-

June 29, 2026

-

BySteffy A

Section 43B of the Income Tax Act 1961: Conditions & Exceptions

Introduction

Many businesses record expenses in their books before making the actual payment. Section 43B of the Income Tax Act 1961 was introduced to ensure that certain deductions are allowed only after the payment has been made. The provision commonly applies to taxes, employer contributions to employee welfare funds, interest on specified borrowings, bonuses, leave encashment, and payments to MSMEs. As a result, the timing of payment can directly affect a taxpayer’s eligibility to claim deductions. The purpose of this section is to ensure timely payment of statutory and business obligations before claiming tax benefits.

In this blog, we will explain Section 43B income tax, the expenses covered under it, the conditions for claiming deductions, and its impact on taxpayers.

What is Section 43B of the Income Tax Act 1961?

Section 43B of the Income Tax Act 1961 specifies certain expenses that are allowed as deductions, subject to prescribed conditions. The section follows the principle of the actual payment basis under Section 43B, under which specified deductions are generally allowed only when the payment is actually made. Under the Income-tax Act, 2025, the corresponding provision has been incorporated under Section 37 of the Income Tax Act 2025 while retaining the same principle.

Example:

A business purchases goods from a registered Micro Enterprise in March 2026 and records the expense in its books. If the payment is not made within the time limit prescribed under the MSMED Act, the deduction may not be available in FY 2025-26 and may instead be claimed only in the year in which the payment is actually made.

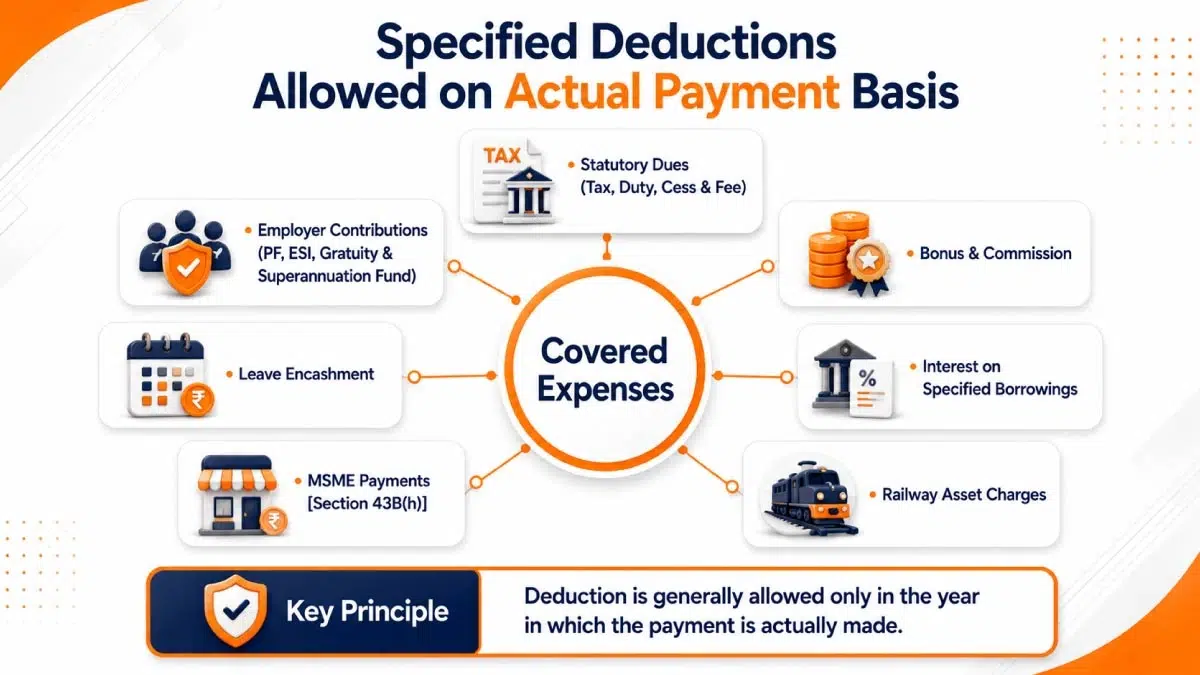

These expenses include:

1. Statutory dues:

This includes payments towards any tax, cess, duty, or fee payable under any law, as well as any contribution made by an employer to a provident fund, superannuation fund, gratuity fund, or any other fund established for the welfare of employees.

