-

July 4, 2026

-

BySteffy A

Form 123 under the Income Tax Act 2025: Form 123 vs Form 12BA

Overview

Form 123 under the Income Tax Act 2025 is the statement employers issue to report taxable perquisites and other salary-related benefits provided to employees. It replaces the earlier Form 12BA under the Income-tax Act, 1961 while continuing the same reporting purpose under the new law. This blog explains who needs Form 123, when employers must issue it, what details it contains, and how it differs from the earlier Form 12BA.

What is Form 123 under the Income Tax Act 2025?

Form 123 is a statutory statement issued by employers to eligible employees for reporting taxable perquisites, fringe benefits, and profits in lieu of salary. Although the form number has changed under the Income-tax Act, 2025, its purpose remains largely the same as the earlier Form 12BA of Income Tax. Employers are required to issue Form 123 only where an employee’s annual salary exceeds ₹1,50,000, as prescribed under the Income-tax Rules.

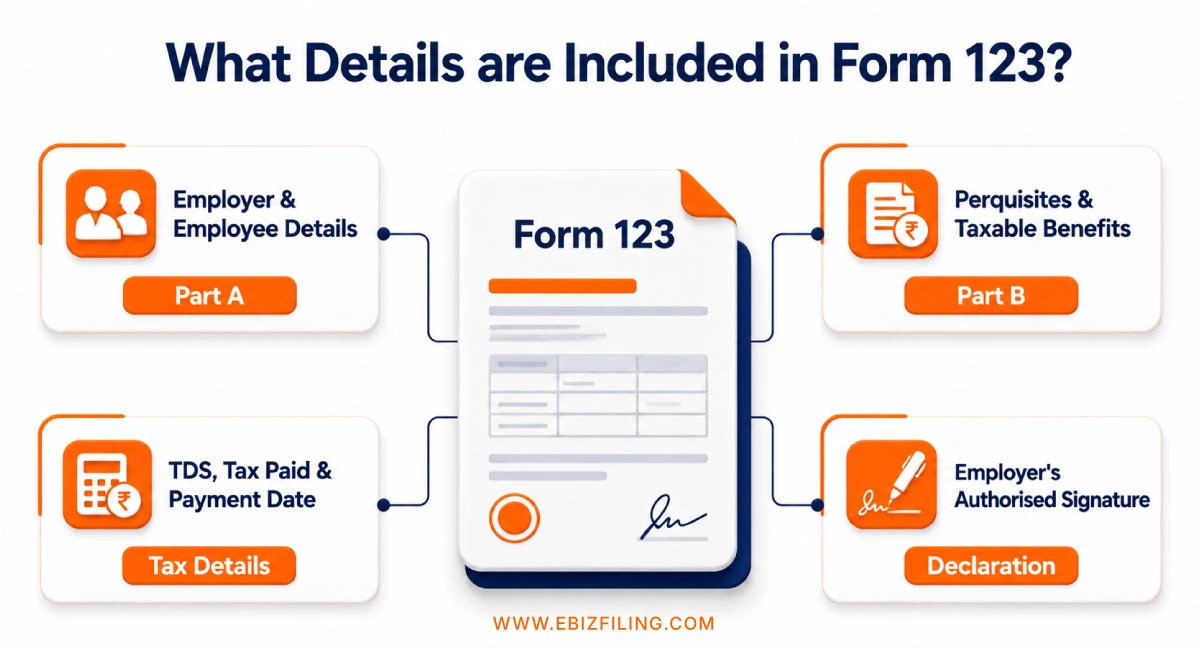

What Details are Included in Form 123 of Income Tax Act?

Form 123 under the Income Tax Act 2025 consists of two parts: Part A and Part B. Together, these sections provide information about the employer, employee, perquisites provided during the tax year, and the related tax deducted at source (TDS). At the end of Form 123, the employer signs a declaration confirming that all information provided in the form is accurate and complete.

Part A: Employer and Employee Details

Part A captures the basic information of both the employer and the employee.

