-

July 4, 2026

-

BySteffy A

Form 10A of the Income Tax Act: Filing Guide and Eligibility

Introduction

Form 10A of the Income Tax Act is the online application that eligible trusts, societies, institutions, hospitals, and other non-profit organizations use to apply for registration or approval to claim Tax exemption under the Income Tax Act. The form must be submitted online to the Principal Commissioner or the Commissioner authorized by the CBDT through the Income Tax e-Filing Portal in the prescribed format. Filing Form 10A enables eligible organizations to obtain or continue their registration and claim the tax benefits available under the Income Tax Act.

In this article, you’ll learn about the purpose of Form 10A, eligibility, required documents, the filing procedure, and the key changes introduced under the Income Tax Act, 2025.

What is Form 10A of the Income Tax Act?

Form 10A is the prescribed online application through which eligible charitable and religious organizations apply for registration, provisional registration, or approval under the Income Tax Act. The form is filed online through the Income Tax e-Filing Portal along with the prescribed documents and organizational details. The form commonly used to apply for registration, provisional registration, or approval under Sections 12AB, 80G, and certain provisions of Section 10(23C).

Form 10A has been renumbered as Form 104 under the Income Tax Act, 2025. However, taxpayers may still come across references to Form 10A while dealing with registrations granted under the earlier law.

Benefits of Filing Form 10A of the Income Tax Act

- Enables eligible organizations to obtain registration under Sections 12AB, 80G, and other applicable exemption provisions.

- Allows registered organizations to claim the tax exemption benefits available under the Income Tax Act.

- Meets the mandatory registration requirements prescribed under the applicable provisions of the Act.

- Enhances credibility among donors, CSR contributors, government authorities, and other stakeholders.

- Supports timely compliance, helping reduce delays and avoid unnecessary departmental queries.

If you are applying as a charitable organization, you can also learn about the 12A and 80G Registration for NGOs and the complete registration process.

Who should file Form 10A of the Income Tax Act?

|

Entity Type |

Purpose of Filing Form 10A |

|

Trusts |

To obtain registration, re-registration, or provisional registration under Section 12AB and claim tax exemption benefits. |

|

Societies |

To apply for provisional registration or registration, wherever applicable. |

| Charitable Institutions |

To seek registration or approval under the applicable provisions of the Income Tax Act. |

|

Religious Organizations |

To obtain tax-exempt status and continue availing of benefits available under the Act. |

| Educational Institutions |

To apply for approval under the relevant provisions governing tax exemptions. |

|

Hospitals and Medical Institutions |

To obtain or renew registration for claiming income tax exemptions, wherever eligible under the applicable provisions. |

| Funds and Other Non-Profit Organizations |

To secure the registration, approval, or renewal required for availing tax exemption benefits. |

Organizations that have not yet been legally established should first complete the Trust Registration process before applying for registration under Sections 12AB and 80G.

Documents Required for Filing Form 10A of the Income Tax Act

The following are the Documents Required for Filing Form 10A under the Income Tax Act.

1. Trust Deed, Memorandum of Association (MOA), or other constitutional documents of the trust, society, institution, or Section 8 company.

2. Registration certificate issued by the relevant authority, such as the Registrar of Societies, Registrar of Companies (ROC), or Registrar of Public Trusts.

3. Permanent Account Number (PAN) of the trust, society, institution, or Section 8 company.

4. Copy of the existing registration or approval order, wherever applicable.

5. Self-certified copies of the annual accounts and financial statements for up to the previous three financial years, wherever applicable.

6. A brief note describing the activities carried out by the organization.

7. Documents evidencing the adoption or modification of the organization’s objects, if any changes have been made.

8. FCRA Registration Certificate, if the organization is registered under the Foreign Contribution (Regulation) Act, 2010.

9. Copy of any order rejecting an earlier application for registration under Sections 12A, 12AA, or 12AB, wherever applicable.

10. Accounts and audit reports relating to any business undertaking carried on by the trust or institution, wherever permitted under the Income Tax Act.

