-

June 30, 2026

-

BySteffy A

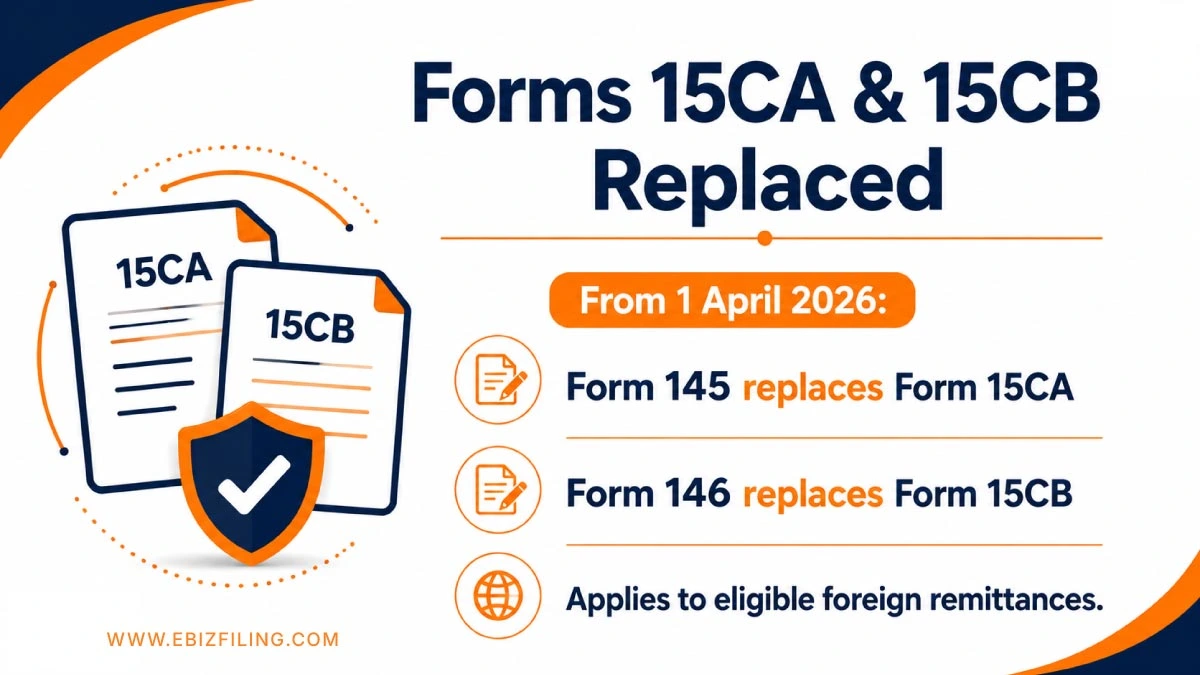

Form 145 and Form 146 Replace Forms 15CA and 15CB in 2026

Introduction to Form 145 and Form 146

Form 145 and Form 146 are the new compliance forms introduced under the Income-tax Act, 2025 for reporting foreign remittances from India. These forms became effective from 1 April 2026 and replaced the earlier Form 15CA and Form 15CB framework applicable to payments made to non-residents and foreign companies. The new forms continue the reporting requirements for foreign remittances under the Income-tax Act, 2025 and help taxpayers meet their tax compliance obligations.

This blog explains the applicability, filing requirements, key differences, and legal provisions related to Form 145 and Form 146.

Form 145 and Form 146 under Income Tax Act 2025

From 1st April 2026, the Income Tax Department has introduced a new framework under the Income tax Act 2025. As a result,

- Form 15CA has been replaced by Form 145,

- Form 15CB has been replaced by Form 146.

The objective remains the same: to ensure that taxes, where applicable, are properly deducted before money is remitted outside India.

If your business was filing Forms 15CA and 15CB before April 2026, you will now need to use Forms 145 and 146 for the same purpose. While the form numbers have changed, the responsibility to report foreign remittances and comply with tax regulations continues.

What is Form 145?

Form 145 is a mandatory declaration filed for making a payment to a non-resident or to a foreign company, before such remittance is made. It is governed by Sections 393, 395, 397, and 462 of the Income Tax Act, 2025 and Rule 220 of the Income Tax Rules, 2026.

The following table compares the form numbers, relevant provisions, and rules under the Income tax Act, 1961 and the Income tax Act, 2025.

|

Particulars |

As per the Income Tax Act, 1961 |

As per the Income Tax Act, 2025 |

|

Form Name |

15CA |

145 |

|

Relevant Provisions |

Sections 195(6), 271-I | Section 393, 395, 397, 462 |

| Relevant rule | 37BB of 1962 Rules |

220 of 2026 rules |

What is Form 146?

