-

June 30, 2026

-

BySteffy A

Form 65 of the Income Tax Act 2025: Patent Tax Benefits

Introduction

Form 65 of the Income Tax Act 2025 is a prescribed application form through which an eligible resident taxpayer can exercise the option to be taxed at a concessional rate of 10% on royalty income derived from a patent developed and registered in India. The form is filed under Section 194(1) (Table: Sl.No. 2) of the Income Tax Act 2025, and forms part of India’s Patent Box Regime, which aims to encourage innovation and research within the country.

The introduction of Form 65 replaces the earlier Form 3CFA that was filed under Section 115BBF of the Income tax Act 1961. Taxpayers opting for this regime can avail of a beneficial tax treatment on eligible patent royalty income, subject to specified conditions and compliance requirements.

In this article, we will discuss what Form 65 of the Income Tax Act 2025 is, its purpose, eligibility criteria, applicability, the filing process, required documents, benefits, and the key differences between Form 65 and Form 3CFA.

What is Form 65 of the Income Tax Act 2025?

Form 65 is an Income tax form used by eligible resident taxpayers to opt for a concessional tax rate of 10% on income earned by way of royalty from a patent developed and registered in India as provided by Section 194(1) (Table: Sl.No. 2) of the Income Tax Act 2025. Form 65 replaces the earlier Form 3CFA filing that was filed under Section 115BBF of the Income Tax Act 1961.

Purpose of Form 65

The primary purpose of filing Form 65 of the Income Tax Act 2025 is to allow eligible taxpayers to avail of a concessional tax treatment on royalty income earned from patents developed and registered in India. By filing this form, a taxpayer can:

- Claim a lower tax rate by paying tax at a concessional rate of 10% (plus surcharge and cess) on the gross amount of royalty income.

- Opt into the Patent Box Regime, which encourages indigenous research and development by providing tax incentives for patents developed and registered in India.

- Forgo other deductions, as no expenditure or allowance can be claimed as a deduction against the royalty income covered under this regime.

- Commit to the regime for the next five tax years, failing which the taxpayer may become ineligible to opt for the regime again for the following five tax years.

Section 194(1) of the Income Tax Act 2025

Section 194(1) of the Income Tax Act 2025 contains special tax provisions for certain types of income that are taxed at prescribed concessional rates, subject to specified conditions. Under Table: Sl. No. 2 of this section, eligible resident taxpayers can opt for a concessional tax rate of 10% on royalty income earned from a patent developed and registered in India.

To avail of this benefit, the taxpayer is required to file Form 65 of the Income Tax Act 2025 and satisfy the conditions prescribed under the Act. The provision forms part of India’s Patent Box Regime, which aims to encourage innovation, research, and the commercialization of intellectual property developed in India.

Who Can File Form 65 of the Income Tax Act 2025?

