-

June 22, 2026

-

BySteffy A

Section 82 of the Income Tax Act 2025: Capital Gains Relief

Overview

Section 82 of the Income Tax Act, 2025, applicable from Assessment Year 2027-28, provides capital gains tax exemption to individuals and Hindu Undivided Families (HUFs) who sell a residential house property and reinvest the gains in another residential house in India. Replacing the old Section 54 of the Income-tax Act, 1961, the provision allows eligible taxpayers to reduce or eliminate their tax liability on long-term capital gains, subject to specified investment conditions and timelines.

In this article, we will discuss the provisions of Section 82, its eligibility conditions, exemption limits, reinvestment requirements, and key differences between Section 54 and Section 82.

Section 82 of the Income Tax Act 2025

Section 82 of the Income Tax Act, 2025 is a capital gains exemption provision that allows individuals and Hindu Undivided Families (HUFs) to claim relief from long-term capital gains tax on the sale of a residential house property, provided the gains are reinvested in another residential house in India within the prescribed timelines. The provision is formally titled “Profit on sale of property used for residence” under the 2025 Act.

This section is the direct successor to Section 54 of the Income Tax Act, 1961. All the core conditions, exemption limits, reinvestment rules, and CGAS requirements that applied under Section 54 continue under Section 82 without any substantive change. Taxpayers and professionals familiar with Section 54 will find Section 82 functionally identical, with only the section number and internal cross-references updated to reflect the new Act’s structure.

Section 82 vs Section 54: What Changed from AY 2027-28?

Section 54 of the Income Tax Act, 1961 applies to transactions governed by the old Act up to 31 March 2026. Section 82 applies from 1 April 2026 onwards, corresponding to Tax Year 2026-27 and AY 2027-28.

|

Provision |

Section 54 of the Income Tax Act, 1961 |

Section 82 of the Income Tax Act, 2025 |

|

Eligible assessee |

Individual or HUF | Individual or HUF (identical) |

| Original asset | Long-term residential house property |

Identical |

|

Purchase window |

1 year before / 2 years after | Identical |

| Construction window | 3 years after transfer |

Identical |

|

₹10 crore cap |

Introduced from AY 2024-25 | Continues under sub-section (7) |

| Two-house option | Gain ≤ ₹2 crore, once in lifetime |

Identical under sub-section (5) |

|

CGAS deposit deadline |

Section 139(1) due date | Section 263(1) due date (renumbered only) |

| Capital gains charge | Section 45 |

Section 67 (renumbered only) |

|

Effective from |

Up to transactions governed by the 1961 Act |

From 1 April 2026 (AY 2027-28 onwards) |

The only changes are internal cross-reference numbers.

Section 82 substantially retains the exemption framework that existed under Section 54 of the Income-tax Act, 1961, with the core eligibility conditions, reinvestment timelines, CGAS provisions, and exemption limits continuing under the new Act.

Short-Term vs Long-Term Capital Gains on Residential Property

For Section 82 of the Income Tax Act, 2025, only long-term capital gains qualify for exemption. Under the Income Tax Act, 2025, a residential house property held for more than 24 months is treated as a long-term capital asset, and the profit from its sale constitutes long-term capital gains. If the property is held for 24 months or less, the gains are short-term, and Section 82 does not apply.

