-

June 29, 2026

-

BySteffy A

Section 37 of the Income Tax Act 2025: Actual Payment Deductions

Introduction

Section 37 of the Income Tax Act 2025 governs certain business deductions that can be claimed only when the actual payment is made, regardless of the accounting method followed by the taxpayer. It covers includes such as taxes, employer contributions to welfare funds, leave encashment, specified interest payments, and delayed payments to MSMEs.

This provision replaces the erstwhile Section 43B of the Income-tax Act, 1961 and continues the same principle of allowing specified deductions on an actual payment basis, with a more streamlined structure under the new law.

In this blog, we will understand the scope of Section 37 of the Income Tax Act 2025, the deductions covered under it, its impact on MSME payments, and the key compliance points businesses should know before claiming deductions.

Section 37 of the Income Tax Act 2025

Section 37 of the Income Tax Act 2025 deals with certain deductions allowed on an actual payment basis only. In simple terms, even if an expense is otherwise allowable as a deduction under the Act, the deduction can be claimed only when the amount is actually paid.

The section overrides the accounting method followed by the taxpayer and focuses on the actual payment of specified liabilities. As a result, merely recording an expense in the books of accounts does not automatically make it deductible for tax purposes.

Section 37 of the Income Tax Act 2025 is the corresponding provision of the erstwhile Section 43B of the Income tax Act 1961. While the section number has changed, the core principle remains the same: certain deductions are allowed only on an actual payment basis. The new law presents the provision in a more streamlined and structured format while retaining its substantive effect.

What Is the Difference Between Section 37 and 43B?

|

Particulars |

Section 43B of the Income Tax Act 1961 |

Section 37 of the Income Tax Act 2025 |

|

Provision Title |

Certain deductions are allowed only on actual payment | Certain deductions allowed on an actual payment basis only |

| Section Number | Section 43B |

Section 37 |

|

Applicability |

Income-tax Act, 1961 | Income Tax Act, 2025 |

| Core Principle | Deduction allowed only on actual payment |

Deduction allowed only on actual payment |

|

MSME Payments |

Covered through Section 43B(h) | Covered under Section 37(2)(g) |

| Structure | Multiple amendments and explanations added over time |

Reorganised and presented in a more streamlined format |

|

Accounting Method |

Actual payment requirement applied | Expressly states that deduction is allowed irrespective of the accounting method followed |

| Liability Year | Actual payment basis applied |

Expressly states that deduction is allowed irrespective of the tax year in which liability was incurred |

For a detailed explanation of the tax implications of delayed payments to micro and small enterprises, check out our article on Section 43B(h) for MSME Payments.