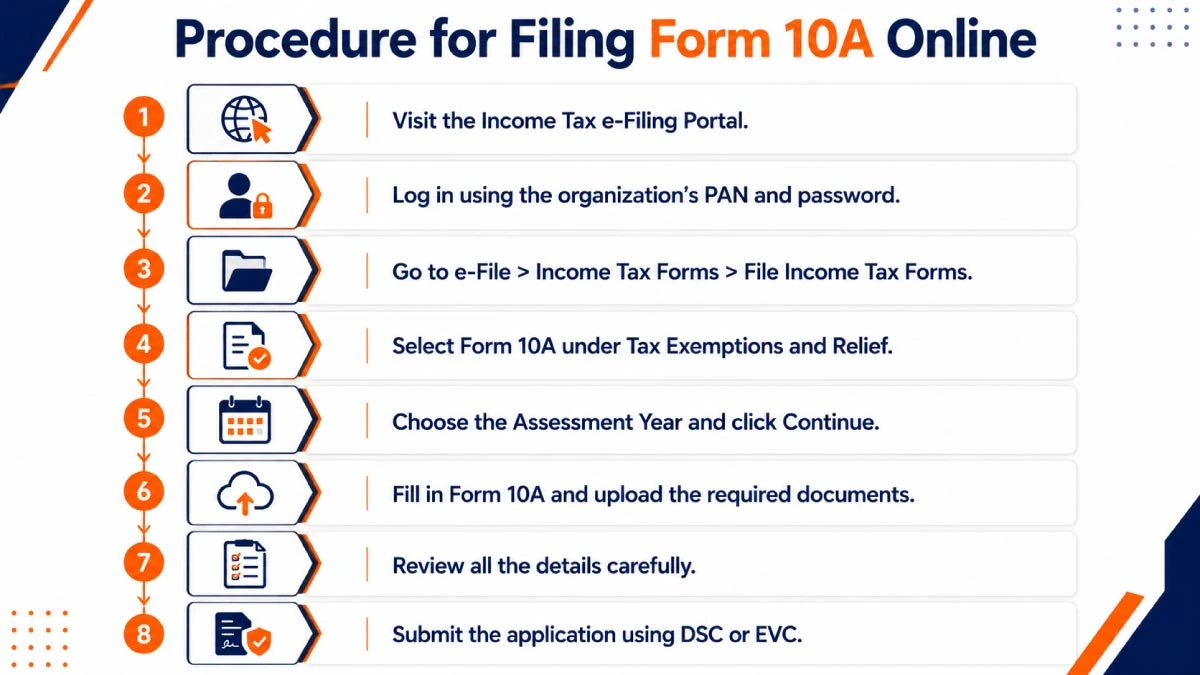

Procedure for Filing Form 10A of the Income Tax Act

1. Visit the Income Tax e-Filing Portal at https://www.incometax.gov.in.

2. Log in using the PAN of the organization as the User ID and enter the password.

3. Click e-File > Income Tax Forms > File Income Tax Forms.

4. Under the Income Tax Act, 1961, select Form 10A. For filings under the Income Tax Act, 2025, select Form 104 (Erstwhile Form 10A), wherever applicable.

5. The organization’s PAN details, Submission Mode (Online), and Filing Type (Original) will be auto-populated.

6. Select the applicable Assessment Year (or Tax Year under the Income Tax Act, 2025).

7. Open the form, enter the required details, upload the prescribed documents, review the information carefully, and then submit the application.

8. After verifying all details, submit the application using DSC or EVC, whichever is applicable.

Form 10A Filing Guidance by Ebizfiling

Errors in documents, incorrect registration details, or incomplete information can delay approval or lead to additional queries from the Income Tax Department.

Ebizfiling supports organizations by:

- Assessing eligibility for registration under Sections 12AB, 80G, and applicable provisions of Section 10(23C).

- Reviewing constitutional documents, registration certificates, and supporting records before filing.

- Assisting with the online filing of Form 10A through the Income Tax e-Filing Portal.

- Preparing and submitting responses to notices or clarification requests from the Income Tax Department.

- Helping trusts, societies, institutions, and other eligible organizations meet registration and ongoing compliance requirements.

