-

July 4, 2026

-

BySteffy A

Form 12BA of The Income Tax : Applicability and Structure

Introduction

Form 12BA of the Income Tax is issued under the income tax laws, which have established guidelines for the assessment of certain perquisites. Additionally, because Form 16 only contains a consolidated account of the pay and benefits an employee receives from their employer, income tax regulations mandate the issuance of separate statements outlining all of the individual’s perquisites. Form 12BA has been renumbered as Form No. 123 under the Income tax Act, 2025.

This article focuses on “What is Form 12BA of the Income Tax?”, the applicability of Form 12BA, the structure of Form 12BA of the Income Tax Act, and FAQs on Form 12BA.

What is Form 12BA of the Income Tax?

Form 12BA is an Income Tax statement that lists the details of perquisites, amenities provided by the employer, profits in lieu of salary, and other fringe benefits. Form 12BA shows the taxable value of the perquisites provided by the employer. It also helps calculate the tax payable on these benefits. Along with Form 16, Form 12BA is also required to be provided by the employer to the employee.

Note: With effect from 1 April 2026, Form 12BA has been renumbered as Form 123 under the Income tax Act, 2025.

Perquisites for Form 12BA of the Income Tax Act

Perquisites, often known as perks, are a type of additional compensation or benefit provided to an employee in exchange for services rendered to an employer. The following categories of these benefits include, which are provided in addition to the regular salary:

Certain monetary benefits and non-monetary benefits provided by the employer may be treated as taxable perquisites depending on the applicable provisions.

Non-cash incentives include rent-free or concessional accommodation, employee stock options, free meals and water, gift cards, restricted stock units, a car, and other benefits in kind.

Structure of Form 12BA of the Income Tax Act

Form No. 123 is divided into two parts. The details included in each part are as follows:

Part A: Employer and Employee Details

Employer Details

- Name and Address

- PAN

- TAN

- Contact details

Employee Details

- Name

- Designation

- PAN

- Type of Employee (where applicable)

- Income from Salary (excluding perquisites)

- Contact details

Part B: Perquisites and Tax Details

Perquisites Information

- Nature of Perquisites

- Value of Perquisites

- Amount Recovered from the Employee (if any)

- Taxable Value of Perquisites

- Profits in Lieu of Salary

Tax Details

- Tax Deducted at Source (TDS)

- Tax Paid by the Employer on Behalf of the Employee

- Total Tax Paid

- Details of Tax Deposited with the Central Government

The above structure is based on the latest Form No. 123 (earlier Form 12BA) prescribed under the Income tax Act, 2025 and is applicable from 1 April 2026.

For the complete format and contents of the form, refer to the official Form No. 123 PDF issued by the Income Tax Department.

Applicability of Form 12BA of the Income Tax Act

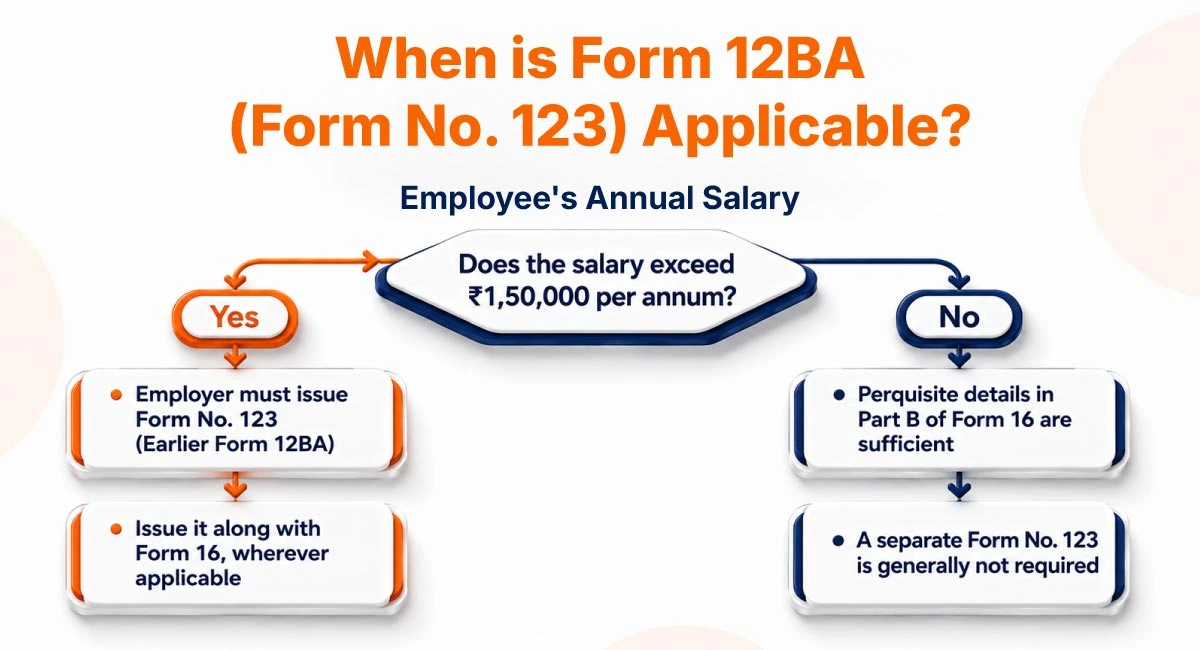

When the salary paid or payable to an employee exceeds ₹1,50,000 per annum, Form 12BA is required to be issued. It is not necessary to issue a separate statement in the form of Form 12BA if the remuneration is less than INR 150,000. Instead, the information on perquisites already included in Part B of Form 16 is sufficient.