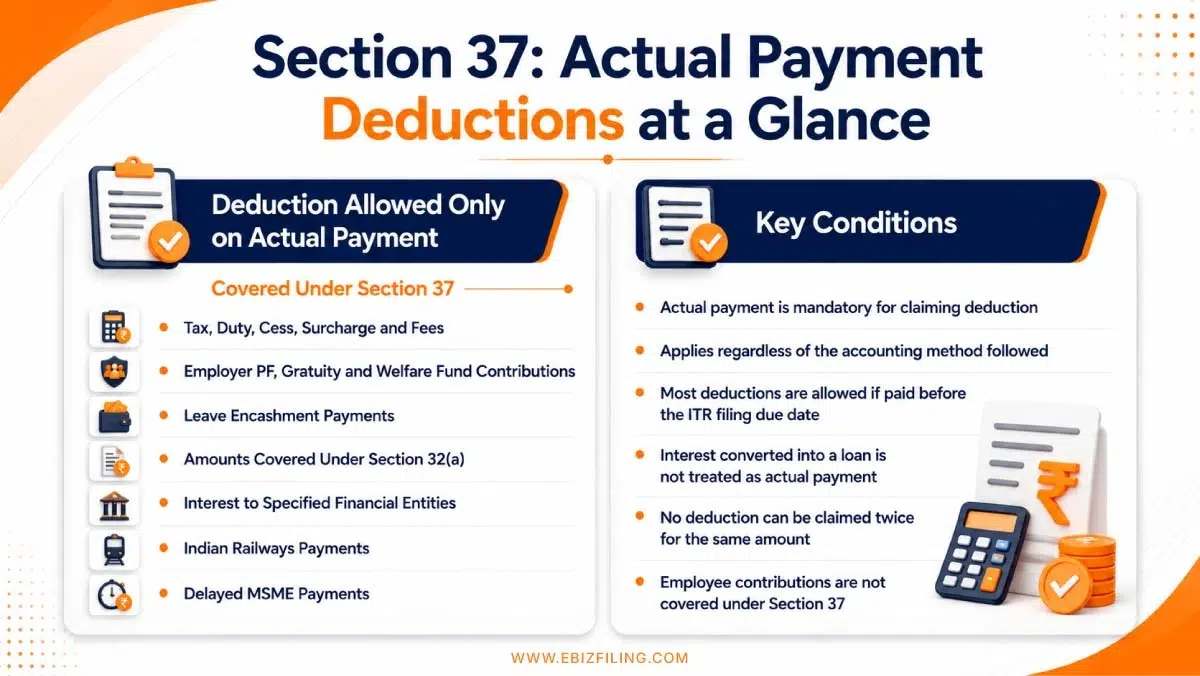

Certain Deductions Allowed on Actual Payment Basis Under Section 37

The following are the deductions covered under Section 37 of the Income Tax Act 2025 can be claimed only on an actual payment basis.

Understanding these provisions helps businesses comply with the Income Tax Act 2025 and avoid the disallowance of eligible business deductions.

General Rule Under Section 37(1)

The sums payable, as specified in sub-section (2), shall be allowed as deductions while computing income chargeable under Section 26 only in the tax year in which they are actually paid, irrespective of:

- Any provision to the contrary in this Act; or

- Method of accounting regularly followed; or

- The tax year in which the liability was incurred.

Sums Covered Under Section 37(2)

The following sums are covered under Section 37(2):

- Section 37(2)(a) : Tax, duty, cess, surcharge or fee, by whatever name called, levied under any law in force.

- Section 37(2)(b) : Contribution of the employer to a provident fund or superannuation fund or gratuity fund or any fund for the welfare of employees.

- Section 37(2)(c) : Amount payable by employer in lieu of any leave at the credit of the employee.

- Section 37(2)(d) : Any sum referred to in section 32(a).

- Section 37(2)(e) : Interest on loans or advances or borrowings from specified financial entities as per the terms and conditions of the agreement governing such loans or advances or borrowings.

- Section 37(2)(f) : Amount payable to the Indian Railways for use of railway assets.

- Section 37(2)(g) : Amount payable by the assessee to a micro or small enterprise beyond the time limit specified in section 15 of the Micro, Small and Medium Enterprises Development Act, 2006.

If your business has not yet obtained MSME Registration, Ebizfiling can help you complete the registration process and avail the benefits available under the MSMED Act.

Payment Made Before Return Filing Due Date [Section 37(3)]

In case the amounts specified in Section 37(2), except the sum referred to in clause (g), are paid after the end of the tax year in which the liability was incurred, but on or before the due date of filing of return of income under section 263(1) for such tax year, the deduction towards such sum shall be allowed in such tax year.

Conversion of Interest Into Loan Is Not Actual Payment [Section 37(4)]

If interest on loans or advances or borrowings specified in Section 37(2)(e) is converted into a loan or advance or debenture or any other instrument by which the liability to pay is deferred to a future date, then it shall not be deemed to have been actually paid.

No Double Deduction Allowed [Section 37(5)]

If a deduction in respect of any sum payable under Section 37(2) has already been allowed in any tax year when such liability was incurred, it shall not be allowed again in any subsequent tax year when it is paid.

Employee Contributions Not Covered [Section 37(6)]

The provisions of this section shall not apply to a sum received by the assessee from any employee as contribution towards any of the funds referred to in section 2(49)(o).

Meaning of Specified Financial Entities [Section 37(7)]

For the purposes of this section, “specified financial entities” means a public financial institution or State Financial Corporation or State Industrial Investment Corporation or such class of non-banking financial companies as may be notified by the Central Government or a scheduled bank or a co-operative bank (other than a primary agricultural credit society or a primary co-operative agricultural and rural development bank).

Meaning of “Sum Payable” [Section 37(8)]

For the purposes of Section 37(2)(a), “the sum payable” means a sum for which the assessee has incurred liability in the tax year even though such sum might not have been payable within that year under the relevant law.

Income Tax Compliance Support from Ebizfiling

Understanding provisions such as Section 37 of the Income Tax Act 2025 is important for claiming eligible deductions and avoiding tax disallowances. Since deductions under this section are allowed only on an actual payment basis, businesses must ensure timely compliance and proper documentation.

Ebizfiling can help you with:

- Income Tax Return (ITR) Filing

- Tax Compliance and Advisory

- MSME Payment Compliance

- Deduction Planning and Review

- Business Tax Support

Avoid filing errors and missed deadlines. Choose Ebizfiling’s Business Income Tax Return Filing service for expert support, timely compliance, and hassle-free tax filing for your business.