Employer details include:

- Name

- Address

- PAN

- TAN

- Contact details

Employee details include:

- Name

- Designation

- PAN

- Type of employee (Director or person having substantial interest, where applicable)

- Income from salary other than perquisites

- Contact details

Part B: Valuation of Perquisites

Part B provides a detailed valuation of the perquisites, fringe benefits, amenities, and profits in lieu of salary provided by the employer. The value of each perquisite is determined in accordance with the prescribed Income tax Rules and is considered for computing the employee’s taxable salary.

Details of Perquisites and Tax Information

Form 123 under the Income Tax Act 2025 contains the particulars of various perquisites, including:

- Accommodation

- Cars or other automotive facilities

- Sweeper, gardener, watchman, or personal attendant

- Gas, electricity, and water

- Interest-free or concessional loans

- Holiday expenses

- Free or concessional travel

- Free meals

- Free education

- Gifts and vouchers

- Credit card expenses

- Club expenses

- Use or transfer of movable assets

- Other benefits, amenities, or privileges

- Eligible start-up ESOPs and other stock options

- Employer’s contribution to specified funds or schemes

- Annual accretion by way of interest, dividend, or similar income

- Other taxable benefits or amenities

For each perquisite, the form specifies:

- Nature of the perquisite

- Value of the perquisite as per the rules

- Amount recovered from the employee, if any

- Amount chargeable to tax

It also includes details relating to tax deducted from salary, tax paid by the employer on behalf of the employee, total tax paid, and the date of payment into the Central Government account.

For the complete format and contents of the form, refer to the official Form No. 123 PDF issued by the Income Tax Department.

Employer Declaration

The form concludes with a declaration by the employer certifying that the particulars furnished in Form 123 are true and complete. The declaration must be signed by the authorised person responsible for issuing the form.

Key Differences Between Form 123 and Form 12BA

The biggest change is the renumbering of the form under the new Income tax Act, 2025. Apart from updated section numbers, rule references, and the form number itself, the reporting requirements and due date continue without any major change.

|

Particular |

Form 12BA |

Form 123 |

|

Governing Act |

Income tax Act, 1961 |

Income tax Act, 2025 |

|

Form Number |

12BA |

123 |

|

Relevant Section |

Section 192 |

Section 392(5)(a) |

|

Relevant Rule |

Rule 26A |

Rule 204(2) |

|

Purpose |

Statement of Perquisites |

Statement of Perquisites |

|

Due Date |

30 April |

30 April |

What are the Due Date and Filing Requirements for Form 123?

Employers must issue Form 123 under the Income Tax Act 2025 within the prescribed time limit and in accordance with the applicable Income tax Rules. Issuing the form on time allows employees to verify their taxable perquisites and report their salary income correctly while filing their Income Tax Return (ITR).

Due Date of Form 123 under the Income Tax Act

Form No. 123 must be issued to the employee on or before 30 April of the year following the relevant tax year.

Form No. 123 may be issued either manually or digitally, depending on the facility provided by the employer. It must be signed by the same person who is authorised to sign Form 130.

Filing Requirements of Form 123 under the Income Tax Act

- Form 123 is required to be issued only where applicable under the Income-tax Rules.

- It is issued in addition to Form 130 and does not replace the TDS certificate.

- If an error is identified after issuance, the employer may issue a revised Form 123.

Form 123 is not required to be attached or uploaded with the Income Tax Return (ITR). However, employees should preserve it for their records.

Issuing Form 123 under the Income Tax Act 2025 within the prescribed due date enables employees to verify the value of taxable perquisites, reconcile salary-related tax deductions, and accurately report salary income while filing their Income Tax Return. It also helps employers meet their statutory compliance requirements under the Income tax Act, 2025.

Professional Compliance Support from Ebizfiling

Ebizfiling simplifies tax and regulatory compliance by helping businesses understand legal requirements and complete their statutory obligations on time.

- Our team also supports TDS returns, payroll tax compliance, and correction filings.

- We help companies complete ROC and LLP compliance requirements on time.

- Clients receive timely updates on important tax and regulatory changes.

