-

July 30, 2026

-

BySteffy A

Section 35AD of the Income Tax Act: Specified Business Deduction

Introduction

Certain businesses require substantial investment in infrastructure, machinery, and other capital assets. To encourage investment in such sectors, Section 35AD of the Income Tax Act, 1961 provided an investment-linked deduction for eligible capital expenditure incurred for specified businesses.

The deduction was available only to businesses specifically covered by the provision and subject to prescribed conditions. It did not apply to every business or every type of capital expenditure.

From 1 April 2026, the Income tax Act, 2025, came into force. Section 46 now governs the deduction for capital expenditure incurred for specified businesses, while Section 35AD remains relevant for earlier periods, past claims, and proceedings governed by the Income tax Act, 1961.

What is Section 35AD of the Income Tax Act?

Section 35AD allowed an eligible assessee to claim a deduction for the whole of the qualifying capital expenditure incurred wholly and exclusively for carrying on a specified business.

In simple terms, an eligible business could claim a deduction for qualifying capital investment instead of claiming normal depreciation over several years.

However, the deduction was subject to conditions relating to:

- The nature of the business;

- The date on which operations commenced;

- The manner of payment;

- The use of machinery and plant;

- The use of the eligible asset; and

- Restrictions on claiming other deductions.

The current Section 46 also allows the deduction at the option of the assessee. Therefore, claiming the deduction is not mandatory.

Section 35AD and Section 46 under the Current Law

For periods governed by the Income Tax Act, 1961, the relevant provision was Section 35AD.

For tax years beginning on or after 1 April 2026, the corresponding provision is Section 46 of the Income tax Act, 2025.

Accordingly, an updated article should explain both provisions:

- Section 35AD: Provision under the Income Tax Act, 1961.

- Section 46: Corresponding provision under the Income tax Act, 2025.

Section 35AD may continue to remain relevant while referring to deductions claimed for earlier assessment years, past transactions, tax proceedings or assets for which the deduction was previously allowed.

List of Specified Businesses

The deduction is not available to every business. It applies only to businesses included within the definition of a specified business.

The specified businesses include:

- Setting up and operating a cold-chain facility.

- Setting up and operating a warehousing facility for storing agricultural produce.

- Laying and operating a cross-country natural gas, crude oil or petroleum oil pipeline network for distribution, including integral storage facilities.

- Building and operating a hotel classified as two-star or above by the Central Government.

- Building and operating a hospital with at least 100 beds for patients.

- Developing and building a housing project under a notified slum redevelopment or rehabilitation scheme.

- Developing and building a housing project under a notified affordable housing scheme.

- Producing fertiliser in India.

- Setting up and operating an inland container depot or container freight station approved or notified under customs law.

- Carrying on bee-keeping and producing honey and beeswax.

- Setting up and operating a warehousing facility for storing sugar.

- Laying and operating a slurry pipeline for transporting iron ore.

- Setting up and operating a notified semiconductor wafer fabrication manufacturing unit.

- Developing, or maintaining, and operating, or developing, maintaining, and operating a new infrastructure facility.

An infrastructure facility may include eligible roads, bridges, rail systems, highway projects, water supply projects, irrigation systems, sanitation systems, ports, airports and inland waterways.

Eligibility Criteria for the Deduction

A specified business must satisfy the general and business-specific conditions prescribed under the law.

General Conditions

The specified business should:

- Not be established by splitting up an existing business;

- Not be formed through the reconstruction of an existing business; and

- Generally not be established by transferring previously used machinery or plant to the specified business.

However, previously used machinery or plant may be permitted when its value does not exceed 20% of the total value of machinery or plant used in the specified business.

Machinery previously used outside India may also qualify when:

- It was not previously used in India;

- Tt is imported into India; and

- Depreciation was not previously allowed in India for that machinery.

Conditions for Pipeline Businesses

A cross-country natural gas, crude oil or petroleum oil pipeline business must satisfy additional conditions.

The business must generally:

- Be owned by an eligible Indian company, consortium, or statutory authority;

- Obtain approval from the Petroleum and Natural Gas Regulatory Board and be notified by the Central Government;

- Make the prescribed portion of its pipeline capacity available on a common-carrier basis; and

- Satisfy other prescribed conditions.