Final Thoughts

Section 37 of the Income Tax Act 2025 continues the actual-payment-based deduction framework that previously existed under Section 43B of the Income Tax Act 1961. The section allows specified deductions only when the payment is actually made and covers liabilities such as taxes, employer welfare fund contributions, leave encashment, interest payable to specified financial entities, railway dues, and certain MSME payments.

Businesses should pay close attention to the deduction conditions prescribed under Section 37, particularly the provisions relating to MSME payment timelines and actual payment requirements. Proper compliance, timely payments, and accurate record-keeping can help taxpayers claim eligible deductions and avoid unnecessary disallowances during tax assessments. Whether you are a startup, MSME, LLP, or company, understanding the practical application of Section 37 of the Income Tax Act 2025 is essential for effective income tax compliance and deduction planning.

FAQs on Section 37 of the Income Tax Act 2025

1. Can a company claim a deduction under Section 37 if GST liability is recorded but not paid during the tax year?

No. Under Section 37 of the Income Tax Act 2025, merely recording GST, tax, cess, surcharge, or similar statutory liabilities in the books of accounts does not make them deductible. These expenses qualify as certain deductions allowed on an actual payment basis only after the amount is actually paid, subject to the conditions prescribed under the Act.

2. How do MSME payment deduction rules under Section 37 affect businesses?

Businesses purchasing goods or services from micro and small enterprises must comply with the payment timelines prescribed under the MSMED Act, 2006. If payments are delayed beyond the permitted period, the related expenditure may be disallowed for that tax year and allowed only when the payment is actually made. Therefore, MSME payment deduction rules have become a critical compliance requirement for businesses.

3. Can an employer claim a deduction for unpaid leave encashment under Section 37?

No. Section 37 of the Income Tax Act 2025 specifically requires actual payment for leave encashment deductions. If an employer merely creates a provision for leave encashment in its financial statements but does not make the payment to employees, the deduction cannot be claimed for that tax year.

4. What happens if employer contributions to PF, ESI, or gratuity funds are paid after the end of the financial year?

Employer contributions covered under Section 37 of the Income Tax Act 2025 may still qualify for deduction if the payment is made on or before the due date of filing the income tax return for that year. This provision helps taxpayers claim eligible deductions even when the payment is made after the financial year closes but within the prescribed timeline.

5. Why are Section 37 MSME payments treated differently from other actual payment deductions?

Most expenses covered under Section 37 of the Income Tax Act 2025 can qualify for deduction if they are paid before the return filing due date. However, Section 37 MSME payments are subject to stricter provisions linked to the MSMED Act. Delayed payments to eligible MSMEs may result in deduction disallowance even if the payment is made before the income tax return filing deadline.

6. Can interest payable to a bank, NBFC, or financial institution be claimed as a deduction if it is converted into another loan?

No. Section 37 of the Income Tax Act 2025 clearly states that conversion of interest into a fresh loan, advance, debenture, or any other instrument that postpones payment does not amount to actual payment. Therefore, the deduction can be claimed only when the interest amount is genuinely paid and not merely restructured.

7. Does Section 37 apply even if a business follows the mercantile system of accounting?

Yes. One of the key Section 37 deduction conditions is that the deduction is allowed only on actual payment, irrespective of the accounting method followed by the taxpayer. Whether a business follows the cash system or the mercantile system, actual payment remains the determining factor for claiming deductions under this section.

8. How can businesses avoid disallowance of deductions under Section 37 of the Income Tax Act 2025?

Businesses should maintain a structured payment tracking system for statutory dues, employee welfare fund contributions, interest liabilities, and MSME invoices. Regular reconciliation of outstanding liabilities and timely payments can significantly reduce the risk of deduction disallowances. Businesses seeking professional support for tax compliance, deduction reviews, and MSME payment monitoring can consult Ebizfiling to ensure compliance with Section 37 requirements.

9. Are payments made to medium enterprises also covered under Section 37(2)(g)?

No. Section 37(2)(g) specifically applies to payments due to micro and small enterprises as defined under the MSMED Act, 2006. Payments made to medium enterprises are generally not subject to the same deduction restrictions applicable to micro and small enterprise dues.

10. What documents should taxpayers maintain to support actual payment deductions under the Income Tax Act 2025?

Taxpayers should maintain proper records such as payment challans, bank statements, PF and ESI deposit receipts, MSME invoices, loan repayment records, tax payment proofs, and other supporting documents. These records help establish eligibility for actual payment deductions under the Income Tax Act 2025 during assessments and audits. Ebizfiling assists businesses in maintaining compliance records and preparing documentation required to support deduction claims under Section 37.

Stay Compliant with Timely TDS Returns

Let our experts manage your TDS return filing so you can focus on running your business while staying tax compliant.

About Ebizfiling -

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]