-

July 23, 2026

-

BySteffy A

Section 115BAC of the Income Tax Act: Tax Slabs and Rules

Introduction

Section 115BAC of the Income Tax Act, 1961 governed the new tax regime for individuals and certain other eligible taxpayers for income earned up to 31 March 2026. It was introduced by the Finance Act, 2020 and was later made the default tax regime.

Under this regime, taxpayers benefited from revised slab rates but could not claim several deductions and exemptions available under the old tax regime. For income earned from 1 April 2026 onwards, the corresponding new tax regime provision is contained in Section 202 of the Income Tax Act, 2025.

This article explains the tax slabs applicable for FY 2025–26, rebate, available deductions, restrictions, Form 10-IEA requirements and TDS rules under the new tax regime.

What is Section 115BAC of the Income Tax Act?

Section 115BAC of the Income Tax Act, 1961 provided the new tax regime for calculating income tax at revised slab rates for income earned up to 31 March 2026. Taxpayers using this regime cannot claim several deductions and exemptions available under the old tax regime.

When Section 115BAC of the Income Tax Act was introduced, eligible taxpayers had to opt for it specifically. Following amendments made by the Finance Act, 2023, the new tax regime became the default regime. An eligible taxpayer is therefore taxed under the new regime unless the taxpayer opts for the old regime in the prescribed manner.

The new tax regime under Section 115BAC of the Income Tax Act applied to:

- Individuals

- Hindu Undivided Families

- Associations of Persons, other than co-operative societies

- Bodies of Individuals

- Artificial Juridical Persons

Eligible taxpayers governed by Section 115BAC could choose the old tax regime by following the prescribed procedure. However, the procedure and switching restrictions depend on whether the taxpayer has income from a business or profession.

Section 115BAC and Section 202: Which Provision Applies?

Section 115BAC of the Income Tax Act, 1961 continues to govern income earned up to 31 March 2026. Returns, assessments, and other proceedings relating to income earned before 1 April 2026 continue to be governed by the relevant provisions of the 1961 Act.

From Tax Year 2026-27, which began on 1 April 2026, the corresponding new tax regime provision is Section 202 of the Income Tax Act, 2025.

Section 202 broadly continues the default new tax regime for individuals, HUFs, AOPs other than co-operative societies, BOIs and artificial juridical persons. It also retains separate switching restrictions for taxpayers with business or professional income.

Form 10-IEA specifically refers to Section 115BAC of the Income Tax Act, 1961. It should therefore not be described as the prescribed form under Section 202. Taxpayers covered by the Income Tax Act, 2025 must follow the applicable return and option requirements prescribed for Section 202.

Section 115BAC Tax Slabs

The following tax slabs applied under the new tax regime to income earned during FY 2025–26, corresponding to AY 2026–27:

|

Total Income |

Tax Rate |

|

Up to ₹4,00,000 |

Nil |

| ₹4,00,001 to ₹8,00,000 |

5% |

|

₹8,00,001 to ₹12,00,000 |

10% |

| ₹12,00,001 to ₹16,00,000 |

15% |

|

₹16,00,001 to ₹20,00,000 |

20% |

| ₹20,00,001 to ₹24,00,000 |

25% |

|

Above ₹24,00,000 |

30% |

The same slab structure applies under Section 202 of the Income Tax Act, 2025, for Tax Year 2026–27.

These rates are applied progressively. For example, where a taxpayer’s total income is ₹14 lakh, the entire income is not taxed at 15%. Each portion of income is taxed at the rate applicable to the relevant slab.

Health and Education Cess at 4% is charged on the income tax and applicable surcharge.

Rebate Under Section 87A

A resident individual whose total income does not exceed ₹12 lakh under the new tax regime may claim a rebate under Section 87A.

The rebate is limited to:

- ₹60,000; or

- The income tax payable at the normal slab rates,

whichever is lower.