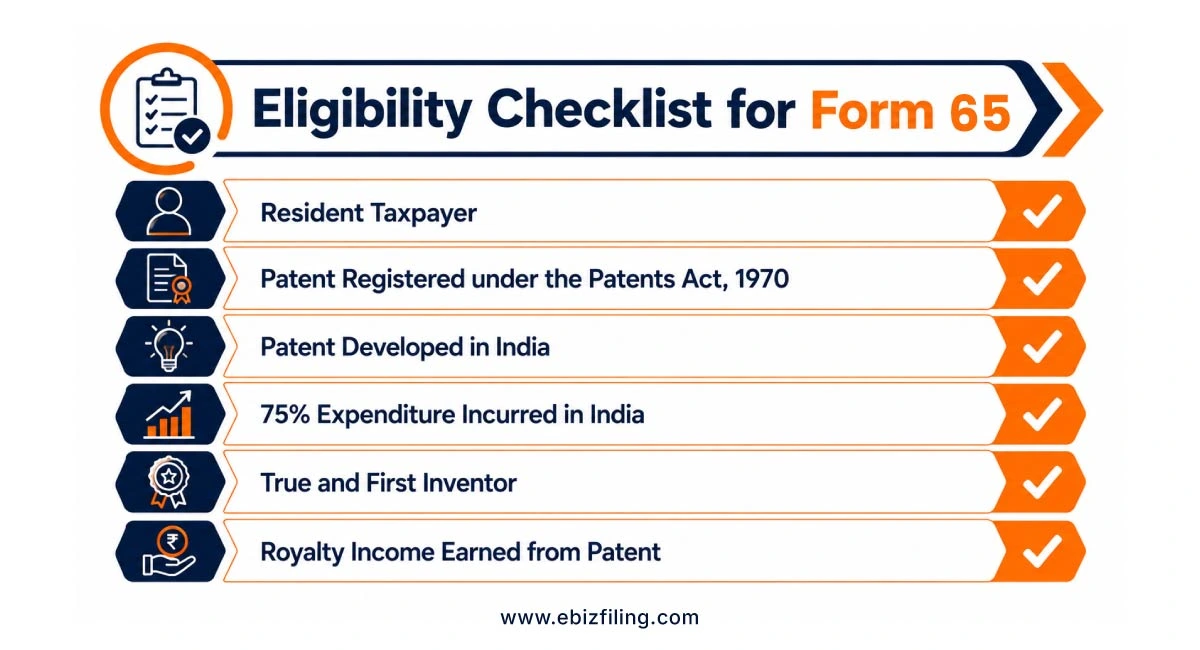

Form 65 can be filed by an eligible resident assessee who earns income by way of royalty from a patent developed and registered in India and wishes to avail the concessional tax regime under Section 194(1) (Table: Sl.No. 2) of the Income Tax Act 2025. The benefit is available only to resident taxpayers. Non-resident individuals or entities are not eligible to opt for this regime.

Eligible Taxpayers

- Individual

- Hindu Undivided Family (HUF)

- Firm

- LLP

- Company

Basic Eligibility Conditions

- The taxpayer must be a resident in India.

- The patent must be developed and registered in India.

- Royalty income must be earned from the eligible patent.

Conditions for Availing Benefits Under Form 65

To claim the concessional tax benefit, the patent must satisfy certain prescribed conditions.

Patent Registered Under the Patents Act, 1970

The patent should be registered under the Patents Act, 1970. The term “patent” carries the same meaning as assigned under section 2(1)(m) of the Patents Act.

Patent Developed in India

The patent is considered to be developed in India only if at least 75% of the total expenditure incurred for the invention has been spent in India by the eligible assessee.

True and First Inventor Requirement

The benefit is available only to the “true and first inventor” whose name appears in the patent register. Where more than one person is registered as a patentee, each qualifying true and first inventor may claim the benefit.

Documents and Information Required for Form 65 Filing

The following documents may be required while filing Form 65 of the Income Tax Act 2025:

- Self-certified copy of the patent grant certificate

- PAN card

- Aadhaar card

- Audited annual accounts

- Bank statements

- Form 26AS

- Details of royalty income

- Details of expenditure incurred on the eligible patent

Taxpayers should also understand their reporting obligations while filing returns. Learn more about Income Tax Return Filing requirements and compliance.

How to File Form 65 of the Income Tax Act 2025?

- Log in to the Income Tax e-Filing Portal using your PAN and password.

- Navigate to e-File > Income Tax Forms and select Form 65.

- Choose the applicable Tax Year.

- Enter the required details, including patent and royalty income information.

- Verify and submit the form using Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

- Download the acknowledgement for future reference.

Note: Form 65 must be filed on or before the due date for filing the return of income for the relevant tax year.

Form 65 vs Form 3CFA: Key Differences

|

Particulars |

Form 3CFA of Income Tax Act 1961 |

Form 65 of the Income Tax Act 2025 |

|

Form Name |

Form 3CFA | Form 65 |

| Applicable Income-tax Act | Income Tax Act 1961 |

Income Tax Act 2025 |

|

Applicable Section |

Section 115BBF | Section 194(1) (Table: Sl.No. 2) |

| Applicable Rule | Rule 5G of the Income-tax Rules, 1962 |

Rule 134 of the Income-tax Rules, 2026 |

|

Purpose |

Option for concessional taxation of patent royalty income | Option for concessional taxation of patent royalty income |

| Tax Benefit | 10% tax rate on eligible patent royalty income |

10% tax rate on eligible patent royalty income |

|

Filing Mode |

Electronic filing | Electronic filing |

| Eligible Taxpayers | Eligible resident taxpayers earning royalty from patents developed and registered in India |

Eligible resident taxpayers earning royalty from patents developed and registered in India |

Professional Assistance for Form 65 Filing

Filing Form 65 requires proper evaluation of eligibility, patent-related conditions, and compliance requirements under Section 194(1) (Table: Sl.No. 2) of the Income Tax Act 2025. Incorrect filing or missing information may affect the availability of the concessional tax benefit on patent royalty income.

At Ebizfiling, we assist taxpayers with Form 65 filing, document review, and compliance support to help ensure accurate and timely submission.

