-

July 18, 2026

-

BySteffy A

Section 196 and 198 of the Income Tax Act 2025: STCG and LTCG

Introduction

Sections 196 and 198 of the Income-tax Act, 2025 prescribe special tax rates for eligible short-term and long-term capital gains arising from specified equity-related assets. Section 196 applies to eligible short-term capital gains, while Section 198 applies to eligible long-term capital gains. These provisions correspond to Sections 111A and 112A of the Income-tax Act, 1961 and apply from 1 April 2026.

This blog explains Section 196 and 198, their applicability, tax rates, conditions, and key differences.

What is Section 196 of the Income Tax Act, 2025?

Section 196 of the Income Tax Act, 2025 provides for the taxation of short-term capital gains arising from the transfer of specified equity-related capital assets. It applies to gains earned from the sale of equity shares, units of an equity-oriented fund, or units of a business trust, subject to prescribed conditions.

Applicability of Section 196

Section 196 applies where:

- The capital gain arises from the transfer of a short-term capital asset.

- The asset is an equity share in a company, a unit of an equity-oriented fund, or a unit of a business trust.

- The sale transaction is chargeable to Securities Transaction Tax (STT) under Chapter VII of the Finance (No. 2) Act, 2004.

Tax Rate under Section 196

Where the conditions of Section 196 are satisfied:

- Short-term capital gains are taxed at 20%.

- The balance of the total income is taxed according to the applicable income tax slab rates.

Benefit of Basic Exemption Limit

Resident individuals and Hindu Undivided Families (HUFs) can claim the benefit of the basic exemption limit. If the total income, excluding short-term capital gains under Section 196, is below the maximum amount not chargeable to tax, the unutilized exemption limit can be adjusted against such gains. Tax at 20% is payable only on the remaining balance.

Exception for IFSC Transactions

The requirement of paying STT does not apply to transactions undertaken on a recognised stock exchange located in an International Financial Services Centre (IFSC), provided the consideration for the transaction is paid or payable in foreign currency.

Deduction under Chapter VIII

If the gross total income includes short-term capital gains taxable under Section 196, deductions under Chapter VIII are allowed only on the gross total income after reducing such short-term capital gains.

To understand how gains from listed shares are classified and taxed, read our guide on income tax rules for equity share trading.

What is Section 198 of the Income Tax Act, 2025?

Section 198 of the Income Tax Act, 2025 provides for the taxation of long-term capital gains arising from the transfer of specified equity-related assets. It applies to long-term gains from equity shares, units of equity-oriented funds, and units of business trusts, subject to the prescribed Securities Transaction Tax conditions.

Applicability of Section 198

Section 198 applies where:

- The total income includes income chargeable under the head “Capital gains.”

- The gain arises from the transfer of a long-term capital asset.

- The asset is an equity share in a company, a unit of an equity-oriented fund, or a unit of a business trust.

- In the case of equity shares, STT has been paid on both acquisition and transfer.

- In the case of units of an equity-oriented fund or business trust, STT has been paid on transfer.

Tax Rate under Section 198

Long-term capital gains exceeding Rs. 1,25,000 are taxable at 12.5%. The balance income, after reducing such long-term capital gains, is taxed according to the applicable income tax rates.

Benefit of Basic Exemption Limit

A resident individual or Hindu Undivided Family can adjust the unused basic exemption limit against long-term capital gains under Section 198. Tax at 12.5% is charged only on the remaining taxable gain after such adjustment.

IFSC Exception

The STT condition does not apply to transfers carried out on a recognised stock exchange located in an International Financial Services Centre, where the consideration is received or receivable in foreign currency.

Deduction under Chapter VIII

Where the gross total income includes long-term capital gains covered under Section 198, deductions under Chapter VIII are allowed only from the gross total income remaining after reducing such capital gains.

Rebate under Section 156

The rebate under Section 156 is allowed from the income tax payable on total income after excluding the tax payable on long-term capital gains covered under Section 198. Therefore, the rebate cannot be used to reduce the tax directly payable on such long-term capital gains.

Meaning of Equity-Oriented Fund

For Section 198, an equity-oriented fund includes a specified mutual fund scheme or an eligible unit-linked insurance scheme meeting the prescribed investment conditions.

- In a fund-of-funds structure, at least 90% of the fund’s proceeds must be invested in another exchange-traded fund, and that fund must invest at least 90% of its proceeds in listed equity shares of domestic companies.