Form 146 is a certificate issued by a Chartered Accountant for payments made to a non-resident or a foreign company where the remittance is taxable and exceeds the prescribed threshold. It certifies the taxability of the remittance, applicable tax deduction, and compliance with the provisions of the Income tax Act, 2025 and relevant Double Taxation Avoidance Agreements (DTAA).

Form 146 is governed by Section 393 of the Income tax Act, 2025 and Rule 220 of the Income-tax Rules, 2026. It replaces the earlier Form 15CB and is generally required before filing Part C of Form 145 for eligible foreign remittances.

The following table compares the form numbers, relevant provisions, and rules under the Income tax Act, 1961 and the Income tax Act, 2025.

|

Particulars |

Income tax Act, 1961 |

Income tax Act, 2025 |

|

Form Name |

15CB | 146 |

| Relevant Provision | Section 195, 271J |

Section 393, 463 |

|

Relevant Rule |

Rule 37BB |

Rule 220 |

Form 145 and Form 146: Key Differences

|

Basis |

Form 145 |

Form 146 |

|

Purpose |

Declaration of foreign remittance to the Income Tax Department | Certification of taxability and TDS compliance for the remittance |

| Replaces | Form 15CA |

Form 15CB |

|

Filed By |

Remitter (person making the payment) | Chartered Accountant |

| Nature | Self-declaration |

Professional certificate |

|

Applicability |

Required for specified payments to non-residents or foreign companies | Required in specified taxable remittance cases, generally where CA certification is needed |

| Main Objective | Report foreign remittance details |

Verify taxability, TDS deduction, and DTAA applicability |

|

Contains |

Remittance details, payer details, recipient details, purpose of payment | Tax computation, DTAA analysis, TDS calculation, and compliance certification |

| Filing Responsibility | Business, individual, or company making the payment |

Practicing Chartered Accountant |

|

When Used |

Before making a foreign remittance | Before filing the applicable part of Form 145 where CA certification is required |

| Governing Rule | Rule 220 of the Income tax Rules, 2026 |

Rule 220 of the Income tax Rules, 2026 |

Form 145 is a declaration filed by the person sending money abroad, whereas Form 146 is a Chartered Accountant’s certificate that confirms the correct tax treatment of that remittance. Form 145 informs the Income Tax Department about the transaction, while Form 146 validates whether the applicable tax and DTAA provisions have been correctly considered before the funds are transferred.

Legal Provisions Governing Form 145 and Form 146

Forms 145 and 146 derive their legal authority from various provisions of the Income tax Act, 2025 and the Income-tax Rules, 2026. These provisions establish the framework for reporting foreign remittances, deducting tax at source, and ensuring compliance with cross-border payment regulations.

Section 393 of the Income tax Act, 2025

Section 393 governs tax deduction at source (TDS) on payments made to non-residents and foreign companies. Form 146 is closely associated with this provision, as it helps certify the taxability of the remittance and the applicable withholding tax obligations before the payment is made.

Section 395 of the Income tax Act, 2025

Under Section 395, the Assessing Officer may issue a certificate permitting a tax deduction at a lower rate or no deduction of tax in eligible cases. Where such a certificate is obtained, the relevant information is required to be reported in Form 145.

Section 397 of the Income tax Act, 2025

Section 397 empowers the Central Board of Direct Taxes (CBDT) to prescribe the manner and form for furnishing information relating to payments made to non-residents and foreign companies. Form 145 has been prescribed under this framework for reporting foreign remittances.

Section 462 of the Income tax Act, 2025

Section 462 explains penalty provisions relating to failures or inaccuracies in furnishing information required under the foreign remittance reporting framework. Taxpayers should therefore ensure that all information reported in Form 145 is accurate and complete.

Section 463 of the Income tax Act, 2025

Section 463 imposes penalties on accountants, merchant bankers, or registered valuers who furnish incorrect information in a report or certificate prescribed under the Act. Chartered Accountants may also be liable for penalties under this provision for furnishing incorrect information in Form 146 certifications.

Rule 220 of the Income-tax Rules, 2026

Rule 220 prescribes the procedure for furnishing information relating to foreign remittances. It specifies the circumstances in which different parts of Form 145 are applicable, the requirement for obtaining Form 146, and the process for filing these forms before remittance. The rule also prescribes reporting obligations for authorized dealers and certain IFSC units.

These provisions govern the reporting of foreign remittances, tax deduction requirements, and related compliance obligations under the Income tax Act, 2025.

Professional Support for Form 145 and Form 146 Compliance

Managing foreign remittance compliance involves more than simply filing forms. It requires understanding the taxability of payments, applying DTAA provisions correctly, obtaining Chartered Accountant certification where necessary, and ensuring that reporting requirements are completed before funds are remitted abroad.

How Can Ebizfiling Help?

- Assistance with determining the applicability of Form 145 and Form 146.

- Support for Form 145 filing and foreign remittance reporting.