2. Employer’s contribution to employee welfare funds:

The contribution made by an employer towards Provident Fund (PF), Employees’ State Insurance (ESI), gratuity fund, superannuation fund, or any other approved employee welfare fund is allowed as a deduction subject to the conditions specified under the Act.

3. Bonus and commission:

Any bonus or commission payable to employees is allowed as a deduction only if it is actually paid within the prescribed time limit.

4. Leave encashment:

Any payment made by an employer in lieu of leave standing to the credit of an employee is allowed as a deduction only on actual payment.

5. Interest on specified borrowings:

Any interest payable on loans or borrowings from public financial institutions, State Financial Corporations, State Industrial Investment Corporations, scheduled banks, co-operative banks, and notified non-banking financial companies is allowed as a deduction only on actual payment.

6. Payments to MSMEs:

Any amount payable to a Micro or Small Enterprise beyond the time limit specified under Section 15 of the MSMED Act, 2006 is allowed as a deduction only in the year in which the payment is actually made. The provisions of Section 43B(h) apply only to Micro and Small Enterprises and do not apply to Medium Enterprises.

7. Railway asset charges:

Any amount payable to the Indian Railways for the use of railway assets is covered under this provision and is deductible only on actual payment.

|

Clause |

Expense Covered |

|

43B(a) |

Tax, Duty, Cess, Fee |

| 43B(b) |

Employer Contribution to PF, ESI, Gratuity, etc. |

|

43B(c) |

Bonus and Commission |

| 43B(d), (da), (e) |

Interest on Specified Borrowings |

|

43B(f) |

Leave Encashment |

| 43B(g) |

Railway Asset Charges |

|

43B(h) |

Payments to MSMEs |

Conditions for Claiming Deductions under Section 43B

To claim a deduction under Section 43B of the Income Tax Act 1961, the following conditions must be satisfied:

1. The sum must be covered under Section 43B:

The deduction must relate to a liability specified under clauses (a) to (h) of Section 43B, including statutory dues, employer contributions to employee welfare funds, bonus or commission, interest on specified borrowings, leave encashment, payments to Indian Railways, and payments to Micro and Small Enterprises (MSMEs).

2. The amount must actually be paid:

Section 43B provides that the deduction is allowed only in the previous year in which the sum is actually paid, irrespective of the year in which the liability was incurred according to the method of accounting followed by the assessee. This reflects the Section 43B payment basis, under which specified expenses are generally allowed as deductions only upon actual payment rather than on an accrual basis.

3. Payment before the due date of filing the return:

As per the proviso to Section 43B, deductions covered under clauses (a) to (g) may be claimed if the payment is made on or before the due date for furnishing the return of income under Section 139(1) and evidence of such payment is furnished along with the return.

4. Special condition for MSME payments:

The benefit of the above provision is not available for payments covered under clause (h). Any amount payable to a Micro or Small Enterprise beyond the time limit specified under Section 15 of the MSMED Act, 2006 is allowed as a deduction only in the year of actual payment. This provision applies only to Micro and Small Enterprises registered under the MSMED Act and does not extend to Medium Enterprises.

5. Conversion of interest into a loan is not considered payment:

Under Explanations 3C, 3CA, and 3D to Section 43B, interest payable on specified borrowings is allowed as a deduction only when it is actually paid. Conversion of such interest into a loan, borrowing, debenture, or any other instrument that merely defers the liability shall not be regarded as actual payment.

