-

July 27, 2026

-

BySteffy A

Section 206AA of the Income Tax Act: PAN and Higher TDS Rules

Introduction

Section 206AA of the Income Tax Act, 1961 dealt with the requirement to furnish a Permanent Account Number, or PAN, where tax was deductible at source. It applied to residents as well as non-residents who received an amount on which TDS was deductible.

Where the recipient failed to provide a valid PAN, the person responsible for making the payment was generally required to deduct tax at a higher rate. However, certain relaxations were available to eligible non-residents for specified payments.

The Income tax Act, 2025, came into force on 1 April 2026. The corresponding PAN and higher TDS requirements are now covered under Section 397(2) of the Income tax Act, 2025. Section 206AA remains relevant for tax periods and proceedings governed by the Income Tax Act, 1961.

What Is Section 206AA of the Income Tax Act, 1961?

Section 206AA of the Income Tax Act, 1961 required every person entitled to receive an amount on which TDS was deductible to furnish their PAN to the person responsible for deducting the tax.

The person receiving the income is known as the deductee, while the person responsible for deducting TDS is known as the deductor.

If the deductee failed to furnish a valid PAN, the deductor was required to deduct tax at the higher rate prescribed under Section 206AA of the Income Tax Act. An invalid PAN or a PAN that did not belong to the deductee was treated in the same manner as non-furnishing of PAN.

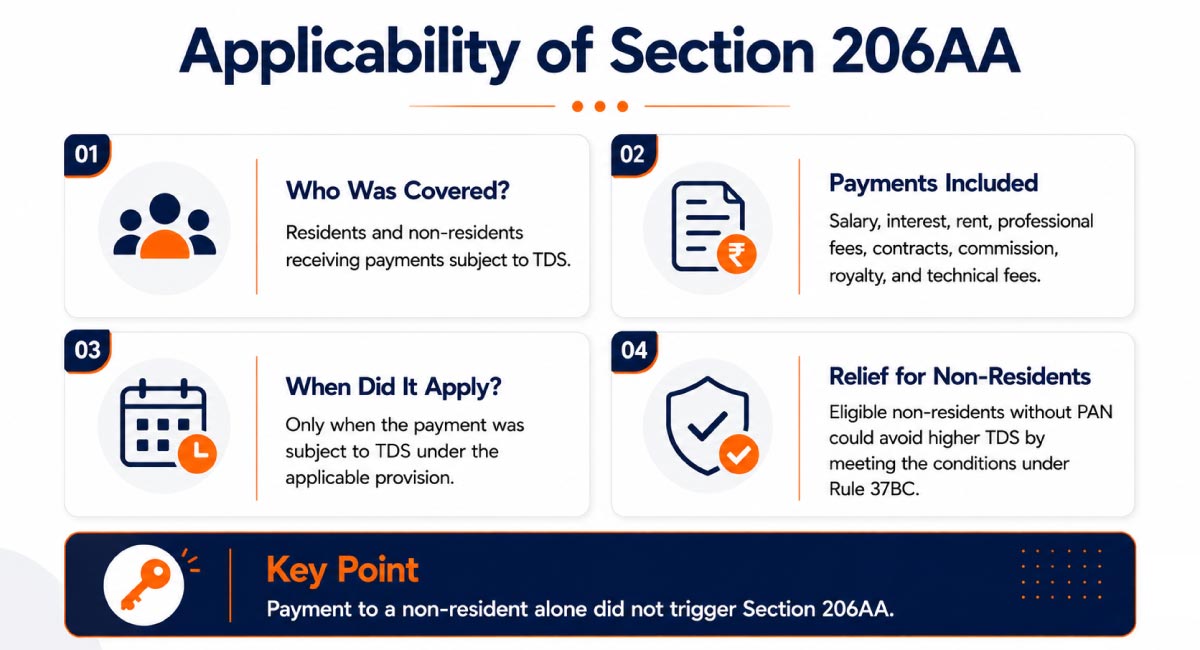

Applicability of Section 206AA of the Income Tax Act

Section 206AA of the Income Tax Act, 1961 applied to any person receiving an amount on which tax was deductible under the TDS provisions of the Income Tax Act, 1961. Therefore, it applied to both residents and non-residents.

It could apply to different categories of payments, including:

- Salary;

- Interest;

- Rent;

- Professional fees;

- Contractual payments;

- Commission or brokerage;

- Royalty;

- Fees for technical services; and

- Other payments subject to TDS.

However, Section 206AA did not automatically apply merely because a payment was made to a non-resident. The payment must first have been subject to TDS under the applicable provision.

Further, it is incorrect to state that Section 206AA did not apply to non-residents who did not have PAN. A non-resident without PAN could avoid the higher TDS rate only when the payment and documentation satisfied the specific conditions prescribed under the Act and Rule 37BC.

Rate of TDS Under Section 206AA of the Income Tax Act

If a person failed to furnish a valid PAN, TDS was required to be deducted at the highest of the following rates:

- The rate specified under the relevant TDS provision of the Income Tax Act;

- The rate or rates in force; or

- The rate of 20%.