- Coordination of Form 146 certification.

- Review of remittance-related documents and agreements.

- Guidance on TDS implications and DTAA benefits.

For professional assistance with Form 145 filing, Form 146 certification, and foreign remittance compliance, connect with Ebizfiling’s experts today.

For more details, read our guide on Major Renumbering of Income Tax Forms Explained.

Conclusion

The introduction of Form 145 and Form 146 has changed the foreign remittance reporting framework in India. These forms have replaced Forms 15CA and 15CB and continue to govern the reporting and certification requirements for payments made to non-residents and foreign companies. To ensure smooth compliance, businesses should review their remittance-related documentation, determine the correct tax treatment of payments, and obtain professional guidance wherever required. Proper preparation can help avoid reporting errors, delays, and compliance issues while making overseas payments.

Frequently Asked Questions

1. What is the due date for filing Form 145 and Form 146?

Form 145 is generally required to be filed before the remittance is processed through an authorized dealer bank. Where applicable, Form 146 certification should also be obtained before filing the relevant part of Form 145 and initiating the remittance.

2. Is Form 145 required for non-taxable foreign remittances?

The applicability of Form 145 depends on the nature of the remittance and the reporting requirements prescribed under Rule 220 of the Income-tax Rules, 2026. Taxpayers should verify whether Form 145 is required before making any payment to a non-resident or foreign company.

3. When is a Form 146 CA certificate required for a foreign remittance?

A Form 146 CA certificate is generally required when the remittance is taxable and exceeds ₹5 lakh during the tax year, unless a certificate from the Assessing Officer has been obtained under the relevant provisions of the Income tax Act, 2025.

4. Can Form 145 be filed without obtaining Form 146?

Yes, in certain cases. For taxable remittances up to ₹5 lakh, Form 145 may be filed without a Form 146 CA certificate. However, where the prescribed conditions require CA certification, Form 146 must be obtained before filing the relevant part of Form 145.

5. How does the Form 15CA replacement affect businesses making overseas payments?

The Form 15CA replacement mainly changes the reporting framework and form numbering under the Income tax Act, 2025. Businesses that previously filed Form 15CA must now use Form 145 while continuing to comply with foreign remittance reporting and TDS requirements.

6. Is Form 146 a complete replacement for Form 15CB?

Yes. Form 146 has replaced Form 15CB from 1 April 2026 and serves the same purpose of providing a Chartered Accountant’s certification for specified foreign remittance transactions.

7. Who is responsible for filing Form 145 and issuing Form 146?

Form 145 must be filed by the remitter, that is, the individual, business, or company making the payment to a non-resident or foreign company. Form 146, on the other hand, must be issued by a practicing Chartered Accountant who verifies the taxability of the remittance, applicable TDS provisions, and any DTAA benefits before the remittance is made.

8. What are the consequences of incorrect Form 145 and Form 146 compliance?

Failure to furnish Form 145 or furnishing inaccurate information may attract a penalty of up to ₹1 lakh under Section 462 of the Income tax Act, 2025. In addition, incorrect certifications under Form 146 may attract penalties under Section 463. Accurate compliance with Form 145 and Form 146 is therefore important for foreign remittance reporting and tax compliance.

9. How can Ebizfiling help with Form 145 and Form 146 compliance?

Ebizfiling assists businesses and individuals with Form 145 filing, Form 146 certification coordination, document review, and foreign remittance compliance support. Professional guidance can help ensure accurate reporting and timely completion of remittance-related obligations.

10. Why should businesses seek professional assistance for Form 145 foreign remittance compliance?

Foreign remittance transactions often involve taxability analysis, DTAA interpretation, TDS calculations, and documentation requirements. Ebizfiling helps taxpayers navigate these requirements and reduce the risk of filing errors, delays, and compliance issues associated with overseas payments.

Need Help with Business Tax Filing?

From preparing financial details to filing your return, we provide end-to-end support for business Income Tax Return filing.

About Ebizfiling -

July 23, 2026 By Steffy A

Section 202 of the Income Tax Act, 2025: Tax Slabs and Rules Introduction Section 202 of the Income Tax Act 2025 contains the provisions governing the new tax regime for individuals, Hindu Undivided Families, Associations of Persons, Bodies of Individuals, […]

July 22, 2026 By Steffy A

Section 332 of the Income Tax Act 2025: NPO Registration Introduction Section 332 of the Income Tax Act 2025 provides the registration framework for eligible non-profit organizations in India. It applies to public trusts, registered societies, Section 8 companies, universities, […]

July 21, 2026 By Steffy A

Section 201 of the Income Tax Act 2025: Tax Rate & Eligibility Introduction Section 201 of the Income Tax Act 2025 provides a concessional tax regime for eligible domestic manufacturing companies. It allows qualifying companies to pay income tax at […]