Impact of Section 43B on Tax Liability

Section 43B of the Income Tax Act 1961 has a direct impact on the computation of taxable income, as deductions covered under this section are generally allowed only on actual payment. If a specified liability remains unpaid, the deduction may be disallowed in the relevant previous year, resulting in an increase in taxable income and, consequently, the tax liability of the assessee. Since a Section 43B tax deduction is linked to the timing of payment, delayed payments can lead to the deferment of deductions until the year in which the liability is actually discharged.

For example, if an employer fails to deposit contributions to employee welfare funds or does not pay bonus, commission, leave encashment, or interest on specified borrowings within the prescribed time, the deduction may not be available in the year in which the liability was incurred. Instead, the deduction may be claimed in the year in which the payment is actually made.

Similarly, in the case of payments to Micro and Small Enterprises covered under Section 43B(h), any amount paid beyond the time limit specified under Section 15 of the MSMED Act, 2006 is allowed as a deduction only in the year of actual payment. Therefore, timely discharge of liabilities covered under Section 43B is essential to avoid disallowances and additional tax liability.

Exceptions to Section 43B of the Income Tax Act 1961

While Section 43B of the Income Tax Act 1961 generally allows deductions only on actual payment, certain provisions and clarifications govern its application:

Payment up to the due date of filing the return:

As per the proviso to Section 43B, deductions covered under clauses (a) to (g) may be allowed if the amount is actually paid on or before the due date for furnishing the return of income under Section 139(1) and evidence of such payment is furnished.

MSME payments covered under Section 43B(h):

The above relaxation is not available for payments covered under clause (h). Any amount payable to a Micro or Small Enterprise beyond the time limit prescribed under the MSMED Act is deductible only in the year of actual payment.

Employees’ contribution to PF and ESI not covered:

As clarified under Explanation 5 to Section 43B, the provisions of this section do not apply to sums received from employees towards PF, ESI, or similar welfare funds. Such contributions are governed by Section 36(1)(va) of the Income Tax Act and must be deposited within the due dates prescribed under the respective welfare laws to remain eligible for deduction.

Conversion of interest into a loan is not treated as payment:

As per Explanations 3C, 3CA and 3D to Section 43B, interest payable on specified borrowings shall be regarded as paid only when actual payment is made. Conversion of such interest into a loan, debenture, or any other instrument that merely postpones the liability does not qualify as actual payment.

Avoid Section 43B Disallowances with Ebizfiling

Managing deductions under Section 43B of the Income Tax Act 1961 requires careful tracking of payment timelines and outstanding liabilities. Delays in payment can lead to the deferment of deductions and higher taxable income.

Ebizfiling helps businesses by:

- Reviewing liabilities covered under Section 43B before tax filing

- Identifying potential disallowances arising from unpaid expenses

- Assessing the impact of delayed MSME payments under Section 43B(h)

- Verifying compliance with statutory payment requirements

Need expert guidance on Section 43B deductions and tax compliance? Connect with an experienced Chartered Accountant through our Online CA Consultation for ITR Filing service and get practical advice on deduction eligibility, tax implications, and compliance requirements.

Conclusion

Section 43B of the Income Tax Act 1961 governs deductions that are allowed only on an actual payment basis. The provision covers specified expenses such as statutory dues, employer contributions to employee welfare funds, bonus or commission, interest on specified borrowings, leave encashment, payments to Indian Railways, and certain MSME payments. As a result, the timing of payment directly affects the year in which a deduction can be claimed. Under the Income tax Act, 2025, corresponding provisions have been incorporated under Section 37 while substantially retaining the same principles. Taxpayers should therefore ensure timely payment of eligible liabilities to avoid the deferment or disallowance of deductions while computing taxable income.

