-

June 26, 2026

-

BySteffy A

Updated Return Under Section 263(6) of the Income tax Act 2025

Introduction

Section 263(6) of the Income tax Act, 2025 introduces the provisions relating to Updated Returns (ITR-U), allowing taxpayers to voluntarily correct errors, disclose omitted income, or update previously filed tax information. The provision continues the concept earlier available under Section 139(8A) of the Income-tax Act, 1961, while reorganizing return filing rules under the new legislation. Understanding the eligibility conditions, filing timeline, and restrictions under Section 263(6) is essential for taxpayers who wish to rectify past omissions and maintain tax compliance.

This guide explains the applicability, key provisions, and practical implications of filing an Updated Return under the Income tax Act, 2025.

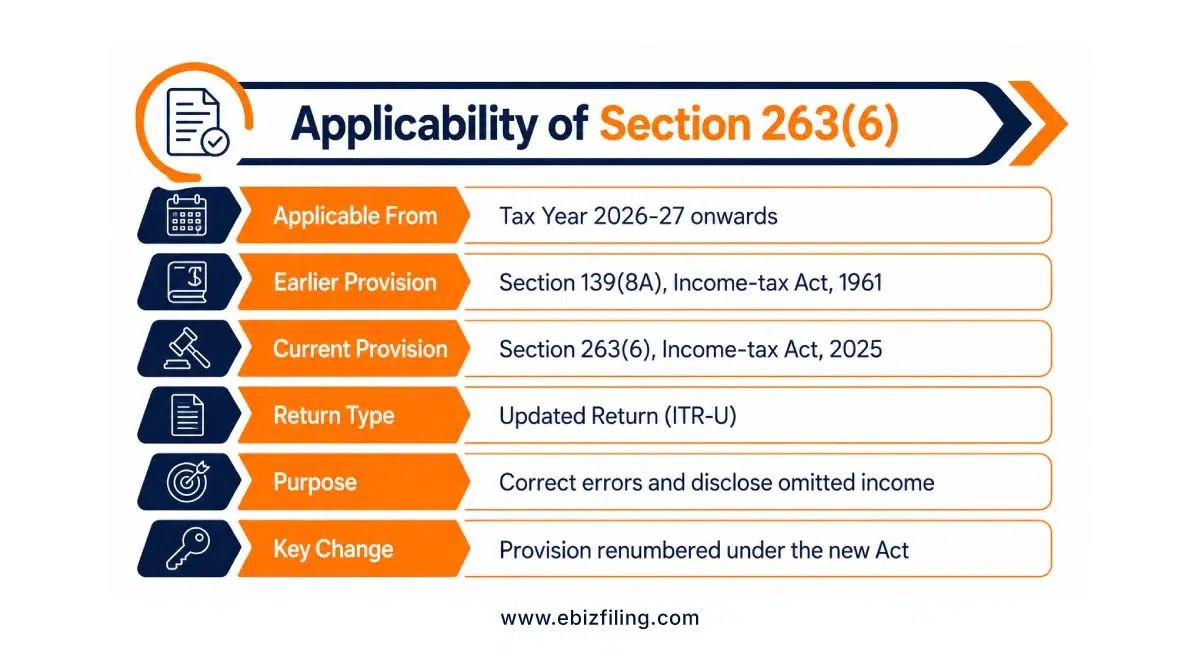

Applicability of Section 263(6) of the Income Tax Act, 2025

The provisions relating to Updated Returns under Section 263(6) of the Income tax Act, 2025 apply from Tax Year 2026-27 onwards. The Income-tax Act, 2025 has reorganized and consolidated various return filing provisions that were previously contained under Section 139 of the Income-tax Act, 1961. As part of this legislative restructuring, the provisions governing Updated Returns have been incorporated under Section 263(6) of the Income tax Act, 2025.

Taxpayers filing returns for periods governed by the Income tax Act, 1961 may continue to refer to Section 139(8A) and the corresponding provisions relating to Form ITR-U. However, for tax periods covered by the Income tax Act, 2025, Updated Returns will be governed by Section 263(6). Although the section number has changed, the objective of allowing taxpayers to rectify omissions voluntarily and update previously filed tax information continues under the new legislation.