Explore related patent taxation and compliance services:

- Tax on Income from Patent

- Patent Registration Services

- Income Tax Return Filing

- Tax Planning and Advisory Services

Explore our detailed guide on Tax on Income from Patents to understand eligibility, concessional tax rates, royalty income taxation, and compliance requirements for patent holders in India.

Conclusion

Form 65 of the Income Tax Act 2025 provides a valuable tax benefit for eligible resident taxpayers earning royalty income from patents developed and registered in India. By filing Form 65 under Section 194(1) (Table: Sl.No. 2), taxpayers can opt for a concessional tax rate of 10% while benefiting from India’s Patent Box Regime. However, before exercising this option, it is important to understand the eligibility conditions, patent requirements, filing obligations, and long-term commitment associated with the regime. Proper compliance and timely filing can help taxpayers maximize the available tax benefits while avoiding future complications.

Frequently Asked Questions

1. Can a startup claim benefits under Form 65 of the Income Tax Act 2025?

A startup can claim benefits under Form 65 of the Income Tax Act 2025 if it is a resident taxpayer, earns royalty income from a patent developed and registered in India, and satisfies all eligibility conditions prescribed under Section 194(1) of the Income Tax Act 2025.

2. Does Form 65 apply to royalty income from foreign patents?

Form 65 applicability is restricted to royalty income earned from patents developed and registered in India. Royalty income from patents registered outside India is not eligible for the concessional tax regime.

3. What happens if Form 65 filing is not completed before the due date?

If Form 65 of the Income Tax Act 2025 is not filed within the prescribed timeline, the taxpayer may not be able to avail of the concessional 10% tax rate on eligible patent royalty income, and the income may be taxed at the normal applicable rates.

4. Can royalty income from multiple patents be reported in a single Form 65?

Yes. Form 65 under Section 194(1) allows taxpayers to provide details of each eligible patent and the royalty income earned from them in the same filing, subject to the prescribed conditions.

5. Is Form 65 filing beneficial for technology companies and research-driven businesses?

Yes. Form 65 patent royalty income provisions can be particularly beneficial for technology companies, research organizations, and innovators that generate royalty income from patents developed and registered in India, as they may qualify for the concessional 10% tax rate.

6. What information should taxpayers keep ready before starting Form 65 filing?

Before starting Form 65 filing, taxpayers should keep patent details, royalty income information, expenditure records related to the patent, PAN details, and supporting documents readily available to ensure accurate submission.

7. How does Form 65 vs Form 3CFA differ from a taxpayer's perspective?

The objective remains largely the same, which is to claim concessional taxation on eligible patent royalty income. However, Form 65 of the Income Tax Act 2025 is the corresponding form under the Income Tax Act 2025, replacing Form 3CFA that existed under the Income Tax Act 1961.

8. Can Ebizfiling assist with Form 65 filing and document verification?

Yes. Ebizfiling can help taxpayers review eligibility, organize documents required for Form 65 of the Income Tax Act 2025 filing, and guide them through the online filing process to ensure accurate and timely compliance.

9. Why is the 75% expenditure condition important under Section 194(1) of the Income Tax Act 2025?

The patent is considered to be developed in India only when at least 75% of the total expenditure incurred for the invention has been spent in India by the eligible assessee. This condition is essential for claiming the concessional tax benefit.

10. How can Ebizfiling help taxpayers understand Form 65 applicability?

Ebizfiling can assist taxpayers in evaluating Form 65 applicability, understanding patent related eligibility conditions, reviewing supporting documents, and ensuring compliance with the requirements of Section 194(1) of the Income Tax Act 2025 before filing the form.

File Your Income Tax Return with Expert Assistance

File your Income Tax Return on time, claim eligible deductions, and avoid notices with expert guidance.

About Ebizfiling -

June 29, 2026 By Steffy A

Section 37 of the Income Tax Act 2025: Actual Payment Deductions Introduction Section 37 of the Income Tax Act 2025 governs certain business deductions that can be claimed only when the actual payment is made, regardless of the accounting method […]

June 26, 2026 By Steffy A

Updated Return Under Section 263(6) of the Income tax Act 2025 Introduction Section 263(6) of the Income tax Act, 2025 introduces the provisions relating to Updated Returns (ITR-U), allowing taxpayers to voluntarily correct errors, disclose omitted income, or update previously […]

June 29, 2026 By Steffy A

Section 63 of the Income Tax Act 2025: Tax Audit Applicability Overview Section 63 of the Income-Tax Act, 2025 is the new provision governing tax audit requirements in India. It replaces Section 44AB of the Income Tax Act, 1961 and […]