For transactions covered under Sections 194O and 194Q, the applicable rate for the third condition was 5% instead of 20%.

Example

Suppose a payment was normally subject to TDS at 10%, but the recipient did not furnish a valid PAN. Assuming the rate in force was not higher than 20%, the applicable TDS rate under Section 206AA would be 20%.

In the case of a non-resident, the applicable rate should also be examined under the relevant tax treaty. Judicial decisions have recognised that a beneficial treaty rate may prevail over the higher rate prescribed under Section 206AA, subject to sat

Under the current Income tax Act, 2025, Section 397(2) similarly provides for deduction at the higher of the prescribed rate, the rate in force, or 20% in most cases. A 5% rate applies to specified transactions covered by the provision.

Important Provisions of Section 206AA

1. PAN Required for a Lower or Nil TDS Certificate

Section 197 of the Income Tax Act, 1961 allowed an eligible taxpayer to apply for a certificate authorising deduction of tax at a lower or nil rate.

However, the Assessing Officer could not issue a certificate under Section 197 unless the application contained the applicant’s PAN.

2. PAN Required in Form 15G or Form 15H

Under the Income Tax Act, 1961, eligible taxpayers could submit a declaration under Section 197A requesting that tax not be deducted from certain specified incomes.

These declarations were submitted through:

- Form 15G by eligible individuals below 60 years of age and certain other eligible persons; and

- Form 15H by eligible resident individuals who were 60 years of age or older.

A declaration under Section 197A was invalid if the declarant failed to furnish a valid PAN. In such a case, the deductor was required to deduct tax at the rate prescribed under Section 206AA.

From 1 April 2026, Forms 15G and 15H have been consolidated into Form 121 under the Income tax Rules, 2026.

3. Invalid or Incorrect PAN

If the PAN furnished by the deductee was invalid or did not belong to the deductee, it was treated as if no PAN had been furnished.

The deductor was then required to deduct TDS at the higher rate applicable under Section 206AA.

4. PAN in Bills and Correspondence

The deductee was required to provide PAN to the deductor. Both parties were also required to mention the deductee’s PAN in relevant correspondence, bills, vouchers, and other documents exchanged between them.

Relaxation for Certain Non-Residents

Section 206AA of the Income tax Act, 1961 provided certain relaxations to eligible non-residents. These relaxations did not exempt the payment from TDS. They only provided relief from the higher TDS rate that would otherwise apply because a valid PAN had not been furnished.

Businesses making cross-border payments should understand the rules governing TDS on Non-Residents before determining the applicable deduction rate.

Interest on Specified Long-Term Bonds

The higher TDS provisions under Section 206AA did not apply to interest paid or payable on specified long-term bonds where tax was deductible under Section 194LC.

Payments Covered Under Rule 37BC

Under Rule 37BC of the Income tax Rules, 1962, a non-resident, other than a company, or a foreign company could claim relief from the higher TDS rate for the following specified payments:

- Interest;

- Royalty;

- Fees for technical services;

- Dividend; and

- Consideration for the transfer of a capital asset.

The relaxation was available only when the non-resident furnished the prescribed information and documents to the deductor. These included:

- Name, email address, and contact number;

- Address in the country or territory of residence;

- A tax residency certificate, where the law of the relevant country or territory provided for its issuance; and

- A foreign Tax Identification Number (TIN) or another government-issued identification number.

Therefore, the absence of PAN did not automatically provide relief from the higher TDS rate. The nature of the payment and the prescribed documentation requirements had to be satisfied.

Relief Under Rule 114AAB

Section 206AA also did not apply to eligible non-residents and foreign companies who were not required to obtain PAN under Rule 114AAB. The relief applied to specified transactions involving eligible foreign investors, specified funds or recognised stock exchanges located in an International Financial Services Centre, subject to the prescribed conditions.

Position Under the Income tax Act, 2025

From 1 April 2026, a similar relaxation is available under Section 397(2)(c) of the Income tax Act, 2025, read with Rule 217 of the Income tax Rules, 2026.

Rule 217 covers specified payments such as interest, royalty, fees for technical services, dividends, and consideration for the transfer of a capital asset. It also provides relief where an eligible non-resident or foreign company is not required to apply for PAN under Section 262 and the applicable rules.

Expert Support for TDS Filing and Corrections

Accurate PAN details, correct TDS rates, and proper reporting are important for error-free TDS compliance. Ebizfiling assists businesses, employers, and deductors with preparing, filing, and correcting TDS statements, commonly referred to as TDS returns.

Our team can help with:

- Checking PAN and deduction details;

- Identifying the applicable TDS section and rate;

- Preparing and filing TDS statements;

- Correcting PAN, challan, or deduction-related errors; and

- Assisting with TDS certificates and compliance records.

Need help with accurate TDS filing or correction of an existing statement? Get professional assistance from Ebizfiling for TDS Return Filing.

Conclusion

Section 206AA of the Income Tax Act required a deductee to furnish a valid PAN where TDS was applicable. Failure to provide a valid PAN generally resulted in tax deduction at a higher rate. However, eligible non-residents could claim relief for specified payments by meeting the conditions under Rule 37BC. From 1 April 2026, the corresponding PAN and higher TDS rules are covered under Section 397(2) of the Income tax Act, 2025.

