Form 130 under the Income Tax Act for Salary TDS Certificate

Introduction

Form 130 under the Income Tax Act is the new TDS certificate for salary, pension, and specified senior citizen interest income. It replaces Form 16 from Tax Year 2026-27. It is issued by the employer and contains quarter-wise details of tax deducted at source (TDS), salary breakup, deductions, and tax deposited.

Under Section 395(4)(b) of the Income Tax Act, 2025, read with Rule 215(1) of the Income Tax Rules, 2026, Form 130 applies from Tax Year 2026-27. For FY 2025-26, employees will continue to receive Form 16. Form 130 applies from Tax Year 2026-27 onwards.

In this blog, we will cover what Form 130 is, how Form 130 replaces Form 16, the difference between Form 130 vs Form 16, and how to download Form 130.

What is Form 130 under the Income Tax Act?

Form 130 under the Income Tax Act is an annual certificate for Tax Deducted at Source (TDS), issued by the employer to a salaried employee or pensioner after the end of the tax year. It contains a detailed summary of salary earned, tax deducted and deposited, and applicable deductions.

This certificate serves as proof that tax has been deducted from salary income and deposited with the Government. It also enables the deductee to claim credit of TDS deducted and deposited on their behalf while filing the Income Tax Return.

Form 130 also applies to interest income earned by specified senior citizens as per Section 402(39) of the Income Tax Act, 2025.

Therefore, Form 130 under the Income Tax Act replaces Form 16, which was earlier issued under Section 203 of the Income Tax Act, 1961, read with Rule 31 of the Income Tax Rules, 1962.

Form 130 vs Form 16 : Key Differences

|

Basis |

Form 130 |

Form 16 |

|

Applicable Law |

Issued under the Income Tax Act, 2025 |

Issued under the Income Tax Act, 1961 |

|

Relevant Section |

Section 395(4)(b) |

Section 203 |

|

Relevant Rule |

Rule 215(1) of the Income Tax Rules, 2026 |

Rule 31 of the Income Tax Rules, 1962 |

|

Purpose |

TDS certificate for salary, pension, and specified senior citizen income where applicable |

TDS certificate mainly for salary income |

|

Issued By |

Employer or specified bank, as applicable |

Employer |

|

Issued To |

Salaried employee, pensioner, or specified senior citizen |

Salaried employee |

|

Structure |

Divided into Part A, Part B, and Part C |

Divided into Part A and Part B |

|

Details Covered |

Employer or bank details, employee or senior citizen details, TDS reconciliation, income computation, deductions, and tax payable |

Employer and employee details, salary breakup, deductions, and TDS details |

|

Mode of Issue |

Must be downloaded from TRACES and issued after signing digitally or manually |

Generally issued by the employer after TDS deduction |

|

Applicability |

Applies from Tax Year 2026-27 onwards |

Applies up to the current filing season for FY 2025-26 |

|

ITR Use |

Helps claim TDS credit and verify income while filing ITR |

Helps claim TDS credit and file ITR |

Structure of Form 130 under the Income Tax Act

Form 130 under the Income Tax Act has three parts, namely Part A, Part B and Part C. Each part covers different details related to the deductor, deductee, income paid or credited, tax deducted at source, and taxable income computation.

Part A: Employer, Bank and Deductee Details

Usually, Part A contains the details of the employer or specified bank and the details of the employee or specified senior citizen to whom Form 130 is issued.

Part B: TDS Reconciliation Details

Here, Part B contains a summary-level reconciliation of the amount paid or credited and the tax deducted at source. It helps show how much income was paid and how much TDS was deducted.

Part C: Income Computation and Annexures

In Part C has two annexures, Annexure-I and Annexure-II.

Annexure-I applies where tax is deducted from salary income of employees under Section 392. It includes break-up of gross salary, exemptions, deductions, total taxable income, tax payable, relief under Section 157, TDS/TCS paid, and net tax payable.

Annexure-II applies to specified senior citizens where tax is deducted under Section 393(1), Table Sl. No. 8(iii). It includes pension income, interest income under the head “Other Sources”, deductions, total taxable income, tax payable, relief under Section 157, and net tax payable.

Form 130 is also part of the new TDS and TCS forms introduced under the Income Tax Act, 2025 to update tax deduction reporting and certificate issuance.

