-

July 3, 2026

-

BySteffy A

Form 15CA and Form 15CB: Filing Process & Compliance

Overview

The Income Tax Department uses Forms 15CA and 15CB to monitor foreign remittances and make sure that any applicable taxes are appropriately withheld and declared prior to money transfers abroad. Form 15CB is a certificate given by a chartered accountant attesting to the remittance’s taxability and compliance with the Income Tax Act and DTAA regulations, whereas Form 15CA is a declaration made by the remitter. However, from 1st April 2026, these forms have been replaced by Form 145 and Form 146 under the new Income tax Act, 2025, bringing foreign remittance reporting under a revised compliance framework.

This blog will explain the difference between Form 15CA and Form 15CB, their applicability, filing requirements, and how to file Form 15CA and 15CB for smooth and compliant foreign remittances.

Difference Between Form 15CA and Form 15CB

Form 15CA

Form 15CA is a declaration form requiring information regarding payments to non-resident individuals or a foreign company to be furnished by persons making such payments before remitting the amount. Form 15CA is a declaration filed by the remitter providing details of the foreign remittance and confirming compliance with applicable tax provisions under the Income Tax Act.

Form 15CB

Form 15CB, however, is not a declaration, but a certificate issued by a Chartered Accountant ensuring that the provisions of the Double Taxation Avoidance Agreement and the Income Tax Act have been complied with in respect of tax deductions while making the payments. Form 15CB is a certificate issued by a Chartered Accountant that may be required for making payments to non-resident individuals and a foreign company when the amount is taxable and the aggregate payments exceed Rs. 5 lakhs in a financial year.

If you were previously filing Forms 15CA and 15CB for foreign remittances, you will now need to use Form 145 and Form 146, as the government has replaced the old forms under the Income-tax Act, 2025, from 1 April 2026.

Let’s Understand the key differences

|

Basis |

Form 15CA |

Form 15CB |

|

Meaning |

Form 15CA is a declaration filed by the remitter before making a payment to a non-resident or foreign company. |

Form 15CB is a certificate issued by a Chartered Accountant certifying the taxability of the remittance and compliance with tax laws. |

|

Purpose |

To provide information about foreign remittances to the Income Tax Department and ensure tax compliance. |

To certify the applicable tax liability, TDS deduction, and compliance with the Income Tax Act and DTAA provisions. |

|

Filed By |

The person making the remittance (remitter). |

A practicing Chartered Accountant (CA). |

|

Nature |

Self-declaration form. |

Professional certification. |

|

Requirement |

Required for specified foreign remittances made to non-residents. |

Required when the remittance is taxable and exceeds ₹5 lakh in a financial year, unless covered by specific exemptions or certificates. |

|

Contents |

Details of the remitter, remittee, amount, nature, and purpose of remittance. |

Details of the remittance, taxability, TDS rate, DTAA applicability, and compliance under Section 195 of the Income Tax Act. |

|

Role in Compliance |

Helps the Income Tax Department track foreign remittances. |

Helps determine the correct tax treatment before the remittance is made. |

|

Submission |

Filed online through the Income Tax e-Filing portal. |

Uploaded online by the Chartered Accountant before filing the applicable part of Form 15CA. |

In simple terms, Form 15CA is a declaration made by the remitter, whereas Form 15CB is a Chartered Accountant’s certificate that validates the tax implications of the remittance. While Form 15CA helps report foreign remittances to the Income Tax Department, Form 15CB ensures that the applicable tax and DTAA provisions have been correctly considered before the funds are transferred abroad.

Applicability and Requirements of Form 15CA and Form 15CB

Form 15CA and Form 15CB are required for certain foreign remittances made to non-residents or foreign companies under the Income Tax Act, 1961. The applicability of these forms depends on the taxability of the remittance, the amount being remitted, and whether any certificate has been obtained from the Assessing Officer.

Form 15CA is an online declaration filed by the remitter to report foreign remittances and ensure tax compliance.

Form 15CB is a certificate issued by a Chartered Accountant certifying the taxability of the remittance and compliance with the Income Tax Act and DTAA provisions.

How to Complete Form 15CA and Form 15CB Filing

Before filing, ensure you have the required documents, such as PAN, remittee details, purpose of remittance, supporting invoices or agreements, and Form 15CB (if applicable).

Obtain Form 15CB (If Required)

If the remittance is taxable and exceeds ₹5 lakh in a financial year, a Chartered Accountant must first issue and upload Form 15CB on the Income Tax e-Filing Portal. An Acknowledgement Receipt Number (ARN) is generated after successful filing.

Log in to the Income Tax e-Filing Portal

Visit www.incometax.gov.in and log in using your PAN and password.

Select Form 15CA

After logging in, go to the E-File section on the Income Tax e-Filing Portal. Select Income Tax Forms, click File Income Tax Forms, and choose Form 15CA from the available forms.

