-

June 23, 2026

-

BySteffy A

Section 54 Under the Income Tax Act: Capital Gains Exemptions

Overview

Section 54 Under the Income Tax Act provides relief from long-term capital gains tax when gains earned from the sale of a residential house property are reinvested in another eligible residential house. This reinvestment transaction must be made 1 year before or 2 years after the transfer date. For a house under construction, the time limit is 3 years from the transfer date. From AY 2024-25 onwards, the maximum exemption under Section 54 is capped at ₹10 crore. This cap was introduced by the Finance Act, 2023. Under the Income Tax Act, 2025, effective from 1 April 2026, this provision has been reorganized under Section 82 while retaining substantially similar conditions.

This article explains the exemption rules under both Section 54 and Section 82 to help taxpayers understand the updated reference clearly.

What is Section 54 of the Income Tax Act? (Now Section 82)?

Section 54 of the Income Tax Act aims to encourage reinvestment in residential properties by offering tax relief on capital gains. It’s designed for individuals and HUFs selling a residential house, with clear rules on reinvestment timelines and conditions. Under the Income Tax Act, 2025, this provision has been reorganized as Section 82, while its key conditions and benefits continue to remain the same.

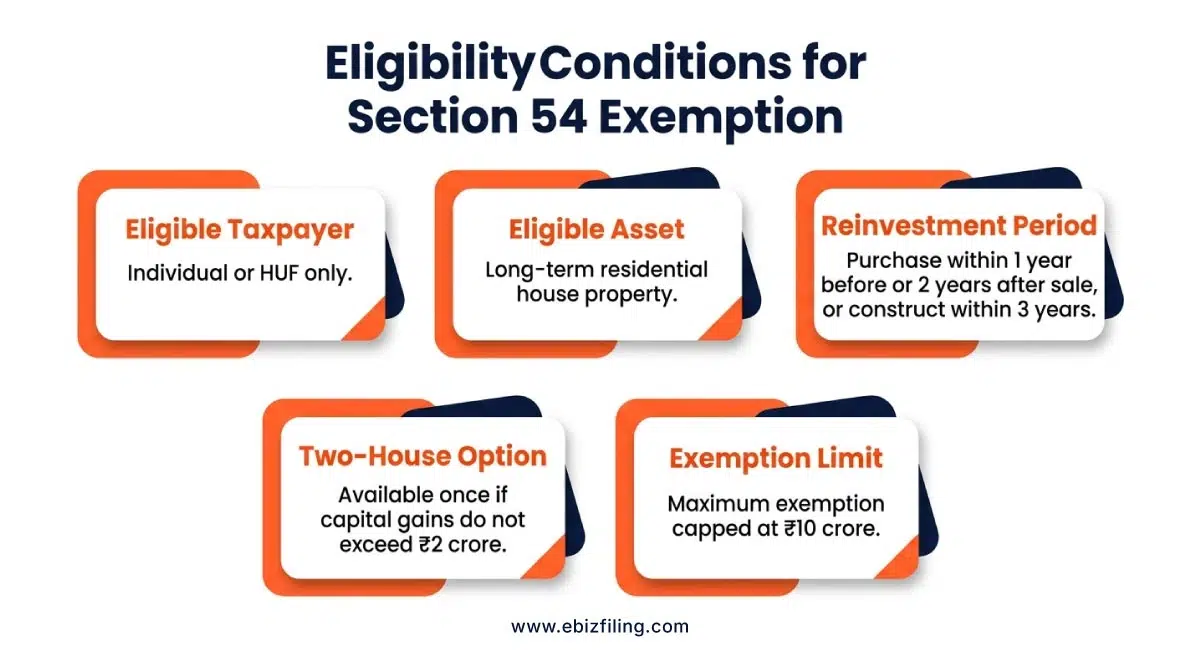

Eligibility Criteria for Section 54 Under the Income-tax Act

|

Particular |

Requirement |

|

Eligible Taxpayer |

Individual or Hindu Undivided Family (HUF) |

|

Original Asset Sold |

Long-term residential house property |

|

Holding Period |

More than 24 months before sale |

|

Purchase of New House |

Within 1 year before or 2 years after the date of transfer |

|

Construction of New House |

Within 3 years from the date of transfer |

|

Capital Gains Requirement |

Long-term capital gains must arise from the sale |

|

Maximum Exemption Limit |

Up to ₹10 crore from AY 2024-25 onwards |

|

Two-House Benefit |

Available once in a lifetime if LTCG does not exceed ₹2 crore |

|

CGAS Deposit |

Unutilized gains may be deposited in the Capital Gains Account Scheme (CGAS) before the due date under Section 139(1) |

Conditions for Claiming Exemption Under Section 54

To obtain the benefit of Section 54 Under the Income Tax Act, the following conditions must be followed:

- You must be an eligible taxpayer belonging to the individual or Hindu Undivided Family (HUF) category.

- The asset you sell should be a residential house property. It should be held as a long-term asset, which means for over 2 years.

- You must earn capital gains. There is no provision for exemption if you do not make profits from selling the residential property.