Who Should Issue Form 130?

Form 130 must be issued by the employer or specified bank responsible for deducting tax under the applicable provisions.

In case of salary income, the employer responsible for deducting tax under Section 392 is required to issue Form 130 to the employee.

In case of pension or interest income of a specified senior citizen, the specified bank responsible for deducting tax under Section 393(1), Table Sl. No. 8(iii), is required to issue Form 130 under the Income Tax Act.

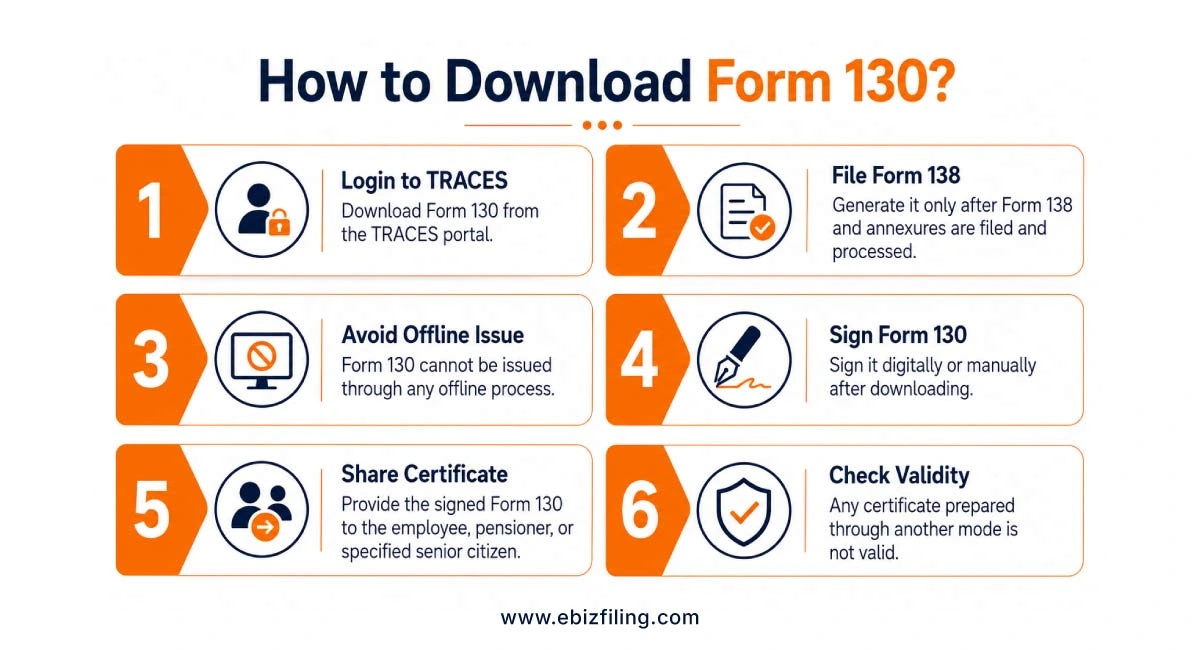

How to Download Form 130 under the Income Tax Act?

- Form 130 must be downloaded by the employer or specified bank from the TRACES website.

- It can be generated only after the relevant quarterly TDS statement in Form 138 and supporting annexures are filed and processed.

- Form 130 cannot be issued through any offline or separate process.

- After downloading Form 130, the employer or specified bank must sign it digitally or manually.

- The signed Form 130 must then be provided to the employee, pensioner, or specified senior citizen, as applicable.

- Any certificate prepared through any other mode or process will not be treated as a valid Form 130.

Due Date and Correction Process for Form 130

|

Particular |

Details |

|

Due Date |

Form 130 under the Income Tax Act must be issued on or before 15th June after the end of the tax year in which income was paid and TDS was deducted. |

|

Correction Requirement |

If there is any mistake in Form 130, the employer must file a revised TDS statement in Form 138 within the prescribed time. |

|

After Processing |

Once the revised TDS statement is processed, the employer can download and issue the corrected Form 130 to the employee. |

|

Record Purpose |

Form 130 is not required to be attached with the Income Tax Return, but it should be preserved for records and TDS credit claim. |

Employers, businesses, and deductors should also follow the TDS and TCS compliance calendar FY 2026-27 to track return filing due dates, certificate issuance timelines, and other important TDS compliance requirements.