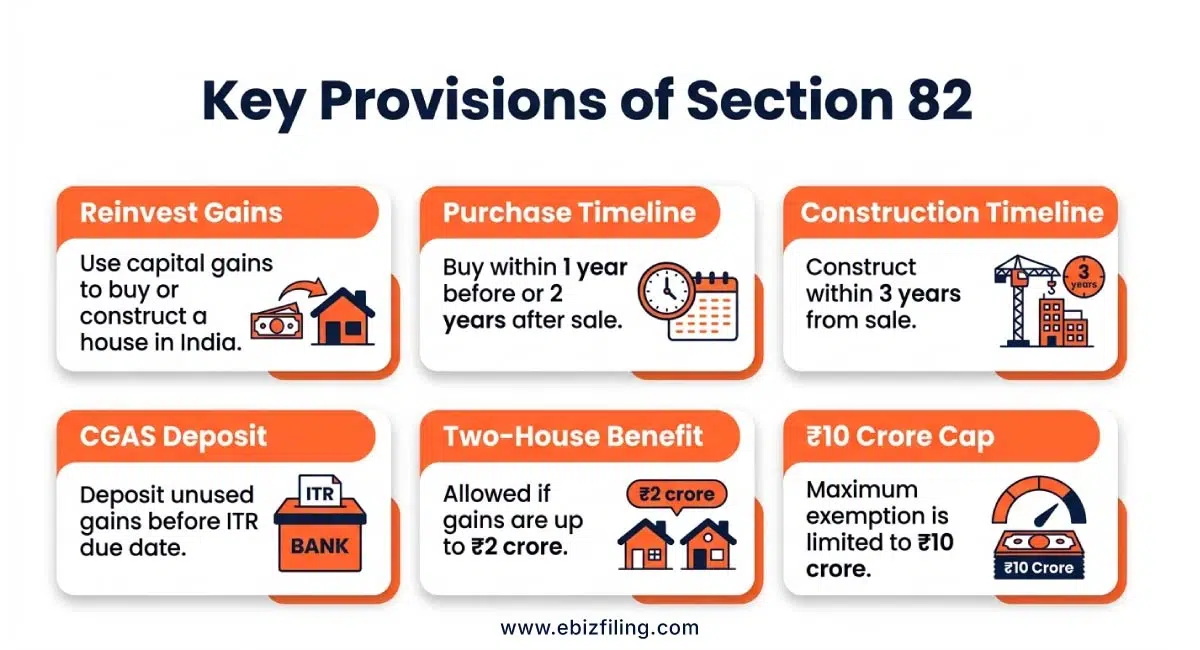

Key Provisions of Section 82 of the Income Tax Act, 2025

Exemption on Reinvestment of Capital Gains (Section 82(1)) :

Where an individual or Hindu Undivided Family (HUF) earns long-term capital gains from the sale of a residential house property and within one year before the date of transfer or within two years after the date of transfer, or constructs a residential house within three years, the capital gains may qualify for exemption under Section 82.

Example: Mr. A sold a residential house and earned a long-term capital gain of ₹75 lakh. He purchased another residential house in India for ₹75 lakh within two years of the sale. Since the entire capital gain was reinvested in the new residential property, he can claim full exemption under Section 82 of the Income Tax Act, 2025, and no capital gains tax will be payable on the transaction. This exemption will be available only if all other conditions under Section 82 are satisfied.

Deposit of Unutilized Capital Gains (Section 82(2)):

If the capital gains are not utilized before filing the income tax return, the unutilized amount must be deposited under the Capital Gains Account Scheme (CGAS) before the due date prescribed for filing the income tax return under Section 263(1) of the Income Tax Act, 2025.

Treatment of Deposited Amount (Section 82(3)) :

The amount already invested in the new house together with the amount deposited under CGAS is deemed to be the cost of the new asset for claiming exemption.

Taxability of Unused CGAS Amount (Section 82(4)) :

If the deposited amount is not utilized within the prescribed period, the unutilized portion becomes taxable as capital gains in the year in which the three-year period expires.

Two-House Benefit (Section 82(5)) :

Where the capital gains do not exceed ₹2 crore, the taxpayer may opt to purchase or construct two residential houses in India and claim exemption.

One-Time Option for Two Houses (Section 82(6)) :

The benefit of investing in two residential houses can be exercised only once and cannot be claimed again in any other tax year.

₹10 Crore Cost Restriction (Section 82(7)) :

If the cost of the new residential house exceeds ₹10 crore, the amount exceeding ₹10 crore is ignored while computing the exemption.

₹10 Crore Capital Gains Restriction (Section 82(8)) :

If the capital gains exceed ₹10 crore, the excess amount is not eligible for exemption under Section 82.

Documents Required to Claim Exemption Under Section 82 of Income Tax Act

To successfully claim exemption under Section 82 of the Income Tax Act, 2025, taxpayers should maintain the following documents:

- Sale deed of the original residential property.

- Purchase deed of the new residential house, if purchased.

- Possession letter of the new residential property, where applicable.

- Construction-related documents, contractor agreements, invoices, and payment records, if a house is constructed.

- Completion certificate or occupancy certificate, where available for a newly constructed property.

- Capital gains computation statement showing the calculation of long-term capital gains.

- Capital Gains Account Scheme (CGAS) deposit receipt, if the capital gains were temporarily parked under the scheme.

- CGAS account passbook, account statement, or other records showing deposits and withdrawals under the scheme.

- Bank statements and payment proofs relating to the purchase or construction of the new residential property.

- Income Tax Return and supporting schedules reflecting the exemption claimed under Section 82.

Proper documentation helps substantiate the exemption claim, demonstrate compliance with reinvestment and CGAS requirements, and reduce the risk of disputes during tax assessment or scrutiny.