The rebate is limited to the income tax calculated at the normal slab rates under the new tax regime. It cannot be adjusted against tax payable on income taxed at special rates. This may include specified capital gains, lottery winnings, virtual digital asset income and other specially taxed income.

Marginal relief may apply where the total income slightly exceeds ₹12 lakh and the additional tax payable is more than the amount by which the total income exceeds ₹12 lakh.

A salaried resident individual with salary income of up to ₹12.75 lakh before standard deduction may have no income tax liability after claiming the standard deduction of ₹75,000. This is subject to the applicable conditions and assumes that the taxpayer does not have other income or income taxable at a special rate.

Under the Income Tax Act, 2025, the corresponding rebate is contained in Section 156.

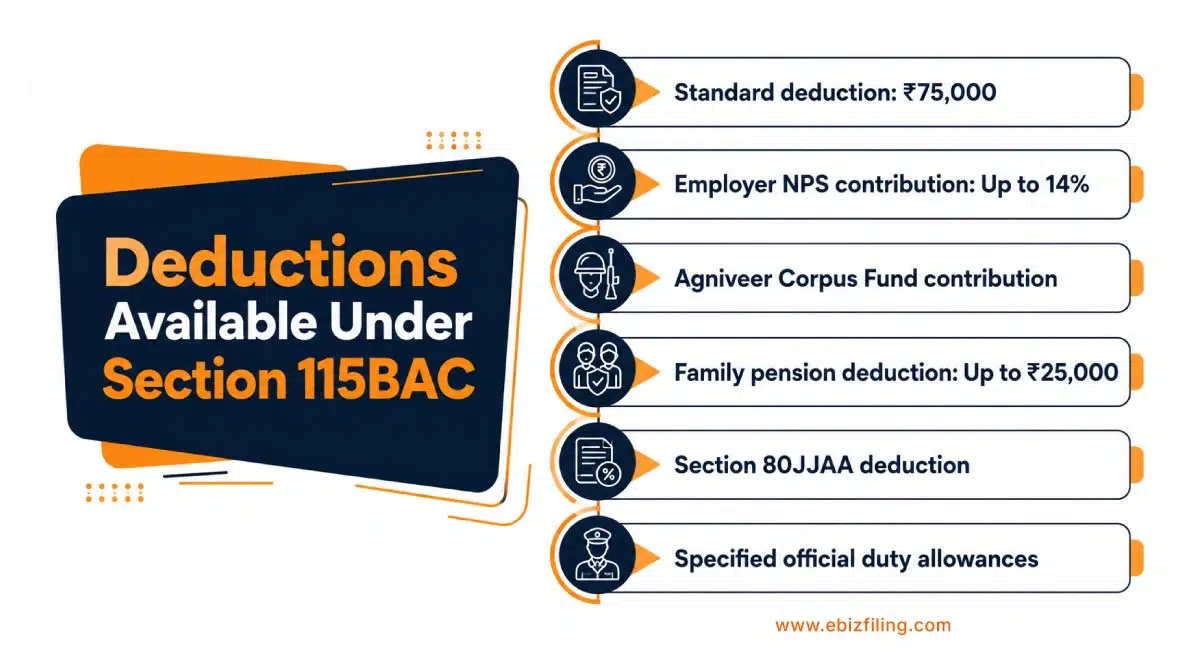

Deductions Available Under Section 115BAC of the Income Tax Act

The new tax regime restricts several deductions, but it does not remove every tax benefit. The following important deductions and allowances continue to be available.

1. Standard Deduction

A salaried employee or pensioner can claim a standard deduction of ₹75,000 or the amount of salary or pension income, whichever is lower.

The standard deduction is also available where income is calculated under Section 202 of the Income Tax Act, 2025.

2. Employer’s Contribution to NPS

A deduction is available under Section 80CCD(2) for an eligible contribution made by an employer to the employee’s National Pension System account.

