-

June 29, 2026

-

BySteffy A

Section 63 of the Income Tax Act 2025: Tax Audit Applicability

Overview

Section 63 of the Income-Tax Act, 2025 is the new provision governing tax audit requirements in India. It replaces Section 44AB of the Income Tax Act, 1961 and specifies when businesses and professionals must get their accounts audited. Understanding tax audit applicability, turnover limits, and compliance requirements under Section 63 is essential to avoid penalties and ensure accurate tax reporting.

In this blog, we’ll explore Section 63 vs Section 44AB, the key changes, and who needs to comply with the tax audit provisions in 2025.

Tax Audit Under Section 63 of the Income-Tax Act, 2025

Section 63 of the Income-Tax Act, 2025 contains the provisions governing tax audits for specified businesses and professionals. The section requires eligible taxpayers to get their accounts audited by an accountant before the specified date if the prescribed turnover, gross receipt, or presumptive taxation conditions are met.

Section 63 succeeds Section 44AB of the Income Tax Act, 1961 as part of the legislative restructuring introduced under the Income-Tax Act, 2025.

Although the section has been restructured under the new Act, the underlying tax audit requirements continue to apply in much the same way as before. It continues to mandate tax audits for businesses and professionals crossing the prescribed thresholds and helps the tax authorities verify the accuracy of income reported by taxpayers.

Taxpayers opting for a Presumptive Taxation Scheme should carefully review the conditions under which a tax audit may still become applicable.

Section 63 vs Section 44AB: Key Differences

The tax audit provisions previously contained in Section 44AB have now been incorporated into Section 63 of the Income-Tax Act, 2025. While the section has been reorganized under the new legislation, its primary objective remains the same: ensuring that eligible businesses and professionals maintain accurate financial records and comply with tax laws.

Although Section 63 substantially retains the framework contained in Section 44AB, certain structural changes have been introduced. The key differences are as follows:

|

Particulars |

Section 63 of the Income Tax Act, 2025 |

Section 44AB of the Income Tax Act, 1961 |

|

Governing Legislation |

Income-Tax Act, 2025 |

Income Tax Act, 1961 |

|

Section Number |

Section 63 | Section 44AB |

| Drafting Structure | Presented in a simplified and tabular format |

Drafted through multiple clauses and sub-clauses |

|

Presumptive Taxation References |

Sections 58(2) and 61(2) | Sections 44AD, 44ADA, and related provisions |

| Audit Trigger Framework | Consolidated under a structured table |

Contained in separate clauses |

|

Business Audit Threshold |

₹1 crore, extendable to ₹10 crore subject to prescribed conditions | ₹1 crore, extendable to ₹10 crore subject to prescribed conditions |

| Professional Audit Threshold | ₹50 lakh |

₹50 lakh |

|

Compliance Objective |

Ensuring transparency and tax compliance through audited accounts |

Ensuring transparency and tax compliance through audited accounts |

While the turnover thresholds and audit requirements remain largely unchanged, Section 63 adopts a more streamlined legislative approach. While the audit requirements have not changed significantly, taxpayers should become familiar with the new section references under the Income Tax Act, 2025.