- You must reinvest in another home, either through purchase or construction. The new property’s transaction should be completed within the time limit allowed under Sec 54.

The Finance Act, 2020 amended Section 54 with effect from Assessment Year 2021-22 to extend the benefit of exemption in respect of investments made in two residential house properties. If the amount of long-term capital gains does not exceed ₹2 crore, an exemption shall be available for investments made through the purchase or construction of two residential house properties. If the assessee exercises this option, it cannot be exercised again for the same or any subsequent assessment year.

With effect from Assessment Year 2024-25, the maximum exemption available under Section 54 is restricted to ₹10 crore. If the cost of the new residential property exceeds ₹10 crore, the excess amount shall be ignored while computing the exemption.

Capital Gains Account Scheme (CGAS) Under Section 54 Under the Income Tax Act

If a taxpayer is unable to utilize the capital gains for purchasing or constructing a new residential property before filing the income tax return, the unutilized amount may be deposited under the Capital Gains Account Scheme (CGAS). The deposit must be made before the due date of filing the return under Section 139(1). The amount deposited must be used within the prescribed time limit for acquiring or constructing a residential house. Any amount not utilized after the specified period may become taxable in the year in which the time limit expires.

How is Exemption Under Section 54 Under the Income Tax Act Calculated?

The exemption available under Section 54 Under the Income Tax Act is either lower of:

- The long-term capital gain arising from the sale of the residential property; or

- The cost of the new residential property purchased or constructed.

Any remaining capital gain will be taxable. For example, if the long-term capital gain is ₹30 lakh and the cost of the new residential property is ₹25 lakh, the exemption available under Section 54 will be limited to ₹25 lakh, and the remaining ₹5 lakh will be taxable.

Example of ₹10 Crore Exemption Limit:

If the long-term capital gain is ₹15 crore and the taxpayer invests ₹15 crore in a new residential property, the exemption under Section 54 will still be restricted to ₹10 crore. The remaining ₹5 crore of capital gain will remain taxable, as the Finance Act, 2023 capped the maximum exemption at ₹10 crore from AY 2024-25 onwards.

Different Types of Capital Assets under the Income Tax Act

Capital assets are divided into two key categories for capital gains:

Short-term capital assets :

For residential house property, land, and buildings, assets held for 24 months or less are treated as short-term capital assets. Short-term capital gains are the profits earned from the sale of such assets.

Long-term capital assets :

For residential house property, land, and buildings, assets held for more than 24 months are treated as long-term capital assets. Long-term capital gains are the profits earned from the sale of such assets.

Consequences if a Taxpayer Transfers a New House Property Within 3 Years

If the new residential house purchased or constructed under Section 54 is transferred within 3 years from the date of its purchase or construction, the exemption claimed earlier is adjusted while calculating capital gains on the sale of the new house.

For this purpose, the cost of acquisition of the new house is reduced by the amount of exemption claimed under Section 54. If the exemption claimed is equal to or more than the cost of the new house, the cost of acquisition may be treated as nil while calculating capital gains.

Comparison Between Section 54 and Section 54F

Although both Section 54 and Section 54F provide exemption from long-term capital gains tax, they apply to different types of capital assets and have different eligibility conditions. The table below highlights the key differences between the two provisions.

|

Section 54 Under the Income Tax Act |

Section 54F Under the Income Tax Act |

|

Applies to long-term capital gains arising from the sale of a residential house property. |

Applies to long-term capital gains arising from the sale of any capital asset other than a residential house property. |

|

Only the capital gains amount needs to be invested to claim full exemption. |

The entire net sale consideration must be invested to claim full exemption. |

|

No restriction applies regarding the number of residential houses owned by the taxpayer. |

The taxpayer should not own more than one residential house (other than the new house) on the date of transfer of the original asset. |

|

If the entire capital gain is not invested, exemption is restricted to the amount invested in the new residential house. |

If only a part of the net sale consideration is invested, exemption is allowed proportionately. |

| If the new residential house is sold within the prescribed period, the exemption claimed under Section 54 may be withdrawn and become taxable. |

If the new house is sold within the prescribed period or the conditions of Section 54F are violated, the exemption claimed earlier becomes taxable. |

|

Exemption is available up to the amount of capital gains invested in the new residential house. |

Exemption is calculated using the formula: Exemption = Cost of New House × Capital Gain ÷ Net Sale Consideration. |

Need Help with Capital Gains and ITR Filing?

- Our experts help calculate long-term capital gains from residential property sales.

- Ebizfiling provides guidance on Income Tax Return Filing for capital gains transactions.

- Our team assists with tax compliance and documentation support.

- Guidance is available for understanding CGAS and exemption-related requirements.

- Taxpayers can connect with Ebizfiling for professional income tax assistance.

Connect with Ebizfiling for Income Tax Return Filing and Capital Gains Tax consultancy support.

Conclusion

Section 54 Under the Income Tax Act, the provisions corresponding to Section 82 under the Income Tax Act, 2025, continue to provide valuable tax relief on long-term capital gains arising from the sale of residential property. Taxpayers can claim exemption by purchasing or constructing another residential property within the prescribed timelines or by depositing the amount under the Capital Gains Account Scheme (CGAS). Proper planning of property transactions, timely reinvestment, and correct utilization of CGAS can help taxpayers maximize exemption under Section 54 and reduce long-term capital gains tax liability.