Frequently Asked Questions

1. Can an expense be disallowed under Section 43B even if it appears in the audited financial statements?

Recognition of an expense in the financial statements does not automatically make it deductible for tax purposes. If the payment conditions prescribed under Section 43B of the Income Tax Act 1961 are not satisfied, the deduction may be disallowed despite being recorded in the books.

2. Why is Section 43B(h) creating challenges for businesses working with MSME vendors?

Many businesses follow credit periods longer than those permitted under the MSMED Act. As a result, even genuine business expenses may not be deductible in the same financial year if payments to eligible MSMEs are delayed.

3. Does obtaining a balance confirmation from an MSME supplier help avoid Section 43B(h) disallowance?

A balance confirmation may support the outstanding amount, but it does not override the payment timelines prescribed under the MSMED Act for claiming deductions under Section 43B(h).

4. Can a company lose a deduction even though the expense is genuine and business-related?

Yes. Section 43B of the Income Tax Act 1961 focuses on the timing of payment rather than the nature of the expense. A genuine expense may still be disallowed if the required payment conditions are not fulfilled.

5. How does Section 43B of the Income Tax Act 1961 affect year-end tax planning?

Businesses often review unpaid statutory dues, employee welfare fund contributions, bank interest, and MSME payables before the financial year closes to identify potential disallowances under Section 43B.

6. Is there a difference between unpaid GST liability and unpaid MSME dues under Section 43B?

Yes. Statutory dues covered under Section 43B(a) may qualify for deduction if paid up to the due date of filing the income tax return. However, this relaxation is not available for MSME payments covered under Section 43B(h).

7. Can converted interest be claimed under Section 43B of the Income Tax Act 1961?

Under Section 43B of the Income Tax Act 1961, unpaid interest that is converted into a loan, borrowing, debenture, or similar instrument is generally not treated as actual payment. Therefore, the deduction is not available merely because the liability has been restructured.

8. What should businesses verify before finalising their tax computation under Section 43B?

Businesses should review unpaid statutory dues, employee welfare fund contributions, bonus liabilities, leave encashment provisions, bank interest, and MSME outstanding balances to identify any amounts that may be disallowed.

9. How can Ebizfiling help businesses identify Section 43B risks before filing their income tax return?

Ebizfiling can assist businesses in reviewing outstanding liabilities, MSME vendor payments, statutory dues, and employee welfare fund contributions to identify potential disallowances before the return is filed.

10. Why do businesses review Section 43B before finalising their income tax return?

Because unpaid statutory dues, employee welfare fund contributions, interest liabilities, and MSME payments can result in the deferment of deductions and increase taxable income if the conditions of Section 43B are not satisfied. Businesses can also seek professional guidance from Ebizfiling to review outstanding liabilities and ensure compliance before filing their income tax return.

File Income Tax Returns

File your ITR with EbizFiling at INR 1199/- only.

About Ebizfiling -

Reviews

Dev Desai

19 Nov 2021Loves their services

Gunjan Kapoor

19 Jan 2018I was amused when I saw the pro activeness in the staff as they made sure everything was on track and in time.

Kriday Thakkar

04 Mar 2018The service I received was great, quick and hassle-free. Looking forward to work with you in future.

July 13, 2026 By Steffy A

Form 79 under the Income Tax Act 2025: Investment Fund Filing Guide Overview Form 79 under the Income Tax Act is a statement used by investment funds to report income paid or credited to unit holders. It is furnished under […]

July 10, 2026 By Steffy A

Form 130 under the Income Tax Act for Salary TDS Certificate Introduction Form 130 under the Income Tax Act is the new TDS certificate for salary, pension, and specified senior citizen interest income. It replaces Form 16 from Tax Year […]

July 7, 2026 By Steffy A

Form 165 under the Income Tax Act: Applicability and Filing Guide Overview Form 165 under the Income Tax Act is a statement used for reporting Specified Financial Transactions (SFTs) to the Income Tax Department. It has been introduced under the […]