- In other cases, at least 65% of the fund’s total proceeds must be invested in listed equity shares of domestic companies.

The prescribed percentage is calculated with reference to the annual average of the monthly opening and closing figures. For eligible unit-linked insurance schemes, the applicable 90% or 65% condition must be satisfied throughout the policy term.

Taxpayers selling other eligible capital assets may also explore the available capital gains tax exemptions, subject to the conditions prescribed under the Income Tax Act.

Difference Between Section 196 and 198 of Income Tax Act

|

Particulars |

Section 196 |

Section 198 |

|

Applicable Capital Gain |

Short-Term Capital Gains (STCG) |

Long-Term Capital Gains (LTCG) |

|

Earlier Provision |

Section 111A of the Income-tax Act, 1961 |

Section 112A of the Income-tax Act, 1961 |

|

Applicable Assets |

Equity shares, equity-oriented mutual funds, and business trust units |

Equity shares, equity-oriented mutual funds, and business trust units |

|

Holding Period |

Short-term capital assets |

Long-term capital assets |

|

Tax Rate |

20% |

12.5% |

|

Exemption Threshold |

No exemption threshold |

Tax applies only on LTCG exceeding Rs. 1,25,000 |

|

Securities Transaction Tax (STT) |

STT must be paid on the sale transaction |

STT must be paid on acquisition and transfer of equity shares, and on transfer of equity-oriented fund units or business trust units |

|

Basic Exemption Limit Benefit |

Available to resident individuals and HUFs |

Available to resident individuals and HUFs |

|

IFSC Relaxation |

STT condition does not apply to eligible IFSC transactions in foreign currency |

STT condition does not apply to eligible IFSC transactions in foreign currency |

|

Chapter VIII Deduction |

Deduction is allowed after reducing STCG from Gross Total Income |

Deduction is allowed after reducing LTCG from Gross Total Income |

|

Rebate under Section 156 |

Section 196 does not contain a separate rebate restriction. Eligibility must be checked under Section 156 and the applicable tax regime |

The rebate under Section 156 cannot reduce the tax payable on long-term capital gains covered under Section 198.le on |

Conditions for Applicability of Sections 196 and 198 of Income Tax Act

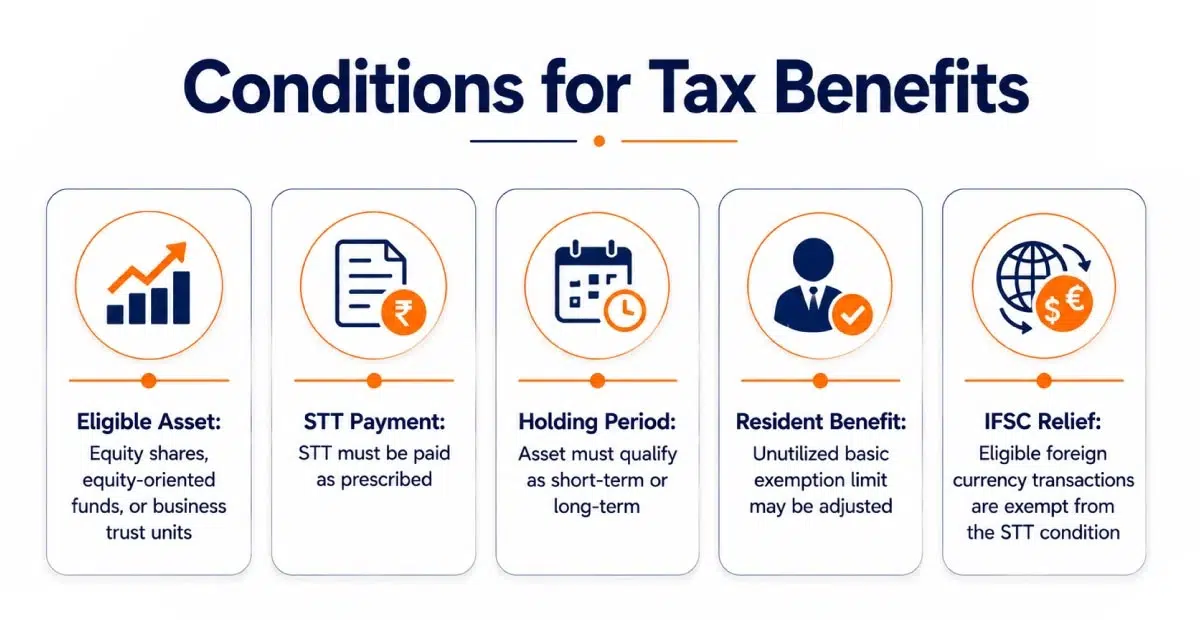

- Eligible Capital Asset: The gain must arise from an eligible equity share, equity-oriented fund, or business trust unit.

