, Form 15CA has been renumbered as Form 145, while Form 15CB has been renumbered as Form 146. Although the form numbers have changed, the purpose of Form 15CA, the scope of Form 15CA, and the reporting requirements for specified Foreign Exchange Transactions continue under the new framework.

File your Form 15CA

Form 15 CA Online filing is necessary if you are making payments outside India to an Individual NRI or a Foreign Company.

About Ebizfiling -

Reviews

Akshay Sharma

18 Apr 2022I took a TM service for my Tea Brand, wonderful service with humble staff, and provided solutions on time. Recommended for all

Ashish Paliwal

29 Sep 2018Let me be honest and tell you that I did not choose eBiz filing after my initial LLP company registration did to pricing. A lot of companies contact me with better rates so I generally choose them. However, I will still rate eBiz filing 10/10 on work ethics. You guys are professionals in true sense.

John Mello

13 Mar 2018I am associated with Ebizfiling since a year now. And all my IT returns and GST returns are managed successfully by them. Really happy with the services.

July 8, 2026 By Steffy A

US Certificate of Good Standing: Why Your Company Needs It Introduction A US Certificate of Good Standing is an official document that confirms that a company registered in the United States is active and compliant with the applicable state requirements. […]

June 29, 2026 By Steffy A

Section 63 of the Income Tax Act 2025: Tax Audit Applicability Overview Section 63 of the Income-Tax Act, 2025 is the new provision governing tax audit requirements in India. It replaces Section 44AB of the Income Tax Act, 1961 and […]

June 24, 2026 By Steffy A

MCA Updates for Directors: Latest Compliance Requirements Overview MCA Updates for Directors play a key role in shaping how company directors in India stay compliant under the Ministry of Corporate Affairs (MCA) and the Companies Act, 2013. These updates come […]