Capital Gains Tax Filing Support by Ebizfiling

Ebizfiling helps individuals and HUFs with income tax return filing for capital gains earned from the sale of residential property. If you are planning to claim exemption under Section 82 of the Income Tax Act, 2025, our tax experts can help you calculate the capital gain, review the reinvestment amount, check CGAS requirements, and report the exemption correctly in your ITR.

We also assist with capital gains computation, property sale documentation review, tax-saving guidance, and online ITR filing for taxpayers who have sold residential house property in India.

Need help with Income tax filing? Connect with Ebizfiling today.

Conclusion

For taxpayers selling a residential house, Section 82 of the Income Tax Act, 2025 offers a valuable opportunity to reduce capital gains tax through timely reinvestment in another residential property. While the provision largely mirrors the earlier Section 54, understanding the reinvestment timelines, CGAS requirements, two-house option, and ₹10 crore cap is essential to claim the exemption successfully. A well-planned property transaction can help taxpayers preserve more of their gains and avoid unnecessary tax outflows while remaining fully compliant with the law. Taxpayers should maintain proper documentation and comply with prescribed timelines to ensure uninterrupted exemption benefits under Income Tax Act Section 82.

Suggested Reads:

Key Clauses for the Sale Deed Agreement

Frequently Asked Questions

1. What is the significance of the ₹10 crore cap under Section 82 of the Income Tax Act, 2025?

Section 82 of the Income Tax Act, 2025 restricts the exemption available on long-term capital gains to a maximum of ₹10 crore. Any capital gain exceeding this limit will not qualify for Section 82 capital gains exemption, even if a higher amount is reinvested in a residential property.

2. How does the two-house benefit under Section 82 operate?

The two-house benefit under Section 82 of the Income Tax Act, 2025, permits investment in two residential houses instead of one when the capital gains do not exceed ₹2 crore. This benefit can be exercised only once and is intended to provide flexibility in tax exemption on residential property sale.

3. Why is the Capital Gains Account Scheme (CGAS) important for claiming exemption under Section 82?

The CGAS allows taxpayers to preserve their exemption claim when the capital gains have not been fully utilized before the due date for filing the income tax return. Depositing the unutilized amount within the prescribed timeline is essential to retain eligibility for capital gains exemption on sale of residential house.

4. What happens to unutilized funds deposited under the Capital Gains Account Scheme?

If the amount deposited under the Capital Gains Account Scheme is not utilized for purchasing or constructing a residential house within the specified period, the unutilized balance becomes taxable as capital gains in the relevant tax year under Section 82 of the Income Tax Act, 2025.

5. Why is Section 82 considered the successor to Section 54?

Section 82 replaces Section 54 under the Income Tax Act, 2025. In Section 82 vs Section 54, the exemption framework, investment conditions, timelines, and limits remain substantially similar, with only the section numbering and statutory references being updated.

6. What is the prescribed time limit for purchasing a new residential house under Section 82?

The new residential house may be purchased within one year before the transfer or within two years after the transfer of the original residential property. These timelines are mandatory for claiming Section 82 of the Income Tax Act, 2025, capital gains exemption.

7. What is the prescribed time limit for constructing a new residential house under Section 82?

Where the exemption is claimed based on construction, the residential house must be completed within three years from the date of transfer of the original residential property to claim tax exemption on residential property sale.

8. How is the exemption amount calculated under Section 82?

The exemption is limited to the lower of the long-term capital gain or the cost of the new residential house, subject to statutory limits such as the ₹10 crore cap and other conditions prescribed under Section 82. Ebizfiling can help taxpayers calculate the eligible exemption correctly and report it accurately while filing their income tax return.

9. What are the key conditions for claiming capital gains exemption on the sale of a residential house under Section 82?

The taxpayer must earn long-term capital gains from a residential house property and reinvest the gains in a residential house situated in India within the specified purchase or construction timelines. Ebizfiling can assist with checking eligibility, CGAS compliance, and accurate reporting of capital gains exemption on sale of residential house in the income tax return.

10. What happens if the new residential house is sold within three years?

If the new residential house is sold within three years of purchase or construction, the exemption claimed under Section 82 may be withdrawn by adjusting the exempted amount against the cost of acquisition, resulting in higher taxable capital gains.

File Your Income Tax Return Online with Expert Assistance

Expert-assisted Income Tax Return filing to help you stay compliant and claim eligible deductions with confidence.

About Ebizfiling -

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]