Get Expert Assistance for TDS Compliance

Ebizfiling India Pvt Ltd can help employers, businesses, and deductors manage TDS compliance properly. Our team can assist with:

- Timely and accurate filing of quarterly TDS returns

- Correction of errors through revised TDS statements

- Proper documentation for income tax compliance

- Support in helping employees and vendors claim correct TDS credit

- Ebizfiling offers expert support for TDS return filing, corrections, and compliance management.

Conclusion

Form 130 under the Income Tax Act is an important TDS certificate for salaried employees, pensioners, and specified senior citizens earning eligible interest income. It replaces the earlier Form 16 from Tax Year 2026-27 and provides details of income earned, tax deducted, tax deposited, deductions, and taxable income. Since Form 130 can be generated only after the relevant TDS statements are filed and processed, employers and specified banks must ensure accurate and timely TDS compliance. Employees should also preserve Form 130 for claiming TDS credit and for future income tax records.

Frequently Asked Questions

1. Can a deductor issue Form No. 130 without filing the TDS statement?

No. A deductor cannot issue Form No. 130 without filing the quarterly TDS statement. The certificate is generated only after the TDS statement is filed and processed. Form 130 is issued based on the processing of quarterly TDS statements in Form No. 138 along with the relevant annexures.

2. Under which section is Form 130 issued?

Form 130 under the Income Tax Act is issued under Section 395(4)(b) of the Income Tax Act, 2025, read with Rule 215(1) of the Income Tax Rules, 2026. It replaces Form 16, which was earlier issued under Section 203 of the Income Tax Act, 1961.

3. Can employees directly download Form 130 from the Income Tax portal?

No. Employees cannot directly download Form 130 from the Income Tax portal. The employer or specified bank must download it from TRACES and issue the signed certificate to the employee, pensioner, or specified senior citizen.

4. How to Download Form 130 from TRACES?

Form 130 under the Income Tax Act must be downloaded by the employer or specified bank from the TRACES website after the relevant quarterly TDS statement in Form 138 is filed and processed. After downloading, it must be signed digitally or manually before being issued.

5. Can Form No. 130 be issued offline?

No. The employer or specified bank must mandatorily download it from the TRACES website and provide the same to the deductee after signing it digitally or manually. The certificate prepared by any other mode or process will not be a legal or valid TDS certificate in Form No. 130.

6. What is the due date for issuing Form 130?

Form 130 under the Income Tax Act must be issued by 15th June of the financial year immediately following the tax year in which the income was paid and tax was deducted.

7. What happens if there is an error in Form 130?

If there is any error in Form 130, the employer must file a revised TDS statement in Form 138 within the prescribed time. Once the revised statement is processed, the corrected Form 130 can be downloaded and issued.

8. How is Form 130 vs Form 16 different for employees?

Form 130 vs Form 16 mainly differs in legal reference, structure, and reporting format. Form 130 is issued under the Income Tax Act, 2025 and has Part A, Part B, and Part C, while Form 16 was issued under the Income Tax Act, 1961 and had Part A and Part B.

9. Can Ebizfiling help with Form 130 related TDS compliance?

Yes. Ebizfiling can assist employers with quarterly TDS return filing, TDS correction filing, and compliance support required for issuing valid TDS certificates. Proper TDS filing helps employees claim correct TDS credit while filing ITR.

10. Does Ebizfiling help if Form 130 has wrong salary or TDS details?

Yes. If Form 130 under the Income Tax Act contains incorrect salary, deduction, or TDS details, Ebizfiling can help with TDS Return Filing & Revision and revised statement support. Once the revised TDS statement is processed, the employer can issue the corrected Form 130.

File Your TDS Return with Confidence

Avoid TDS filing errors and meet due dates with reliable TDS Return filing assistance from experts.

About Ebizfiling -

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]

July 30, 2026 By Steffy A

Section 133 of the Income Tax Act, 2025: Donation Deduction Introduction Section 133 of the Income Tax Act, 2025 allows taxpayers to claim a deduction for monetary donations made to specified funds, charitable institutions, government bodies and approved organizations. The […]