Comparison Between Section 139(8A) vs Section 263(6) of the Income Tax Act 2025

|

Particulars |

Section 139(8A) of the Income tax Act, 1961 |

Section 263(6) of the Income tax Act, 2025 |

|

Applicable Act |

Income tax Act, 1961 | Income tax Act, 2025 |

| Provision | Updated Return (ITR-U) under Section 139(8A) |

Updated Return (ITR-U) under Section 263(6) |

|

Purpose |

Allows taxpayers to voluntarily disclose omitted income or correct errors after the prescribed filing deadline. | Continues the same framework for voluntary correction of omissions and disclosure of additional income. |

| Time Limit | Within the prescribed period applicable under the Income tax Act, 1961. |

Within 48 months from the end of the financial year succeeding the relevant tax year. |

|

Refund Claim |

Not permitted. | Not permitted. |

| Reduction of Tax Liability | Not allowed. |

Not allowed. |

|

One Updated Return Rule |

Only one Updated Return can be filed for an assessment year. | Only one Updated Return can be filed for a tax year. |

| Search/Survey Restriction | Filing is restricted in specified cases involving search, survey, requisition, or other proceedings. |

Filing is restricted in cases involving search, survey, requisition, and other situations specified under Section 263(6). |

|

Legislative Position |

Original provision introduced under the Income tax Act, 1961. |

Renumbered and consolidated under Section 263 of the Income tax Act, 2025. |

Key Compliance Considerations Under Section 263(6) of the Income tax Act, 2025

Section 263(6)(a): Eligibility to File an Updated Return

Any person may file an Updated Return (ITR-U), regardless of whether an original, belated, or revised return has been filed for the relevant tax year. The updated return may be filed for the taxpayer’s own income or for income of another person for which the taxpayer is assessable under the Act. The return can be furnished within the prescribed time limit.

Section 263(6)(b): Special Cases Where an Updated Return Is Permitted

Section 263(6)(b)(i): Filing an Updated Return for Loss Cases

A taxpayer who has filed a loss return within the due date may furnish an Updated Return if it converts the loss into income or reduces the amount of loss originally reported.

Section 263(6)(b)(ii): Filing an Updated Return in Response to a Notice

An Updated Return may also be filed in response to a notice issued under Section 280, subject to the conditions and time period specified in the notice.

Section 263(6)(c): Situations Where an Updated Return Cannot Be Filed

Section 263(6)(c)(i): Updated Return Resulting in a Loss

An Updated Return cannot be filed if it results in a loss for the relevant tax year, except in cases specifically permitted under Section 263(6)(b)(i).

Section 263(6)(c)(ii): Reduction in Tax Liability

The facility cannot be used if the Updated Return reduces the total tax liability determined based on the original, belated, or revised return.

Section 263(6)(c)(iii): Refund Claims or Increased Refunds

An Updated Return cannot be filed if it creates a refund where none existed earlier or increases the refund already claimed.

Section 263(6)(c)(iv): Multiple Updated Returns Not Permitted

A taxpayer can file only one Updated Return for a particular tax year. Once filed, another Updated Return for the same year is not allowed.

Section 263(6)(c)(v): Pending or Completed Proceedings

An Updated Return generally cannot be filed if assessment, reassessment, recomputation, or revision proceedings are pending or have already been completed for the relevant tax year, except where specifically permitted by law.

Section 263(6)(c)(vi): Information Regarding Violation of Specified Laws

The facility is unavailable if the Assessing Officer possesses information relating to violations of specified laws and such information has been communicated to the taxpayer before filing the Updated Return.

Section 263(6)(c)(vii): Information Received Under International Agreements

An Updated Return cannot be filed where information relating to the taxpayer has been received under tax information exchange agreements and communicated before the return is furnished. Individuals with foreign income should also understand the applicability of DTAA Benefits and international information-sharing provisions while evaluating their tax reporting obligations.

Section 263(6)(c)(viii): Prosecution Proceedings Initiated

The facility is not available if prosecution proceedings under Chapter XXII have already been initiated for the relevant tax year.

Section 263(6)(c)(ix): Cases Involving Show-Cause Notice Under Section 281

Where more than 36 months have elapsed and a show-cause notice under Section 281 has been issued, the taxpayer may not be eligible to file an Updated Return, unless otherwise permitted under the Act.

Section 263(6)(c)(x): Persons Notified by the Board

The CBDT may notify certain persons or classes of persons who will not be eligible to file an Updated Return.

Section 263(6)(d): Cases Involving Search, Survey, or Requisition

A taxpayer is not eligible to file an Updated Return if a search under Section 247, requisition under Section 248, or specified survey under Section 253 has been conducted. This restriction applies to the relevant tax year and certain preceding years covered by such proceedings.

Section 263(6)(e): Impact on Carried Forward Losses, Depreciation, and Tax Credits

Where filing an Updated Return results in a reduction of carried forward losses, unabsorbed depreciation, or tax credits available in subsequent years, the taxpayer must also file Updated Returns for the affected subsequent tax years to ensure consistency in tax records.

