-

July 6, 2026

-

BySteffy A

All About Form 3CFA Filing Under the Income Tax Act 1961

Introduction

Form 3CFA filing is required by eligible taxpayers who wish to claim the concessional tax rate on Patent Royalty Income under Section 115BBF of the Income tax Act 1961. Under the new Income tax Act 2025 and Income tax Rules 2026, Form 3CFA has been renumbered as Form 65, making it important for taxpayers to identify the correct form while exercising this option. This provision allows eligible resident patentees to pay tax at a concessional rate on royalty earned from a Patent Developed in India, subject to prescribed conditions.

In this article, we will discuss Form 3CFA Filing, eligibility criteria, the meaning of patent development in India, Royalty Income Tax provisions, the Concessional Tax Rate on Patent Income, filing timelines, the procedure for filing the form, and the details required to complete Income Tax Form 3CFA.

What is Form 3CFA Filing Under Section 115BBF?

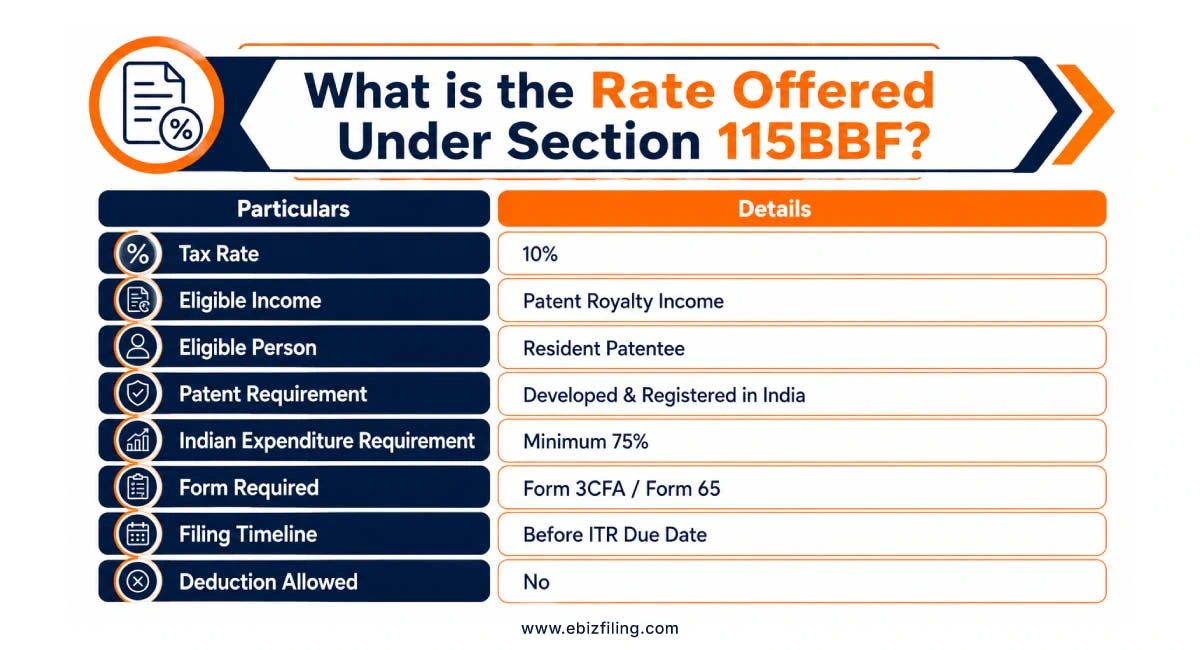

Form 3CFA filing is required to be made with the Income Tax Department as per the procedure prescribed under Section 115BBF to opt for taxation of Patent Royalty Income earned from a patent developed and registered in India by an eligible assessee. An eligible assessee means a person resident in India who is a patentee, that is, the true and first inventor of the invention. For the purpose of claiming the concessional tax benefit, a patent is considered to be developed in India if at least 75% of the expenditure incurred for the invention has been spent in India.

It is important to note that under the Income tax Act 2025 and Income Tax Rules, 2026, Form 3CFA has been renumbered as Form 65.

For more information, refer to our guide on Income Tax Form Renumbering under the Income tax Act 2025.