Choose the Applicable Part

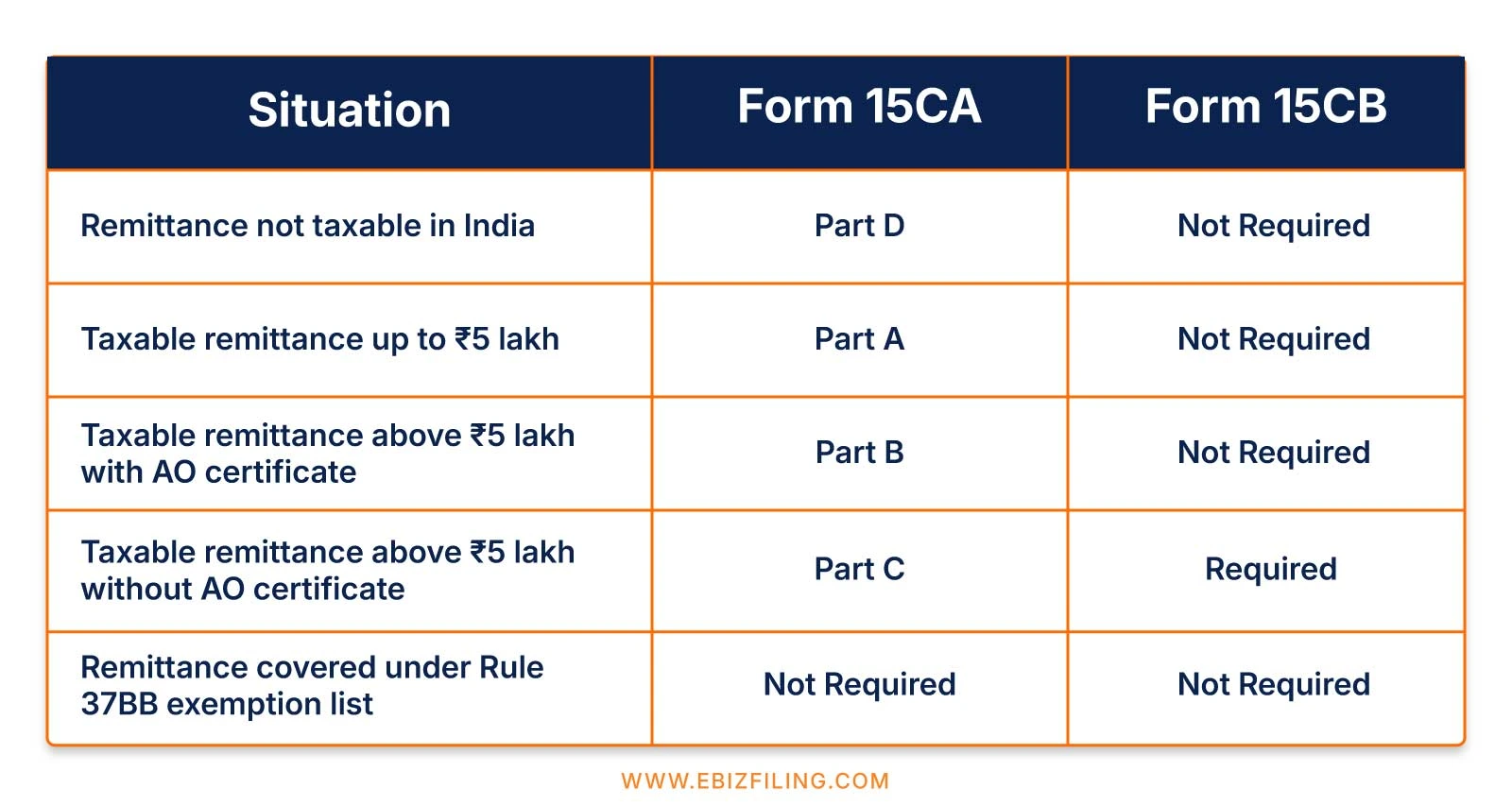

Select the relevant part of Form 15CA based on your remittance:

- Part A: Taxable remittance up to ₹5 lakh.

- Part B: Taxable remittance above ₹5 lakh with an Assessing Officer’s certificate.

- Part C: Taxable remittance above ₹5 lakh requiring Form 15CB.

- Part D: Remittance is not chargeable to tax in India.

Enter Remittance Details

Provide details of the remitter, remittee, remittance amount, purpose of payment, and tax information. For Part C, enter the ARN of the uploaded Form 15CB.

Verify and Submit

Review the information, e-verify the form using DSC or EVC, and submit it online. After successful submission, an acknowledgement number and transaction ID will be generated.

Submit Documents to the Bank

Provide the Form 15CA acknowledgement and Form 15CB (where applicable) to your authorized dealer bank for processing the foreign remittance.

This process ensures compliance with the Income Tax Act and helps facilitate smooth foreign remittances.

Want to understand the practical requirements, exemptions, and documentation involved in foreign remittances? Read our detailed guide on the Submission of Form 15CA and Form 15CB under the Income Tax Act.