- Securities Transaction Tax (STT): STT must be paid as prescribed under the applicable section.

- Holding Period: The asset must qualify as a short-term or long-term capital asset based on the prescribed holding period.

- Resident Benefit: Resident individuals and HUFs can adjust the unutilized basic exemption limit against eligible capital gains.

- IFSC Relaxation: Eligible transactions carried out through recognized stock exchanges in an IFSC in foreign currency are exempt from the STT condition.

Capital gains arising from residential property may be governed by different exemption provisions, including Section 82 of the Income Tax Act, 2025.

Get Help with Capital Gains Tax Filing

Ebizfiling can help you calculate short-term and long-term capital gains under Section 196 and 198, file your Income Tax Return, respond to tax notices, and meet the applicable reporting requirements.

Related Services:

- Income Tax Return Filing

- Income Tax Notice Response

- Tax Planning and Advisory

- NRI Income Tax Return Filing

Get professional help with capital gains tax calculation and Income Tax Return filing under Section 196 and 198.

Conclusion

Section 196 and 198 of the Income Tax Act, 2025 set out separate tax rules for short-term and long-term capital gains on equity shares, equity-oriented funds, and business trust units. Section 196 taxes eligible short-term gains at 20%, while Section 198 taxes long-term gains above Rs. 1,25,000 at 12.5%. These sections replace Section 111A and 112A of the Income-tax Act, 1961.

Since the tax treatment depends on the type of asset, holding period, STT payment, and applicable exemptions, taxpayers should review these conditions carefully before filing their Income Tax Return.

FAQs on Section 196 and 198 of Income Tax Act

1. When does Section 196 apply to the sale of equity shares?

Section 196 applies when short-term capital gains arise from the sale of equity shares, units of an equity-oriented fund, or business trust units and the transaction is chargeable to Securities Transaction Tax. Eligible gains are generally taxed at 20%.

2. How is the ₹1.25 lakh threshold applied under Section 198?

The ₹1.25 lakh threshold applies to the aggregate qualifying long-term capital gains covered under Section 198 during the tax year. Only the eligible gains exceeding this amount are taxable at 12.5%, subject to the prescribed conditions.

3. Which assets are covered under Section 196 short term capital gains?

STCG under Section 196 applies to short-term capital gains arising from the transfer of equity shares, units of equity-oriented mutual funds, and units of business trusts, provided the prescribed STT conditions are satisfied.

4. What is the Section 198 long term capital gains tax rate?

Section 198 long term capital gains exceeding Rs. 1,25,000 are taxable at 12.5%. The balance income is taxed according to the applicable income tax rates.

5. Is STT mandatory under Section 196 and 198?

Yes, STT is generally required under Section 196 and 198. However, eligible transactions carried out through a recognised stock exchange in an IFSC and settled in foreign currency are exempt from this condition.

6. Can the basic exemption limit be adjusted against gains under Section 196 and 198?

Yes. A resident individual or HUF can adjust the unused basic exemption limit against eligible gains under Section 196 and 198, subject to the conditions provided in the Act.

7. How does Section 196 and 198 treat STT on equity shares?

Under Section 196, STT must be chargeable on the sale transaction. Under Section 198, STT is generally required on both acquisition and transfer of equity shares.

8. Are Chapter VIII deductions allowed against STCG under Section 196?

No direct deduction is allowed from STCG under Section 196. Chapter VIII deductions are allowed only from the gross total income remaining after reducing such short-term capital gains.

9. How should capital gains under Section 196 and 198 be reported in the Income Tax Return?

Capital gains under Section 196 and 198 must be reported in the applicable capital gains schedule of the Income Tax Return. Ebizfiling can assist with gain calculation, tax treatment, and accurate ITR filing.

10. Can Ebizfiling help with LTCG under Section 198 and tax notice response?

Yes. Ebizfiling can help calculate LTCG under Section 198, prepare the relevant ITR, review STT and exemption conditions, and assist with income tax notice responses.

Reliable Income Tax Filing Services

Get complete Income Tax Return support to ensure timely filing and smooth tax compliance every year.

About Ebizfiling -

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]