Suggested Reads:

Section 397 of the Income Tax Act

Frequently Asked Questions

1. What happens when a deductee does not furnish a valid PAN?

For transactions governed by the Income tax Act, 1961, Section 206AA generally required TDS to be deducted at the highest of the rate specified under the relevant provision, the rate or rates in force, or 20%. From 1 April 2026, the corresponding requirements are covered under Section 397(2) of the Income tax Act, 2025.

2. Is TDS always deducted at 20% when PAN is not furnished?

No. Under Section 206AA, TDS was deducted at the highest of the rate specified under the relevant provision, the rate or rates in force, or 20%. For transactions covered under Sections 194O and 194Q, the specified higher rate was 5% instead of 20%. Section 397(2) of the Income tax Act, 2025 also prescribes 5% for specified transactions and 20% in other cases.

3. What happens if the PAN furnished by the deductee is invalid or belongs to another person?

An invalid or mismatched PAN is treated as non-furnishing of PAN. The deductor may have to apply the higher TDS rate, correct the PAN through a TDS correction statement, and deposit any resulting shortfall and applicable interest.

4. What happens if a vendor furnishes PAN after issuing the invoice?

The invoice date alone does not determine the applicable TDS rate. For most vendor payments, tax becomes deductible on the earlier of credit or payment. If a valid PAN is furnished before TDS becomes deductible, the normal rate may apply. Furnishing PAN later does not automatically remove an earlier short-deduction default.

5. Can a foreign company receive payment without obtaining an Indian PAN?

Yes, in specified cases. Under the earlier framework, a foreign company could avoid the higher rate under Section 206AA without obtaining an Indian PAN for payments covered by Rule 37BC, provided the prescribed information and documents were furnished.

6. Does Rule 37BC or Rule 217 completely remove TDS?

No. These rules provide relief only from the higher rate that applies because PAN was not furnished. Normal TDS may still apply if the payment is chargeable to tax in India under domestic law or an applicable tax treaty.

7. Can the PAN relaxation apply when property is purchased from a non-resident?

Consideration paid for the transfer of a capital asset is included among the specified payments covered by Rule 37BC, subject to the prescribed conditions and documents. However, the relaxation does not remove the buyer’s obligation to deduct tax where TDS is otherwise applicable. Under the 2025 framework, the corresponding relaxation is covered by Rule 217.

8. Can Form 15G or Form 15H be accepted without a valid PAN?

No. Under the Income tax Act, 1961, a declaration in Form 15G or Form 15H without a valid PAN was treated as invalid. For a tax year beginning on or after 1 April 2026, these declarations are furnished through Form 121 under Section 393(6). A declaration without a valid PAN is also invalid under Section 397(2).

9. Can a lower or nil TDS certificate be issued without PAN?

No. Under the earlier law, an application under Section 197 had to contain the applicant’s PAN. From 1 April 2026, applications for a lower or nil deduction are governed by Section 395 and are filed in Form 128. Section 397(2) provides that a certificate cannot be granted if a valid PAN is not furnished in the application.

10. How can Ebizfiling help prevent PAN-related TDS errors?

Ebizfiling can assist deductors with verifying PAN details, identifying the applicable TDS provision and rate, preparing TDS statements, and correcting PAN, challan, or deduction-related errors. Proper review before filing can reduce PAN mismatches, short deductions, and incorrect tax-credit reporting.

File TDS Returns

Quickly file error-free TDS Returns with EbizFiling. Prices Starting INR 999/-.

About Ebizfiling -

Reviews

Ashish Paliwal

29 Sep 2018Let me be honest and tell you that I did not choose eBiz filing after my initial LLP company registration did to pricing. A lot of companies contact me with better rates so I generally choose them. However, I will still rate eBiz filing 10/10 on work ethics. You guys are professionals in true sense.

Hetal Verma

27 Jan 2018Great work done by the Ebizfiling team. Good luck for the future.

Lakshman Rajpurohit

28 May 2017We are looking for company who provides registration and process for SSI certificate. We contact ebizfiling and they have done job for us in a smooth way. we really appreciate their service and quick turn around time. Special Thanks to team of ebizfiling India pvt. ltd.

July 30, 2026 By Steffy A

Section 133 of the Income Tax Act, 2025: Donation Deduction Introduction Section 133 of the Income Tax Act, 2025 allows taxpayers to claim a deduction for monetary donations made to specified funds, charitable institutions, government bodies and approved organizations. The […]

July 29, 2026 By Steffy A

Section 46 of the Income Tax Act, 2025: Specified Business Deduction Introduction Certain businesses require major investment in buildings, machinery, infrastructure, and operational facilities. Hospitals, hotels, warehouses, pipelines, and infrastructure projects are common examples. Section 46 of the Income Tax […]

July 25, 2026 By Steffy A

Section 393(2) of the Income Tax Act 2025: Complete TDS Guide Introduction Section 393(2) of the Income Tax Act 2025 provides the rules for deducting tax at source from specified income and sums paid or credited to non-residents, foreign companies […]