Information included in Form 12BA: Wages, bonuses, commissions, and any other financial compensation received from one or more employers.

Information not included in Form 12BA: Lump-sum payments received at the time of termination of service, superannuation, or voluntary retirement, such as gratuity, severance pay, leave encashment, and voluntary retrenchment benefits. Dearness allowance that is not included in the calculation of the superannuation or retirement benefits of the concerned employee.

Where applicable, employers should issue the prescribed statement in accordance with the Income-tax provisions and the prescribed form requirements. In Form 12BA, the employer may state that the employee has not received any perquisites.

Difference Between Form 12B and Form 12BA

Although Form 12B and Form 12BA of the Income Tax serve different purposes, they are often confused because both relate to salary and tax compliance. The table below highlights the key differences between the two.

|

Particulars |

Form 12B |

Form 12BA |

|

Purpose |

To declare salary income and TDS details from a previous employer. |

To provide details of taxable perquisites and profits in lieu of salary. |

|

Issued/Furnished By |

Employee |

Employer |

|

Issued/Furnished To |

New Employer |

Employee |

|

When Applicable |

When an employee joins a new employer during the financial year. |

Where applicable, along with Form 16 for reporting taxable perquisites. |

|

Key Information |

Previous employment income and TDS deducted. |

Employee details, employer details, perquisites, and tax deduction details. |

Form 12BA Compliance Support by Ebizfiling

Managing employer tax compliance involves more than issuing Form 12BA. Ebizfiling provides end-to-end assistance to help businesses meet their salary-related tax obligations.

Our services include:

- TDS Return Filing to ensure timely and accurate tax compliance.

- Form 16 Compliance for proper salary and tax reporting.

- Payroll Compliance to manage employee tax records and statutory requirements.

- Income Tax Compliance to help businesses comply with applicable tax provisions.

With a team of experienced professionals, Ebizfiling helps employers maintain accurate records, reduce compliance risks, and meet statutory deadlines efficiently.

Conclusion

Form 12BA of the Income Tax serves as an important statement for reporting taxable perquisites and other salary-related benefits provided to employees. Employers should determine its applicability, report perquisites accurately, and issue the form along with Form 16 wherever required. As Form 12BA has been renumbered as Form No. 123 with effect from 1 April 2026, employers should also ensure compliance with the updated provisions while fulfilling their tax reporting obligations.

FAQs on Form 12BA of the Income Tax

1. What information is required in Form No. 123 (Earlier Form 12BA)?

Form No. 123 includes employer and employee details, salary information, details and valuation of taxable perquisites, profits in lieu of salary, TDS details, and tax payment information. It helps ensure accurate reporting of employee benefits for tax purposes.

2. Is Form 12BA still applicable after the introduction of Form No. 123?

Yes. With effect from 1 April 2026, Form 12BA has been renumbered as Form No. 123 under the Income tax Act, 2025. While the form number has changed, its purpose of reporting taxable perquisites and profits in lieu of salary continues under the new format.

3. Can Form 12BA be revised after it has been issued?

Yes. If any error is identified after issuing Form 12BA, the employer should correct the records and provide an updated statement wherever required.

4. What is the difference between Form 12BA and Form 16?

Form 16 is a certificate showing salary paid and TDS deducted by the employer, whereas Form 12BA of the Income Taxprovides detailed information on taxable perquisites and profits in lieu of salary. Where applicable, both documents are issued together.

5. What are taxable perquisites under Section 17(2)?

Taxable perquisites under Section 17(2) include specified benefits provided by an employer, such as accommodation, motor car facilities, concessional loans, gifts, ESOPs, employer-paid obligations, and other prescribed benefits. Their value is reported in Form No. 123, wherever applicable.

6. How can I download Form 12BA (Form No. 123)?

The latest Form No. 123 (Earlier Form 12BA) can be downloaded from the official Income Tax Department website. Employers should always use the latest prescribed format while preparing the statement.

7. Can an employee use Form 12BA while filing an Income Tax Return?

Yes. Although Form 12BA is not filed separately with the Income Tax Return, it helps employees understand the valuation of taxable perquisites and verify salary-related information while preparing their return.

8. Is Form 12BA required if an employee receives no taxable perquisites?

If an employee does not receive any taxable perquisites, employers should verify whether issuing Form No.123 is required under the applicable Income-tax provisions.

Ebizfiling can help businesses with employer tax compliance and salary-related reporting.

9. What should employers keep in mind while preparing Form 12BA?

Employers should ensure that taxable perquisites are correctly valued, salary details are accurate, and TDS information matches payroll records before issuing the statement. Businesses seeking professional support for TDS Return Filing, Form 16 compliance, and employer tax compliance can also consult Ebizfiling for end-to-end assistance.

10. Where can employers get assistance with Form 12BA compliance?

Employers should ensure that Form 12BA (Form No. 123) is prepared accurately and issued in accordance with the applicable Income-tax provisions. Ebizfiling assists businesses with TDS Return Filing, Form 16 compliance, payroll compliance, and employer tax compliance, helping them maintain accurate records and meet statutory requirements efficiently.

TDS Returns Filing

Quickly file error-free TDS Returns with EbizFiling. This ensures seamless credit to the deductee.

About Ebizfiling -

Reviews

Deepika Khan

29 Sep 2018I would rate 5/5 for their services, pricing and transparency.

Jaydipkumar Babriya

18 Apr 2022Excellent service with a high level of professionalism. They not only applied for trademark, got it registered but also provided guidance and advisory thereof. That's amazing experience!! Really deserve 5 out of 5!!

Mamta Tanna

20 Dec 2017More power to the Ebizfiling team for being so generous and systematic in the whole process of ESIC registration.

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]