We also assist registered trusts with Annual Filing for Trust services to help ensure continued compliance with the Income Tax Act and other applicable regulations.

Final Thoughts

Form 10A of the Income Tax Act helps eligible trusts, societies, and other non-profit organizations obtain or continue registration for tax exemption benefits. Under the Income tax Act, 2025, it has been renumbered as Form 104. Understanding the eligibility, required documents, and filing process helps reduce delays and ensures accurate compliance. Where needed, Ebizfiling India Pvt Ltd can assist with filing and departmental queries.

Frequently Asked Questions

1. Can a newly formed trust apply for Form 10A without any financial statements?

Yes. A newly established trust or institution can apply for provisional registration through Form 10A of the Income Tax Act even if it has not started its activities or prepared audited financial statements. However, it must provide valid constitutional documents and details of its proposed charitable activities.

2. Is Form 10A required if a trust already has a 12A registration certificate?

If your trust has already completed the migration to the Section 12AB regime by filing Form 10A, you normally do not need to file it again. Future renewals or regular registrations are generally made through Form 10AB (Form 105 under the Income-tax Act, 2025).

3. Can a trust apply for 80G approval without obtaining Section 12AB registration?

Although applications for Section 12AB registration and 80G approval can be filed together, obtaining Section 12AB registration is generally necessary before or along with 80G approval. This registration establishes the organization’s eligibility for tax exemption and forms an important basis for seeking 80G approval.

4. Does receiving foreign donations affect Form 10A registration?

Receiving foreign contributions does not prevent an organization from applying through Form 10A of the Income Tax Act. However, if the organization is registered under the Foreign Contribution (Regulation) Act, 2010 (FCRA), details of that registration may need to be disclosed during the application process.

5. What happens if the objectives mentioned in the trust deed change after obtaining registration?

If a trust or institution modifies its objects after registration, it may be required to apply for fresh registration within the prescribed timeline. Significant changes to the charitable objects may affect the validity of the existing registration or approval.

6. Can religious trusts also file Form 10A of the Income Tax Act?

Yes. Religious trusts can apply for registration through Form 10A of the Income Tax Act. However, eligibility for certain tax benefits and donor deductions depends on the applicable provisions of the Income Tax Act and the nature of the organization’s activities.

7. Does the Income Tax Department conduct verification before granting Section 12AB registration?

Yes. The Commissioner of Income-tax (Exemptions) examines the organization’s constitutional documents, objectives, and activities before granting registration. Depending on the application, the department may also request additional information or supporting documents during the verification process.

8. Can Form 10A of the Income Tax Act be revised after submission?

Generally, there is no online facility to revise Form 10A of the Income Tax Act after it has been submitted successfully. However, applicants must follow the correction, withdrawal, or clarification process available on the Income Tax e-Filing Portal, depending on the stage of the application. Ebizfiling can assist with the applicable process and help address any departmental queries, if required.

9. How long does it usually take to receive approval after filing Form 10A?

The time required for approval depends on the type of registration, the completeness of the documents, and whether the Income Tax Department seeks clarification. Ebizfiling helps applicants prepare complete applications to reduce avoidable delays.

10. Why do many Form 10A applications face delays even when all documents are uploaded?

Applications may still be delayed if the uploaded documents are incomplete, contain inconsistencies, or do not match the trust deed, registration records, or the organization’s actual activities. Delays can also occur if notices issued by the Income Tax Department are not responded to within the prescribed time. Ebizfiling helps review documents, file the application accurately, and respond to departmental queries to reduce avoidable registration delays.

Income tax

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling

About Ebizfiling -

Reviews

Dev Desai

19 Nov 2021Loves their services

Jayesh Tejani

28 Aug 2017It is a very professional set up and a really dedicated team. You guys did a great job for my Trademark application in a really short time. All the best to you and your team.

Ratnesh Mishra

19 Nov 2021Awesome work done by this team especially Ms Aishwarya and Mr Deepak....They followed everything on time and service cost was very competitive... Looking forward working with these awesome guys👏👏👏😍

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]