How Ebizfiling Helps with Form 15CA and Form 15CB Compliance

If you are planning to make a payment to a non-resident or foreign company, ensuring compliance with Form 15CA and Form 15CB requirements is essential. Determining the taxability of a remittance, applying DTAA provisions, and completing the filing process accurately can be challenging without professional guidance.

To simplify the process, our experts assist with applicability checks, Chartered Accountant certification support, document verification, and end-to-end filing assistance for foreign remittances.

Conclusion

Form 15CA and Form 15CB are often required before making certain payments to non-residents or foreign companies. Before funds are transferred abroad, it is important to assess the applicable tax and compliance requirements. These forms help support the remittance process by providing the necessary reporting and certification, where required. By understanding their applicability and filing requirements, taxpayers can reduce the risk of delays, penalties, and last-minute issues with banks or tax authorities. Proper compliance at the time of remittance can save significant time and effort later.

Suggested Reads:

Frequently Asked Questions

1. Can Form 15CA and Form 15CB be revised after submission?

If an error is identified after filing, the remitter may withdraw or refile Form 15CA subject to the procedures available on the Income Tax e-Filing Portal. If there is any change in taxability or remittance details, a revised Form 15CB may also be issued by the Chartered Accountant before the remittance is processed.

2. Are Form 15CA and Form 15CB required for all overseas payments?

Certain remittances specified under Rule 37BB and transactions not chargeable to tax in India may not require Form 15CA or Form 15CB. The applicability depends on the nature of the remittance, taxability, and prescribed exemptions.

3. Can a bank process a foreign remittance without Form 15CA?

Authorized dealer banks generally require proof of compliance before processing certain foreign remittances. If Form 15CA applies to the transaction, the bank may ask for the Form 15CA acknowledgement and, where required, the Form 15CB certificate before releasing the payment.

4. Which part of Form 15CA should be selected while filing?

The applicable part depends on the nature and value of the remittance. Part A applies to taxable remittances up to ₹5 lakh, Part B applies where an Assessing Officer’s certificate is obtained, Part C applies when Form 15CB is required, and Part D applies to remittances that are not chargeable to tax in India.

5. Can Form 15CA be filed without Form 15CB?

Yes. Income Tax Form 15CA can be filed without Form 15CB in cases where the remittance is not taxable, falls under exempt categories, or does not require a Chartered Accountant’s certification under the applicable provisions.

6. What details are required for the Form 15CA filing process?

The Form 15CA filing process requires details such as the remitter’s PAN, remittee information, remittance amount, purpose of remittance, country of payment, tax deduction details, and supporting documents like invoices or agreements.

7. What happens if Form 15CA and Form 15CB are not filed when required?

Failure to file Form 15CA and Form 15CB when applicable may result in penalties under the Income Tax Act, delays in foreign remittance processing, and compliance issues during tax assessments or audits. Failure to furnish Form 15CA when required may attract a penalty of ₹1,00,000 under Section 271-I of the Income Tax Act. It may also lead to delays in processing foreign remittances.

8. Is Form 15CA required for payments made to foreign freelancers or consultants?

Yes. If the payment is made to a foreign freelancer, consultant, or service provider and is taxable under Indian tax laws, Income Tax Form 15CA may be required before the remittance is processed. The requirement for Form 15CB will depend on the amount and taxability of the payment.

9. How can Ebizfiling help with Form 15CA and Form 15CB compliance?

Ebizfiling assists individuals and businesses with the complete Form 15CA and Form 15CB compliance process, including applicability assessment, taxability review, Chartered Accountant certification support, document verification, and online filing assistance for foreign remittances.

10. Can Ebizfiling assist with obtaining a Form 15CB certificate?

Yes. Ebizfiling assists individuals and businesses in obtaining a Form 15CB certificate through qualified Chartered Accountants. Our team helps review remittance details, assess taxability, gather documentation, and coordinate the certification process to ensure compliance with foreign remittance regulations.

File Form 15CA Online with Expert Assistance

Simplify your overseas remittance compliance with professional Form 15CA online filing services and expert guidance.

About Ebizfiling -

July 20, 2026 By Steffy A

Top 5 Finance influencers in India Introduction Financial literacy matters more today than it ever has. With markets, taxes, and investment options growing more complex by the year, people are increasingly turning to digital platforms for guidance they can actually […]

July 18, 2026 By Steffy A

Independent Director in India: Eligibility and Registration Process Overview Becoming an independent director in India is increasingly recognized as a professional opportunity in corporate governance. Experienced professionals can use their knowledge to contribute to Board-level discussions, business strategy, risk management, […]

July 20, 2026 By Steffy A

PF and ESI Compliance Calendar August 2026: Key Due Dates Introduction The PF and ESI Compliance Calendar August 2026 provides employers with the key statutory due dates for depositing PF and ESI contributions relating to July 2026. Adhering to these […]