Under the new tax regime, the deduction under Section 80CCD(2) may be claimed up to 14% of salary, subject to the prescribed conditions and the overall limit applicable to specified employer contributions.

3. Central Government Contribution to the Agniveer Corpus Fund

An eligible individual can claim a deduction under Section 80CCH(2) for the amount contributed by the Central Government to the individual’s Agniveer Corpus Fund account.

The exception available under Section 115BAC of the Income Tax Act specifically covers the Central Government contribution under Section 80CCH(2).

4. Family Pension Deduction

A taxpayer receiving a family pension can claim a deduction equal to:

- One-third of the family pension; or

- ₹25,000,

whichever is lower, where income is calculated under the new tax regime.

5. Deduction Under Section 80JJAA

An eligible business can claim a deduction under Section 80JJAA for additional employee cost, subject to the conditions prescribed under the Income Tax Act.

6. Specified Employment Allowances

Certain allowances paid for performing official duties may continue to qualify for exemption, including:

- Travelling allowance for an official tour or transfer

- Daily allowance for expenses during an official tour

- Conveyance allowance for performing official duties

- Prescribed transport allowance for an eligible employee with a specified disability

Deductions under Sections 80CCD(2), 80CCH(2) and 80JJAA continue to be available under Section 115BAC of the Income Tax Act, subject to their respective conditions.

Deductions Not Available Under the New Tax Regime

The following commonly claimed deductions and exemptions were generally not available under Section 115BAC of the Income Tax Act:

- Section 80C deduction for PPF, ELSS, life insurance premiums and specified investments

- Section 80D deduction for medical insurance premiums

- House Rent Allowance exemption under Section 10(13A)

- Leave Travel Concession exemption

- Section 80E deduction for education loan interest

- Section 80G deduction for donations

- Section 80TTA and Section 80TTB deductions

- Section 80GG deduction for rent paid

- Interest deduction under Section 24(b) for a self-occupied house property

- Professional tax deduction

- Most other Chapter VI-A deductions

A loss under the head “Income from house property” cannot generally be set off against income under another head while using the new tax regime.

Taxpayers claiming significant HRA, home loan interest, medical insurance, investment and donation deductions should calculate their tax liability under both regimes before making a decision.

Form 10-IEA for Taxpayers Having Business Income

A taxpayer having business or professional income was not disqualified from using the new tax regime. However, the procedure for opting for the old tax regime was more restrictive for such taxpayers.

Under Section 115BAC of the Income Tax Act, 1961, an eligible taxpayer having business or professional income was generally required to file Form 10-IEA on or before the due date prescribed under Section 139(1) to opt out of the default new tax regime.

Form 10-IEA was not generally required for an individual who did not have business or professional income. Such a taxpayer could ordinarily select the old tax regime while filing the applicable income tax return.

After opting for the old regime, a taxpayer having business or professional income could subsequently withdraw the option and return to the new regime. However, after returning to the new regime, the taxpayer generally could not select the old regime again unless the taxpayer ceased to have business or professional income.

Form 10-IEA specifically applied to options exercised under Section 115BAC of the Income Tax Act, 1961, including returns for income earned during FY 2025–26. It should not be described as the prescribed form for exercising an option under Section 202 of the Income Tax Act, 2025. Taxpayers governed by Section 202 must follow the procedure and forms prescribed under the new law.

Professional Income Tax Return Filing Support by Ebizfiling

Ebizfiling assists taxpayers with accurate Income Tax Return Filing by reviewing their income, deductions, TDS details and applicable tax regime.

Ebizfiling Assistance Includes

- Comparison of the old and new tax regimes

- Review of income and TDS details

- Identification of eligible deductions

- Selection of the correct ITR form

- Form 10-IEA assistance, where applicable

- Income tax return filing and verification support

Get expert assistance with accurate Income Tax Return Filing.

Conclusion

Section 115BAC of the Income Tax Act provided the default new tax regime with revised slab rates and restricted deductions and exemptions. Taxpayers were advised to calculate their tax liability under both regimes before making a final choice.