Applicability of Section 63 of the Income-Tax Act, 2025

1. Tax Audit Requirement for Businesses Under Section 63(1)(a)

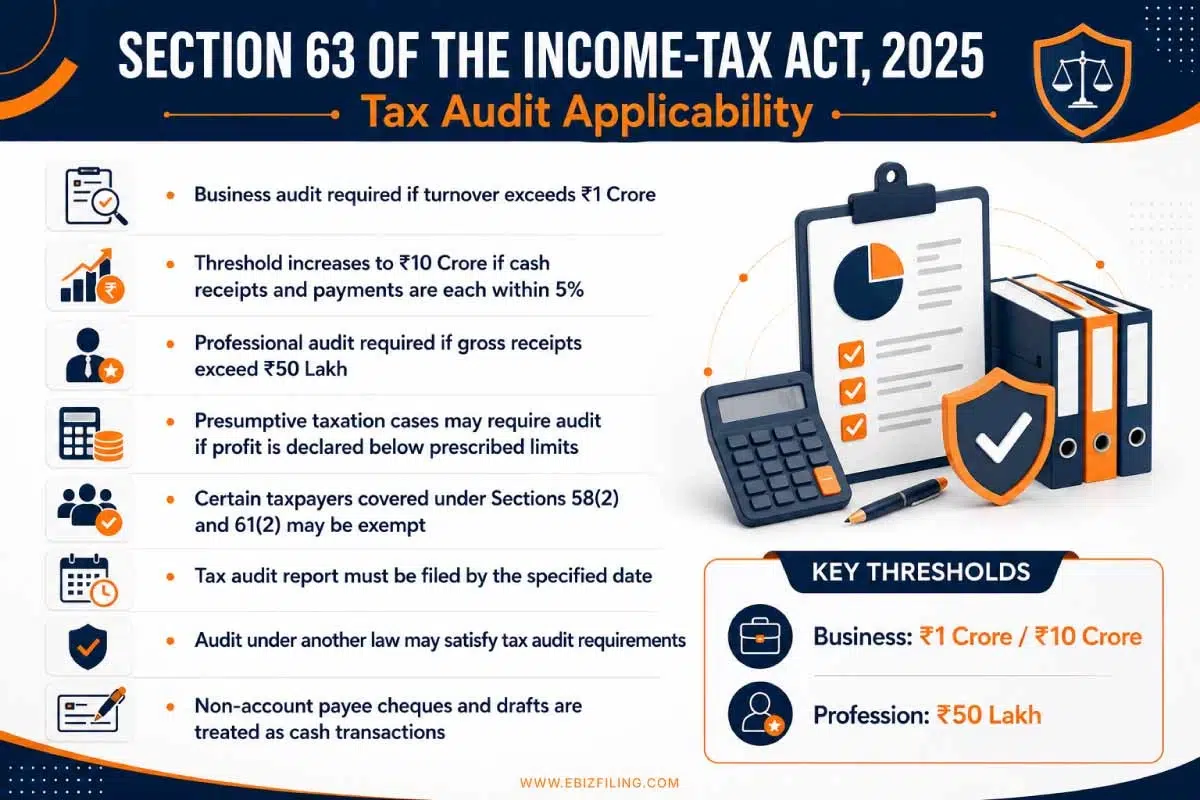

A person carrying on business is required to undergo a tax audit if the total sales, turnover, or gross receipts from the business exceed ₹1 crore in a tax year, subject to the conditions specified under Section 63(1)(b).

2. Enhanced Turnover Threshold of ₹10 Crore Under Section 63(1)(b)

In case of a person whose:

(i) Aggregate of all amounts received, including the amount received for sales, turnover, or gross receipts during the tax year, in cash, does not exceed 5% of the said amount; and

(ii) The aggregate of all payments made, including the amount incurred for expenditure, in cash, during the tax year does not exceed 5% of the said payment,

Businesses with predominantly digital transactions can avail a higher tax audit threshold of ₹10 crore, provided cash receipts and cash payments do not exceed 5% of the total receipts and payments respectively.

Businesses can also review our article on Tax Audit Turnover Limits for a better understanding of audit thresholds.

3. Tax Audit Requirement for Professionals Under Section 63(1)(c)

A person carrying on a profession is required to undergo a tax audit if the gross receipts from the profession exceed ₹50 lakh in a tax year.

4. Tax Audit Requirement for Presumptive Taxation Cases Under Section 63(1), Sl. No. 2

Taxpayers opting for presumptive taxation and declaring profits below the prescribed limits may become subject to tax audit requirements under Section 63.

5. Exception to Tax Audit Requirement Under Section 63(2)

Taxpayers declaring income in accordance with Sections 58(2) or 61(2) may not be required to undergo a tax audit under Section 63.

6. Furnishing of Tax Audit Report Under Section 63(3)

The assessee shall furnish by the specified date, the report of such audit in such form, duly signed and verified by the accountant and setting forth such particulars, as may be prescribed.

7. Compliance Through Audit Under Other Laws Under Section 63(4)

Where a person is required, by or under any other law, to get his accounts audited, then it shall be sufficient compliance of this section if such person:

(a) Gets the accounts of such business or profession audited under such law before the specified date; and

(b) Furnishes by that specified date the report of such audit along with the report of the accountant in the form as may be prescribed.