Suggested Reads:

Frequently Asked Questions

1. How does Section 82 of the Income Tax Act 2025 relate to the old Section 54?

Section 82 under the Income Tax Act, 2025 corresponds to the old Section 54 of the Income Tax Act, 1961. It covers exemption on long-term capital gains from the sale of a residential house property when the gains are reinvested in another eligible residential house.

2. Who is eligible to claim Section 54 capital gains exemption?

Section 54 Under the Income Tax Act capital gains exemption can be claimed by an Individual or a Hindu Undivided Family (HUF) on the transfer of a long-term residential house property, subject to fulfillment of the prescribed conditions.

3. How does the Capital Gains Account Scheme (CGAS) work under Section 54?

The Capital Gains Account Scheme (CGAS) allows taxpayers to deposit unutilized capital gains in a designated account if they are unable to purchase or construct a new residential property before the due date of filing the income tax return under Section 139(1). The deposited amount must be utilized within the prescribed period to retain the exemption under Section 54.

4. What happens if the new residential house is sold within 3 years?

If the new residential house is sold within 3 years from the date of purchase or construction, the earlier exemption under Section 54 may be adjusted while calculating capital gains on the sale of the new house.

5. Can exemption under Section 54 be claimed for two residential houses?

Yes, a taxpayer can claim an exemption for investment in two residential houses, but only once in a lifetime and if capital gains do not exceed ₹2 crore, subject to conditions prescribed under the Act. However, this benefit can be exercised only once in a lifetime.

6. What is the maximum exemption limit under Section 54 from AY 2024-25?

From Assessment Year 2024-25 onwards, the maximum exemption available under Section 54 Under the Income Tax Act is restricted to ₹10 crore. Any investment exceeding this limit will not be considered while calculating the exemption.

7. What is the time limit to reinvest capital gains under Section 54?

To claim exemption under Section 54 Under the Income Tax Act, the taxpayer must purchase a new residential house within one year before or two years after the sale of the original property. Alternatively, a new residential house may be constructed within three years from the date of transfer. Ebizfiling can assist taxpayers with capital gains tax planning, exemption guidance, and ITR filing support.

8. How does Section 54 Under the Income Tax Act help save tax?

Section 54 Under the Income Tax Act helps taxpayers save tax by providing a capital gains exemption on residential houses. If the long-term capital gains arising from the sale of a residential property are reinvested in another eligible residential property within the prescribed period, the taxpayer may claim exemption under Section 54.

9. Can NRIs claim exemption under Section 54 Under the Income Tax Act?

Yes. Non-Resident Indians (NRIs) are eligible to claim exemption under Section 54 Under the Income Tax Act if they satisfy the prescribed conditions and reinvest the capital gains in an eligible residential property located in India. NRIs should also ensure proper reporting of such transactions while filing their income tax returns in India.

10. How can Ebizfiling help with capital gains tax and ITR filing?

Ebizfiling assists taxpayers with capital gains calculations, Section 54 Under the Income Tax Act capital gains exemption planning, Capital Gains Account Scheme (CGAS) guidance, and Income Tax Return Filing. Our experts help ensure compliance with applicable income tax provisions and accurate reporting of capital gains transactions.

Income Tax Return

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling.

About Ebizfiling -

Reviews

Harshit Gamit

19 Apr 2018My GST process was made easier with Ebizfiling. I really appreciate the hard work by your team. Keep up the same in the future. Good Luck!

Pooja Oza

08 Jun 2017If you are also planning to start your own company, there is only one place you need to go to and that is Ebiz. They will take care of all your compliance and legal needs with ease.

saroj behra

19 Apr 2022It has been a Great experience working with Ebizfiling.It is is truly a name you can rely on for a new company registration, gst filing, tax issues etc.The team is truly an expert in its field. Its result oriented approach is truly commendable.Very satisfied with its support team especially Divya G,Sejal G,and Viplab G.They have been very cooperative throught my journey of my new venture.I highly recommend ebizfiling for everyone who wants a better and hasslefree approach to opening and maintaining a new business. Happy ebizfiling..!

June 22, 2026 By Steffy A

Section 82 of the Income Tax Act 2025: Capital Gains Relief Overview Section 82 of the Income Tax Act, 2025, applicable from Assessment Year 2027-28, provides capital gains tax exemption to individuals and Hindu Undivided Families (HUFs) who sell a […]

June 22, 2026 By Steffy A

Income Tax Compliance Calendar July 2026: Key Due Dates Introduction The Income Tax Compliance Calendar July 2026 helps individuals, businesses, employers, and tax deductors stay updated on important statutory due dates related to TDS, TCS, and income tax return filing. […]

June 18, 2026 By Steffy A

Taxability of Minor’s Income Under Income Tax Act, 2025 Introduction Taxability of minor’s income has become a real concern for parents during income tax filing, as children now earn from sports, acting, YouTube, Instagram, gaming, brand deals, gifts, and investments. […]