The common-carrier capacity should be made available to persons other than the assessee or its associated persons.

Conditions for Infrastructure Facilities

An eligible infrastructure facility must generally be owned by an eligible Indian company, consortium, authority, board, corporation or other permitted statutory body.

The entity must also enter into an agreement with:

- The Central Government;

- A State Government;

- A local authority; or

- Another statutory body.

The agreement must relate to developing, operating, or maintaining a new infrastructure facility.

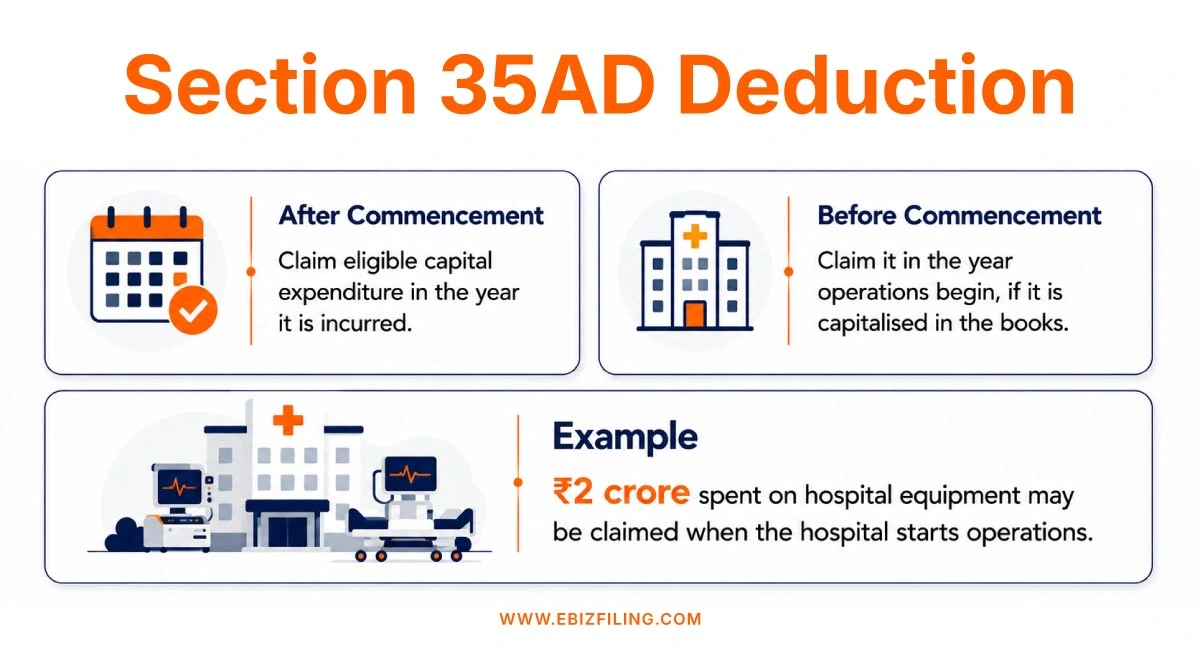

Deduction for Specified Business under Section 35AD

The timing of the deduction depends on when the capital expenditure is incurred.

Expenditure Incurred After Commencement

Capital expenditure incurred after the specified business begins operations is deductible in the tax year in which it is incurred, provided all conditions are satisfied.

Expenditure Incurred Before Commencement

Capital expenditure incurred before the business begins operations can be claimed in the year of commencement when:

- The expenditure relates wholly and exclusively to the specified business; and

- It is capitalized in the books of account on the date operations commence.

Capital expenditure incurred before commencement must be capitalised correctly in the books, making proper business accounting and bookkeeping important for claiming the deduction.

Example

Suppose an eligible hospital incurs ₹2 crore on medical equipment before starting operations. The expenditure is capitalised in its books on the commencement date.

Subject to the applicable conditions, the eligible amount can be claimed in the tax year in which the hospital starts operating.

Expenditure Not Eligible for Deduction

The deduction does not cover every capital expense.

The following expenditure is excluded:

Land

Any expenditure incurred on purchasing land is not eligible.

Goodwill

The cost of acquiring goodwill cannot be claimed.