Ebizfiling Assistance for Accurate ITR-U Filing

- We help determine whether you qualify to file an Updated Return (ITR-U) under Section 263(6) of the Income tax Act, 2025.

- Our experts assist in calculating the additional tax, interest, and other applicable charges before filing by using Ebizfiling’s tax calculation tools.

- We help prepare and review the Updated Return to ensure accurate reporting of income and disclosures.

- Get support in understanding restrictions, due dates, and filing conditions applicable to Updated Returns.

- From document review to successful submission, our team assists you throughout the ITR-U filing process.

File your Income Tax Return accurately and on time with expert assistance from Ebizfiling. Contact us today to get started.

Final Thoughts

Section 263(6) of the Income tax Act, 2025 provides taxpayers with an opportunity to voluntarily correct omissions and update previously filed tax information through an Updated Return (ITR-U). While the provision continues the framework previously available under Section 139(8A) of the Income tax Act, 1961, it also lays down specific eligibility conditions and restrictions that must be carefully considered before filing. Taxpayers should review their tax records, assess the impact of additional tax liabilities, and ensure compliance with the prescribed timelines. Filing an Updated Return correctly can help improve tax accuracy and reduce the risk of future disputes with the tax authorities.

Frequently Asked Questions

1. Can an Updated Return be filed under Section 263(6) of the Income tax Act, 2025 if no original return was filed?

Section 263(6) of the Income tax Act, 2025 allows a taxpayer to file an Updated Return (ITR-U) even if an original, belated, or revised return was not filed for the relevant tax year, subject to the prescribed eligibility conditions and restrictions.

2. What is the ITR-U due date under Section 263(6) of the Income tax Act, 2025?

Under Section 263(6) of the Income tax Act, 2025, an Updated Return can generally be filed within 48 months from the end of the financial year succeeding the relevant tax year. Taxpayers seeking assistance with ITR-U filing under the Income tax Act, 2025 may consult Ebizfiling to understand the applicable timeline and compliance requirements.

3. Can an Updated Return (ITR-U) be used to claim a higher income tax refund?

The Updated Return (ITR-U) under Section 263(6) of the Income-tax Act, 2025 cannot be used to claim a refund where none existed earlier or to increase an already claimed refund. The provision is primarily intended for voluntary disclosure of omitted income and correction of tax information.

4. Is it possible to file more than one Section 263(6) Updated Return for the same tax year?

As per the Section 263(6) of the Income tax Act, 2025 return filing rules, only one Updated Return can be furnished for a particular tax year. Once an ITR-U has been filed, another Updated Return for the same tax year is not permitted.

5. Can a taxpayer file an Updated Return after receiving a notice under Section 280?

Section 263(6)(b)(ii) permits the filing of an Updated Return in response to a notice issued under Section 280, provided the return is furnished within the time period and conditions specified in the notice.

6. Can a loss return be converted into an income return through an Updated Return?

A taxpayer who has filed a loss return within the prescribed due date may file an Updated Return if it converts the reported loss into income or reduces the amount of loss originally declared, subject to the Updated Return eligibility conditions.

7. What happens if an Updated Return affects carried forward losses or unabsorbed depreciation?

If filing an Updated Return under the Income tax Act, 2025 results in a reduction of carried forward losses, unabsorbed depreciation, or eligible tax credits, Updated Returns may also need to be filed for the affected subsequent tax years to maintain consistency in tax records.

8. Can an Updated Return be filed after assessment proceedings have been completed?

An Updated Return cannot be filed where assessment, reassessment, recomputation, or revision proceedings are pending or have already been completed for the relevant tax year, except in specific situations permitted under the Act.

9. Who can file an Updated Return under Section 263(6)?

Any taxpayer may file an Updated Return (ITR-U) under Section 263(6) of the Income-tax Act, 2025, irrespective of whether an original, belated, or revised return was filed. However, eligibility is subject to various restrictions relating to refunds, tax reductions, prosecution, search proceedings, and other specified circumstances.

10. What is the difference between an Updated Return and a Revised Return?

A Revised Return is filed to correct mistakes in a return already submitted within the permitted revision period. An Updated Return (ITR-U) under Section 263(6) can be filed even after the revised return deadline has expired and may be used to voluntarily disclose omitted income, subject to the conditions prescribed under the Income-tax Act, 2025.

File Your Income Tax Return with Confidence

Our tax experts help individuals and businesses file their Income Tax Returns accurately and on time through a simple online process.

About Ebizfiling -

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]