What is the Rate Offered Under Section 115BBF?

Section 115BBF provides a Concessional Tax Rate on Patent Income of 10% on income earned by way of Patent Royalty Income from a patent developed and registered in India. However, no deduction in respect of any expenditure shall be allowed to the assessee while computing income taxable at the rate of 10%.

Example:

Suppose Mr. A, an eligible resident patentee, earns ₹10 lakh as royalty income from a patent that was developed and registered in India. Subject to fulfillment of the prescribed conditions under Section 115BBF, the royalty income may be taxed at the concessional rate of 10%. However, Mr. A cannot claim deductions for expenses incurred in earning such royalty income while computing the taxable amount.

How to arrive at the total income by way of royalty to offer tax @10%?

Royalty income means any consideration for the:

- Transfer of all or any right in respect of a patent; or

- Imparting any information concerning the working of, or the use of, a patent; or

- Use of a patent; or

Rendering any services concerning the activities referred to above.

Royalty also includes any lump sum consideration (including any advance payment received which is non-refundable) but excludes income in the nature of capital gains or consideration received from the sale of a product manufactured using a patented process or article for commercial use.

Time Limit to Avail the Option of Concessional Tax Rate

Eligible assessee may opt for the concessional rate of taxation by filing Form 3CFA on or before the due date of filing the income tax return. There is no compulsion to pay tax under Section 115BBF, and an assessee may choose to pay tax at the normal income tax rates.

However, if an assessee, after opting for the concessional tax rate, pays tax otherwise than at 10% in any of the next five years, the assessee shall not be eligible to opt for the concessional tax rate for the subsequent five assessment years from the year in which such tax treatment is adopted. In simple words, if an assessee opts for the concessional tax rate, the benefit remains available subject to compliance with the prescribed provisions. If the assessee does not comply with the provisions during any of the next five years, the assessee shall become ineligible to claim the concessional tax benefit for the following five assessment years.

Procedure for Form 3CFA Filing

An eligible assessee can furnish the form by any of the following two ways:

- Electronically through a Digital Signature Certificate (DSC); or

- Electronically through an Electronic Verification Code (EVC), i.e., through an OTP sent to the registered mobile number of the assessee.

The form shall be completed in all respects and must be filed before the due date specified above to avail of the concessional tax rate.

What Details are Required in Form 3CFA?

Very few details are required for Form 3CFA filing to claim the concessional tax rate, such as the basic details of the assessee, including PAN Application, address, and patent-related information, including the patent number, date of grant of patent, and details of the person or persons in whose name the patent is registered. The form may also require details relating to royalty income and expenditure incurred in respect of the eligible patent.

Ebizfiling’s Support for Tax and Regulatory Compliance

Understanding provisions such as Section 115BBF, Patent Royalty Income, and Form 3CFA filing can be challenging for taxpayers. Ebizfiling simplifies complex tax and compliance topics through expert-written guides, practical insights, and regular updates on regulatory changes. Our goal is to help businesses, professionals, and individuals stay informed about income tax requirements and make better compliance decisions.

Explore Related Assistance:

- Income Tax Return Filing

- Business Income Tax Return Filing

- Tax Compliance Advisory

- Annual Compliance Services

Whether you need assistance with Income Tax Return Filing, tax compliance, or understanding various income tax provisions, Ebizfiling’s experts are here to help.

Conclusion

Form 3CFA filing enables eligible resident patentees to claim the concessional 10% tax rate on Patent Royalty Income under Section 115BBF of the Income tax Act 1961. To avail of this benefit, taxpayers must satisfy the eligibility conditions, ensure that the patent qualifies as a Patent Developed in India, and file the prescribed form within the due date. With the renumbering of Form 3CFA as Form 65 under the Income tax Act 2025, taxpayers should also stay updated with the latest compliance requirements to avoid filing errors and continue enjoying the available tax benefits.

Frequently Asked Questions

1. Can the concessional tax rate on Patent Royalty Income be claimed without Form 3CFA filing?

No. Form 3CFA filing is an important requirement for taxpayers who wish to opt for the concessional tax regime under Section 115BBF. Without filing the prescribed form within the specified timeline, the benefit of the concessional tax rate may not be available.