For income earned from 1 April 2026 onwards, Section 202 of the Income Tax Act, 2025 became the corresponding new tax regime provision. Individuals without business or professional income could generally select the suitable regime while filing their income tax return. Taxpayers having business or professional income were required to follow the prescribed switching restrictions and Form 10-IEA requirements for returns governed by the Income Tax Act, 1961.

Frequently Asked Questions

1. Was Section 115BAC of the Income Tax Act the default tax regime?

Yes. Section 115BAC provided the default new tax regime for eligible taxpayers for income earned up to 31 March 2026. From 1 April 2026, the corresponding default new tax regime is contained in Section 202 of the Income Tax Act, 2025.

2. Can HRA exemption be claimed under the new tax regime?

No. The House Rent Allowance exemption under Section 10(13A) is generally not available under the new tax regime. Taxpayers receiving HRA should compare their tax liability under both regimes before making a choice.

3. Is the standard deduction available under Section 115BAC of the Income Tax Act?

Yes. Eligible salaried employees and pensioners can claim a standard deduction of ₹75,000 or the amount of salary or pension income, whichever is lower.

4. Does a salaried taxpayer need Form 10-IEA to choose the old regime?

A salaried taxpayer without business or professional income generally does not need to file Form 10-IEA. The taxpayer can opt for the old tax regime while filing the applicable income tax return.

5. When is Form 10-IEA required under Section 115BAC of the Income Tax Act?

Form 10-IEA is generally required where an eligible taxpayer having business or professional income wants to opt out of the default new tax regime under Section 115BAC. It must be filed on or before the applicable due date under Section 139(1). Ebizfiling can assist taxpayers with reviewing the conditions, filing Form 10-IEA and completing their income tax return accurately.

6. Can a taxpayer having business income change the tax regime every year?

No. A taxpayer having business or professional income cannot freely switch between the old and new regimes every year. Once the taxpayer withdraws the old regime option and returns to the new regime, the old regime generally cannot be selected again unless the taxpayer stops having business or professional income.

7. What happens if an employee does not declare a tax regime to the employer?

Where an employee does not communicate a preference, the employer will generally calculate salary TDS under the default new tax regime. The regime used by the employer for TDS does not necessarily determine the employee’s final choice while filing the return.

8. Can the regime selected in the ITR differ from the regime declared to the employer?

Yes. An employee without business or professional income may generally select a different tax regime while filing the income tax return. This may result in additional tax payable or a refund of excess TDS. Ebizfiling experts can compare the old and new regimes, review eligible deductions and assist with accurate Income Tax Return Filing.

9. Are Sections 80C and 80D deductions available under Section 115BAC?

No. Deductions for specified investments under Section 80C and medical insurance premiums under Section 80D are generally unavailable. However, specified benefits such as standard deduction and employer NPS contribution remain available, subject to the applicable conditions.

10. What is the corresponding provision for Section 115BAC under the Income Tax Act, 2025?

From 1 April 2026, the corresponding new tax regime provision is Section 202 of the Income Tax Act, 2025. Section 115BAC of the Income Tax Act remains relevant for income, returns and proceedings governed by the Income Tax Act, 1961.

ITR filing

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling

About Ebizfiling -

Reviews

Anish Mehta

04 Jan 2018"I would whole heartedly recommend ebizfiling for their professional and diligent work. We are delighted to acknowledge the excellent services provided by ebizfiling for the legal structuring and compliance. I would like to thank ebizfiling, for their approachability, fair pricing and timely responses."

Devangi Patnayak

11 Mar 2018I am very happy with the way they serve their clients. They are focused on providing the best help that they can and are result oriented.

Kavya Talada

29 Mar 2022Private company incorporation was done by ebizfiling I really thank the entire team for giving best service and with affordable price.. I have inquired many firms but ebizfiling is the best service

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]