- Practical compliance guidance is available whenever additional support is required.

Businesses can obtain expert assistance with Business Income Tax Return Filing to ensure accurate filing and timely compliance.

Conclusion

Form 123 under the Income Tax Act 2025 replaces the earlier Form 12BA while continuing to serve the same purpose of reporting taxable perquisites and other salary-related benefits provided by employers. Where applicable, employers should issue Form 123 within the prescribed timeline so employees can correctly report their salary-related tax details and maintain proper tax records. Employees should keep a copy of Form 123 even after filing their Income Tax Return, as it can help verify salary-related tax details whenever required.

Suggested Reads:

Frequently Asked Questions

1. When is Form 123 under the Income Tax Act 2025 not required to be issued?

Form 123 is issued only where required under the Income-tax Rules. Employers should check whether the prescribed conditions apply before issuing the form.

2. Why is Form 123 issued even if Form 130 has already been provided?

Form 123 of Income Tax and Form 130 serve different purposes. While Form 130 is the TDS certificate, Form 123 statement of perquisites reports the valuation of taxable perquisites, fringe benefits, and other salary-related benefits. Therefore, Form 123 is issued in addition to Form 130.

3. Can employers issue Form 123 in electronic format?

Form 123 under the Income Tax Act, 2025 may be issued either manually or electronically, depending on the employer’s internal process. It must be signed by the authorised person who is also responsible for signing Form 130.

4. What should an employer do if incorrect details are reported in Form 123?

If any information in Form 123 filing is found to be incorrect after issuance, the employer may issue a revised Form 123 containing the corrected particulars.

5. Should employees keep Form 123 after filing their Income Tax Return?

Although Form 123 under the Income Tax Act 2025 is not required to be attached with the Income Tax Return, employees should preserve it for future reference and tax records.

6. Has anything changed apart from Form 123 replacing Form 12BA?

Besides the fact that Form 123 replaces Form 12BA, the corresponding section, rule number, and statutory references have also been updated under the Income-tax Act, 2025 and the Income-tax Rules, 2026. However, the purpose of the form remains the same.

7. Does Form 123 continue to apply if an employee opts for the new tax regime?

Yes. Form 123 under the Income Tax Act 2025 continues to apply under the new tax regime because taxable perquisites continue to be reportable wherever applicable.

8. Does Form 123 include only cash benefits received from an employer?

Form 123 statement of perquisites covers both monetary and non-monetary benefits, including accommodation, motor cars, concessional loans, ESOPs, gifts, employer contributions to specified funds, and other taxable amenities.

9. Where can businesses get professional assistance with employer tax compliances?

Businesses can seek professional assistance from Ebizfiling for payroll compliance, TDS returns, ITR filing, ROC compliance, and other statutory requirements.

10. How does Ebizfiling help businesses stay updated with changes under the Income-tax Act, 2025?

Ebizfiling regularly publishes practical updates on changes such as Form 123 replaces Form 12BA and assists businesses with income tax, TDS, company law, and other regulatory compliances to help them stay compliant with the latest legal requirements.

Need a Professional Employee Handbook?

A well-drafted Employee Handbook helps businesses maintain consistency, improve employee awareness, and support statutory compliance.

About Ebizfiling -

July 23, 2026 By Steffy A

Section 202 of the Income Tax Act, 2025: Tax Slabs and Rules Introduction Section 202 of the Income Tax Act 2025 contains the provisions governing the new tax regime for individuals, Hindu Undivided Families, Associations of Persons, Bodies of Individuals, […]

July 22, 2026 By Steffy A

Section 332 of the Income Tax Act 2025: NPO Registration Introduction Section 332 of the Income Tax Act 2025 provides the registration framework for eligible non-profit organizations in India. It applies to public trusts, registered societies, Section 8 companies, universities, […]

July 21, 2026 By Steffy A

Section 201 of the Income Tax Act 2025: Tax Rate & Eligibility Introduction Section 201 of the Income Tax Act 2025 provides a concessional tax regime for eligible domestic manufacturing companies. It allows qualifying companies to pay income tax at […]