Financial Instruments

Expenditure incurred on acquiring shares, securities, or other financial instruments is excluded.

Non-Permitted Payments

Where a payment or aggregate of payments exceeding ₹10,000 is made to one person in a day through a mode other than the specified banking or online mode, the expenditure is not treated as eligible capital expenditure.

Therefore, businesses should make qualifying capital payments through properly permitted banking or electronic modes and maintain supporting records.

Ensure Accurate Business Income Tax Filing

Claiming a deduction under Section 35AD requires proper identification of eligible capital expenditures, accurate tax computation and complete supporting records.

Incorrect classification or reporting may affect the deduction claimed in the business income tax return.

Ebizfiling can assist businesses with:

- Reviewing eligible capital expenditure

- Computing taxable business income

- Reporting deductions correctly

- Preparing supporting financial records

Get professional assistance with tax computation, deduction reporting and company ITR filing.

Conclusion

Section 35AD of the Income Tax Act encouraged investment in selected industries by allowing a deduction for eligible capital expenditure incurred for specified businesses. However, the deduction was subject to strict conditions relating to the nature of the business, eligible expenditure, payment method, machinery use and continued use of the asset. From 1 April 2026, businesses should refer to Section 46 of the Income tax Act, 2025 for the corresponding provision. Before claiming the deduction, the assessee should verify the applicable commencement conditions, approvals, expenditure records and restrictions on other deductions.

Frequently Asked Questions

1. Does Section 35AD of the Income Tax Act still apply after 1 April 2026?

Section 35AD applied under the Income Tax Act, 1961. From 1 April 2026, the corresponding provision is Section 46 of the Income tax Act, 2025. Section 35AD may still remain relevant for earlier tax periods, past claims, and related proceedings.

2. Does the deduction under Section 35AD cover every capital expense?

No. The deduction under Section 35AD covered only qualifying capital expenditure incurred wholly and exclusively for an eligible specified business. Expenditure on land, goodwill, and financial instruments is not eligible.

3. Can depreciation be claimed after claiming the deduction under Section 35AD?

No. A business cannot claim depreciation or another deduction for the same asset cost when the full expenditure has already been allowed under Section 35AD or the corresponding current provision.

4. Can expenditure incurred before starting the specified business be claimed?

Yes. Pre-commencement capital expenditures may be claimed in the year the specified business begins operations. However, the expenditure must be capitalised in the books of account on the commencement date.

5. What happens if capital expenditure exceeding ₹10,000 is paid in cash?

Where a payment or aggregate of payments exceeding ₹10,000 is made to one person in a day through a non-permitted mode, the expenditure is not eligible for the deduction under Section 35AD.

6. Can previously used machinery qualify for the deduction?

Previously used machinery is generally restricted. However, it may qualify when its value does not exceed 20% of the total value of machinery or plant used in the specified business, subject to prescribed conditions.

7. Can a loss from a specified business be adjusted against normal business income?

No. A loss from a specified business can generally be adjusted only against profits from another specified business. Any unadjusted loss may be carried forward for adjustment against eligible profits in later years.

8. What happens if an eligible asset is used for another purpose during the eight-year period?

The asset must generally be used only for the specified business for eight years. If it is used for another purpose during this period, the earlier deduction, reduced by notional depreciation, may become taxable as business income.

9. What records are required to claim a Section 35AD deduction?

Businesses should maintain invoices, payment records, asset registers, commencement documents, government approvals and evidence showing the use of each asset. Ebizfiling can assist with accounting records, tax computation and company income tax return filing.

10. How can Ebizfiling help with a specified business deduction?

Ebizfiling can help businesses review eligible capital expenditure, compute taxable income and report the deduction correctly in the company income tax return. Proper reporting helps reduce classification and compliance errors.

ITR filing

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling

About Ebizfiling -

Reviews

Harshit Gamit

19 Apr 2018My GST process was made easier with Ebizfiling. I really appreciate the hard work by your team. Keep up the same in the future. Good Luck!

Misha Kapoor

04 Oct 2017I am a satisfied customer of Ebizfiling. I would surely recommend it to others.

Pooja Oza

08 Jun 2017If you are also planning to start your own company, there is only one place you need to go to and that is Ebiz. They will take care of all your compliance and legal needs with ease.

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]