2. Does a patent need to be registered in India for Form 3CFA filing?

Yes. The concessional tax benefit under Section 115BBF is available only in respect of patents that are developed and registered in India. Merely earning royalty income from a patent is not sufficient; the patent must also satisfy the prescribed conditions relating to development and registration in India.

3. Is Patent Royalty Income eligible for a 10% tax rate in India?

Yes. Eligible resident patentees can avail a Concessional Tax Rate on Patent Income of 10% on qualifying Patent Royalty Income. This provision was introduced to encourage innovation and research activities within India. To understand the broader framework of Tax on Income from Patents, taxpayers may refer to our detailed guide on the subject.

4. How is a Patent Developed in India determined?

A patent is generally considered a Patent Developed in India when at least 75% of the expenditure incurred for the invention has been spent within India. This condition helps ensure that the benefit is available only for inventions substantially developed in the country.

5. Can advance royalty payments be treated as Patent Royalty Income?

Yes. Non-refundable advance payments and lump-sum consideration received in connection with patent rights may be treated as Patent Royalty Income. However, the nature of the payment and the underlying arrangement should satisfy the conditions prescribed under Section 115BBF.

6. Are deductions allowed while claiming the concessional tax rate under Section 115BBF?

No. Taxpayers opting for the concessional tax rate of 10% cannot claim deductions for expenditure incurred in earning such royalty income. The income is taxed at the prescribed rate without allowing related expense deductions.

7. What happens if the conditions of Section 115BBF are not followed after opting for the concessional tax regime?

If the prescribed conditions are not complied with after opting for the concessional tax regime, the taxpayer may lose the benefit of the concessional rate for the period specified under the law. Therefore, continued compliance is important even after exercising the option.

8. What information is generally required for Form 3CFA filing?

Form 3CFA filing generally requires details such as PAN, address, patent number, date of grant of patent, patentee information, and royalty income details. Taxpayers may also refer to our guides on Patent Registration in India and Income Tax Return Filing.

9. How can Ebizfiling help taxpayers stay informed about Form 3CFA filing and tax compliance?

Ebizfiling regularly publishes easy-to-understand guides, compliance updates, and practical insights on income tax provisions, regulatory changes, and filing requirements. These resources help taxpayers stay updated on topics such as Form 3CFA filing, royalty taxation, and other compliance obligations.

10. Why should taxpayers stay updated on changes such as the renumbering of Form 3CFA to Form 65?

Tax laws and compliance procedures are updated from time to time. Staying informed about changes, such as the renumbering of Form 3CFA as Form 65 helps taxpayers use the correct forms, avoid filing mistakes, and remain compliant with the latest income tax requirements.

Income Tax Return

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling

About Ebizfiling -

Reviews

Anaya Patel

16 Sep 2018I was so satisfied with the services they provided to me. I had a great time working with them.

Gunjan Kapoor

19 Jan 2018I was amused when I saw the pro activeness in the staff as they made sure everything was on track and in time.

Christopher

07 Aug 2020EbizFiling helped us with our Indian subsidiary company formation from start to finish. The customer service, knowledge, technical know how and communication was amazing. The delivery of services were timely and as per schedule. Thanks team and congratulations on the job well done. I recommend EbizFiling to any local or international company that wants to start operations in Incredible India.

July 25, 2026 By Steffy A

Section 393(2) of the Income Tax Act 2025: Complete TDS Guide Introduction Section 393(2) of the Income Tax Act 2025 provides the rules for deducting tax at source from specified income and sums paid or credited to non-residents, foreign companies […]

July 25, 2026 By Steffy A

Section 394 of the Income Tax Act, 2025: TCS Rules and Exemptions Introduction Section 394 of the Income Tax Act governs the collection of tax at source on specified transactions. Under this provision, sellers and other specified persons collect TCS […]

July 23, 2026 By Steffy A

Section 202 of the Income Tax Act, 2025: Tax Slabs and Rules Introduction Section 202 of the Income Tax Act 2025 contains the provisions governing the new tax regime for individuals, Hindu Undivided Families, Associations of Persons, Bodies of Individuals, […]