-

June 29, 2026

-

BySteffy A

Section 43B(h) for MSME Payments: Compliance and Tax Impact

Introduction

Section 43B(h) provides that payments due to Micro and Small Enterprises for goods supplied or services rendered are allowed as deductions only when paid within the timelines prescribed under the MSMED Act, 2006. However, delayed payments will be allowed as a deduction in the financial year in which the payment was made. It addresses the issue of working capital scarcity in the MSME industry and promotes prompt payments to Micro and Small Enterprises. Under the Income Tax Act 2025, Section 43B(h) for MSME Payments has been renumbered as Section 37(2)(g), while its core objective remains unchanged.

In this article, we will discuss the applicability of Section 43B(h), who it applies to, the applicable payment due dates, and its tax implications.

Section 43B(h) for MSME Payments

Section 43B generally allows certain deductions only on an actual payment basis. Clause (h) specifically covers payments due to Micro and Small Enterprises registered under the MSMED Act.

Under this clause, any sum payable to a registered Micro or Small Enterprise will be allowed as a deduction only if it is paid within the time limits prescribed under the MSMED Act.

If payment is delayed beyond the prescribed timeline, the deduction is allowed only in the year in which the actual payment is made. Under the Income tax Act, 2025, Section 43B(h) for MSME Payments has been renumbered as Section 37(2)(g), while the underlying principle of allowing deduction on timely payment remains unchanged.

To understand the provisions and applicability in detail, read our guide on Section 37 of the Income Tax Act 2025.

To Whom Does Section 43B(h) Apply?

Section 43B(h) applies only to payments made to Micro and Small Enterprises (MSEs) that are registered under the MSMED Act and hold a valid Udyam Registration Certificate. The provision becomes applicable when a business purchases goods or avails services from such suppliers. It does not apply to Medium Enterprises, even if they are registered under the MSMED Act.

MSME Payment Due Date Under Section 43B(h)

The payment timelines under Section 43B(h) for MSME Payments are governed by Section 15 of the MSMED Act, 2006:

- Within 15 days: When there is no written agreement between the buyer and the supplier.

- Within the agreed period (maximum 45 days): When a written agreement exists between the parties.

If payment is made beyond the prescribed timeline, the related expense cannot be claimed as a deduction in the same financial year and will be allowed only in the year of actual payment.

|

Particulars |

Payment Within Due Date |

Payment After Due Date |

|

Deduction Availability |

Same Financial Year | Year of Actual Payment |

| Tax Impact | No Disallowance |

Expense Disallowed Temporarily |

|

Taxable Income |

Lower | Higher |

| MSMED Compliance | Compliant |

Non-Compliant |

Tax Implications of Section 43B(h) for MSME Payments

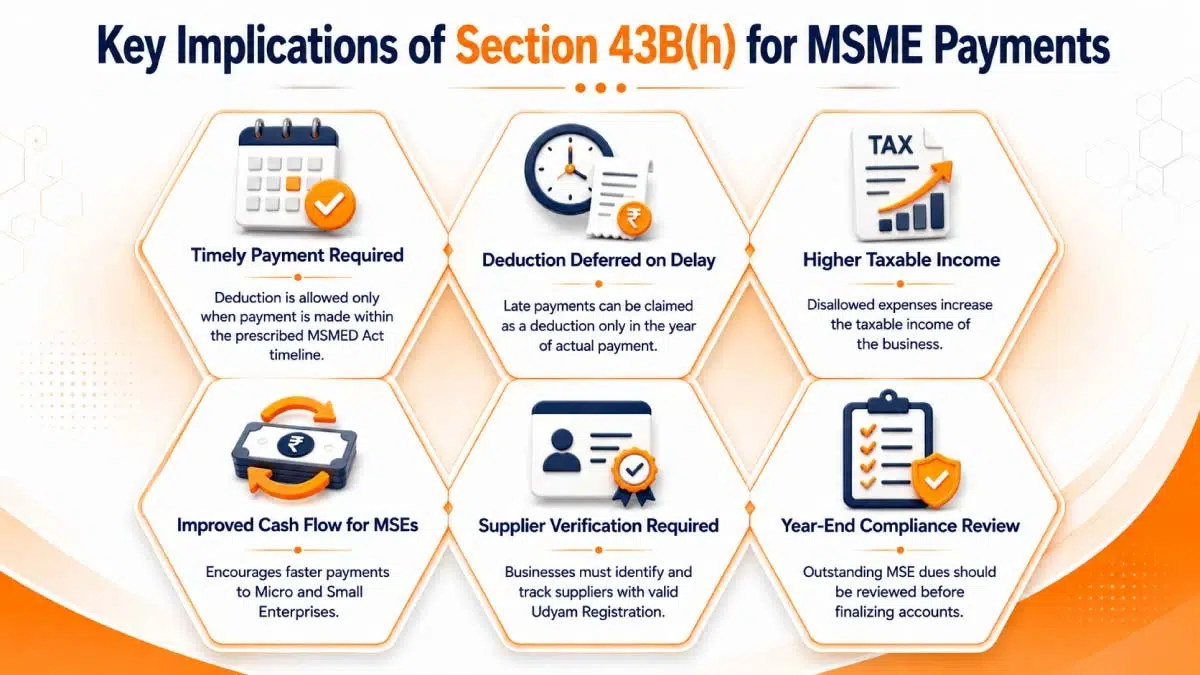

The introduction of Section 43B(h) for MSME Payments has changed how businesses manage payments to Micro and Small Enterprises (MSEs). What was once treated as a routine credit period can now directly affect a company’s taxable income. Some of the key implications of this provision are:

Deduction Depends on Timely Payment:

Businesses can claim a deduction for payments made to eligible MSE suppliers only if the payment is made within the timelines prescribed under the MSMED Act. If the payment is delayed, the deduction is postponed until the year in which the actual payment is made.

Higher Taxable Income in Case of Delay:

When an outstanding payment is disallowed under Section 43B(h), the corresponding expense is added back while computing taxable income. This may increase the tax liability of the business for that financial year.

Stronger Cash Flow for MSEs:

The provision was introduced to address the problem of delayed payments faced by Micro and Small Enterprises. Timely payments help these businesses maintain working capital and meet their day-to-day operational expenses.

Need for Better Vendor Tracking:

Businesses must identify which suppliers are registered as Micro or Small Enterprises and maintain updated records of their Udyam Registration details. This has made vendor classification an important part of tax compliance.

Changes in Credit and Payment Policies:

Many businesses that previously operated on longer credit cycles may need to revisit their payment terms to ensure compliance with the MSMED Act timelines and avoid deduction-related issues.

Greater Focus During Year-End Compliance:

Before finalizing accounts, businesses must review outstanding balances payable to eligible MSE suppliers and determine whether any disallowance under Section 43B(h) is required. This has become an important year-end tax compliance check.

To understand the broader provisions and deductions covered under Section 43B, read our detailed guide on Section 43B of the Income Tax Act.

Stay Compliant with Section 43B(h) Through Ebizfiling

The applicability of Section 43B(h) depends on whether your suppliers qualify as Micro or Small Enterprises under the MSMED Act. Ebizfiling helps businesses identify eligible suppliers and assess the impact of delayed payments on tax deductions.

- Verification of supplier Udyam Registration details

- Review of payments that may be subject to Section 43B(h) disallowance

- Guidance on MSMED Act payment timelines

- Assessment of year-end outstanding balances

- Support in tax and compliance reporting

Section 43B(h) applicability depends on the MSME status of your suppliers. Check our MSME Registration (Udyam Registration) service and get expert guidance from Ebizfiling to stay compliant and avoid tax disallowances.

Conclusion

Section 43B(h) for MSME Payments has made timely payment to Micro and Small Enterprises an important tax compliance requirement for businesses. Since the deduction of eligible expenses is now linked to payment within the timelines prescribed under the MSMED Act, delayed payments can result in tax disallowances and higher taxable income. Businesses should therefore review the applicability of Section 43B(h), monitor payment due dates, and maintain proper records of suppliers holding valid Udyam Registration. A proactive approach to compliance can help businesses avoid deduction-related issues, ensure accurate Income Tax Return Filing, and maintain proper tax reporting throughout the financial year.

FAQs on Section 43B(h) for MSME Payments

File Income Tax Returns

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling at INR 1199/- only.

About Ebizfiling -

Reviews

Ashrith Akkana

19 Apr 2022I took import export certificate from the ebizfiling. They have done the work on time.. Thank you for making my import export certificate in time 😊

Hemang Malhotra

08 Oct 2018I was new as an Entrepreneur when I had seen their post on social media. I contacted them regarding proprietorship and realized they their pricing is incomparable in the market also their services are really prompt. Thank you, Ebizfiling.

Kunal Undirwade

04 Apr 2022I registered my company from Ebizfilling. I have had a great experience with them. Their services and work are very beautiful and understandable to everyone. At first I thought that these people would work or not and I was skeptical about how they would work properly. But here I was very much assisted by Divya Gehlot and Madam Sejal. I am very happy with the service / help provided by them and I wish them success in their endeavors. Also my best wishes to the entire Ebizfilling team

June 29, 2026 By Steffy A

Section 37 of the Income Tax Act 2025: Actual Payment Deductions Introduction Section 37 of the Income Tax Act 2025 governs certain business deductions that can be claimed only when the actual payment is made, regardless of the accounting method […]

June 26, 2026 By Steffy A

Updated Return Under Section 263(6) of the Income tax Act 2025 Introduction Section 263(6) of the Income tax Act, 2025 introduces the provisions relating to Updated Returns (ITR-U), allowing taxpayers to voluntarily correct errors, disclose omitted income, or update previously […]

June 29, 2026 By Steffy A

Section 63 of the Income Tax Act 2025: Tax Audit Applicability Overview Section 63 of the Income-Tax Act, 2025 is the new provision governing tax audit requirements in India. It replaces Section 44AB of the Income Tax Act, 1961 and […]