8. Meaning of “Specified Date” Under Section 63(5)(a)

The tax audit report must be furnished by the specified date prescribed under the Act, which is generally linked to the due date for filing the income tax return and may be revised through government notifications.

9. Treatment of Non-Account Payee Cheques and Bank Drafts Under Section 63(5)(b)

The payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash.

Ebizfiling’s Tax Audit Support

Ebizfiling provides professional assistance to help businesses and professionals comply with Section 63 of the Income-Tax Act, 2025.

Our services include:

- Determining tax audit applicability based on turnover, gross receipts, and presumptive taxation provisions.

- Assistance with preparing financial statements, books of accounts, and tax audit documentation.

- Coordination with Chartered Accountants for timely completion and filing of tax audit reports.

- End-to-end support for income tax compliance and statutory deadline management.

Learn more about tax audit limits, applicability criteria, and compliance requirements by reading our detailed guide on Tax Audit Applicability.

Conclusion

Section 63 of the Income-Tax Act, 2025 replaces Section 44AB and continues to govern tax audit requirements for businesses and professionals. While the law has been reorganized under the new Act, the tax audit limits and applicability conditions remain largely unchanged. Taxpayers should carefully assess their turnover, gross receipts, and eligibility for the ₹10 crore threshold to determine whether a tax audit is required. Staying compliant with Section 63 can help avoid penalties and ensure smooth tax filing and reporting.

Frequently Asked Questions

1. Are freelancers and consultants covered under Section 63 Tax Audit provisions?

Yes. Professionals such as consultants, architects, lawyers, doctors, and freelancers may require a tax audit if their gross professional receipts exceed ₹50 lakh during the tax year under Section 63 of the Income-Tax Act, 2025.

2. Is a tax audit under Section 63 different from a statutory audit?

Yes. A statutory audit is conducted under laws such as the Companies Act, while a Section 63 Tax Audit is carried out to verify compliance with the Income-Tax Act, 2025. Even if a business undergoes a statutory audit, it may still need to comply with tax audit requirements if the prescribed turnover or receipt limits are crossed.

3. Can a business with turnover above ₹1 crore avoid a tax audit under Section 63?

Yes, if cash receipts and cash payments do not exceed 5% of total receipts and payments respectively, the audit threshold increases to ₹10 crore. In such cases, a tax audit may not be required despite turnover exceeding ₹1 crore.

4. Is a tax audit required if income is declared under presumptive taxation?

If income is declared according to the presumptive taxation provisions specified under the Act, a tax audit may not be required. However, claiming lower profits than the prescribed limits can trigger Tax Audit Applicability.

5. What is the due date for filing a tax audit report under Section 63?

The tax audit report must be furnished by the specified date prescribed under the Act and relevant government notifications applicable for the relevant assessment year. Taxpayers should ensure timely submission to avoid penalties and compliance issues. The due date may vary if revised by the government through notifications.

6. Do digital payments affect tax audit applicability under the new law?

Yes. Businesses that primarily use digital modes of payment and keep cash transactions within the prescribed 5% limit can benefit from the higher ₹10 crore tax audit threshold under Section 63 of the Income-Tax Act, 2025.

7. What happens if a taxpayer misses the tax audit report filing deadline?

Failure to furnish the tax audit report by the specified date may attract penalties and lead to compliance issues. Timely completion of the Section 63 Tax Audit is essential to avoid penalties and ensure smooth tax compliance.

8. If accounts are already audited under another law, is a separate tax audit necessary?

A separate audit is generally not required. Taxpayers can use the audit conducted under another applicable law, provided the prescribed audit report and additional documentation are furnished within the specified timeline.

9. How can businesses determine their tax audit applicability under Section 63?

Businesses must evaluate turnover, cash transactions, and whether they are covered under presumptive taxation provisions. Ebizfiling can assist in assessing Tax Audit Applicability and identifying the compliance requirements applicable to a specific business.

10. Can Ebizfiling help with tax audit compliance under the Income-Tax Act, 2025?

Yes. Ebizfiling provides assistance with determining audit applicability, preparing documentation, coordinating with Chartered Accountants, and ensuring timely compliance with Section 63 of the Income-Tax Act, 2025 and income tax return filing.

File Income Tax Returns

Meet your tax filing obligations with ease and ensure timely submission of your Income Tax Return through a seamless online process.

About Ebizfiling -

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]