-

July 22, 2026

-

BySteffy A

Section 196D of the Income Tax Act, 1961: TDS Rules for FIIs

Introduction

Section 196D of the Income Tax Act governed the deduction of tax at source on certain securities income paid to Foreign Institutional Investors in India. It was introduced through the Finance Act, 1993, and became effective from 1 June 1993. The provision helped collect tax at the time covered securities income was credited or paid to a foreign investor.

In this blog, we explain the applicability of Section 196D, the applicable TDS rate, the treatment of capital gains, DTAA benefits and the corresponding provisions under the Income tax Act, 2025.

What Is Section 196D of the Income Tax Act?

Section 196D of the Income Tax Act applied when securities income referred to in Section 115AD was payable to a Foreign Institutional Investor. The provision generally covered dividend and other securities income, except interest specifically covered under Section 194LD. Capital gains from the transfer of covered securities were separately excluded from TDS under Section 196D(2).

Who Is a Foreign Institutional Investor?

Under Section 115AD, a Foreign Institutional Investor meant an investor specified by the Central Government through a notification in the Official Gazette.

In the present SEBI regulatory framework, the term Foreign Portfolio Investor, or FPI, is generally used. FPIs are regulated under the SEBI Foreign Portfolio Investors Regulations. However, the older Income tax Act provisions continued to use the term Foreign Institutional Investor.

For ease of understanding, this article uses the terms “FII” and “FPI” where relevant. However, “Foreign Institutional Investor” was the term specifically used under Section 196D of the Income tax Act, 1961.

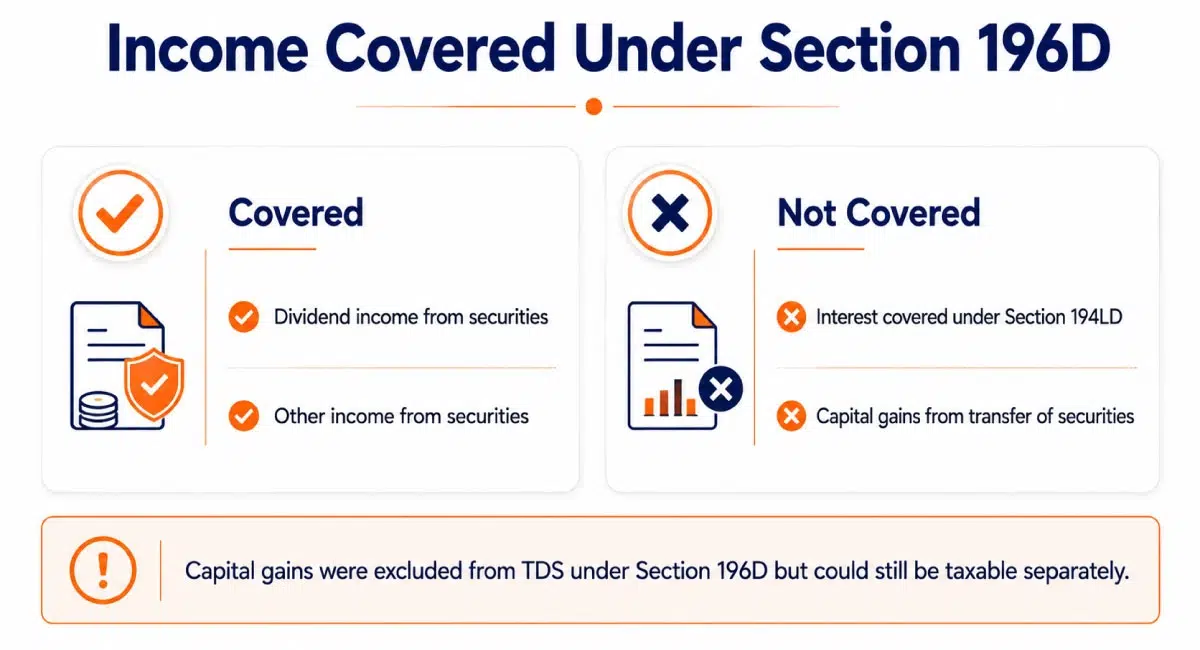

Income Covered Under Section 196D

Section 196D covered income received by a Foreign Institutional Investor in respect of securities referred to under Section 115AD.

The covered income generally included:

- Dividend income from securities, other than units referred to under Section 115AB; and

- Other income in respect of securities, except interest specifically covered under Section 194LD.

However, Section 196D did not apply to:

- Interest income is specifically covered under Section 194LD; and

- Capital gains arising from the transfer of securities referred to under Section 115AD.

Capital gains were specifically excluded from TDS under Section 196D(2), although they could still be taxable in the hands of the FII or FPI under the applicable capital gains provisions.

TDS Rate Under Section 196D of the Income Tax Act

The basic TDS rate under Section 196D of the Income Tax Act was 20% on covered securities income paid to an FII. The Income Tax Department also recognises that a lower rate available under an applicable Double Taxation Avoidance Agreement may be used where the required treaty conditions are fulfilled.

The applicable rate may also be affected by provisions relating to surcharge, health and education cess, PAN, treaty documentation and the legal status of the recipient.

When Is TDS Deducted?

TDS was required to be deducted at the earlier of the following:

- When the income is credited to the account of the recipient; or

- When the payment is made through cash, cheque, bank transfer, or another mode.

The same credit-or-payment principle also applied to specified funds under Section 196D(1A).

Is TDS Deducted on Capital Gains Under Section 196D?

No TDS was required under Section 196D on income arising by way of capital gains from the transfer of securities covered under Section 115AD.

However, this does not mean that the capital gains are automatically exempt from income tax. The FII or FPI may still be required to calculate and pay tax on the capital gains at the applicable rate under Section 115AD and other relevant provisions. Section 115AD separately prescribed rates for short-term and long-term capital gains.

Payment of Securities Transaction Tax did not independently determine whether TDS was required under Section 196D. Capital gains were outside the TDS requirement because Section 196D(2) specifically excluded capital gains arising from the transfer of covered securities.

DTAA Benefit Under Section 196D of the Income Tax Act

A Foreign Institutional Investor residing in a country that has a DTAA with India may be entitled to a lower TDS rate where the treaty rate is more beneficial.

To apply the lower treaty rate, the investor must satisfy the applicable conditions and provide the required documents, including a valid Tax Residency Certificate.

Under the corresponding provision of the Income tax Act, 2025, the treaty rate applies where it is lower than 20% and the prescribed residency certificate has been furnished.

Therefore, a DTAA does not provide an automatic exemption. The relevant treaty article, beneficial ownership conditions, and supporting documents must be examined.

TDS on Income of a Specified Fund

Section 196D(1A) provided a separate 10% TDS rate where covered securities income was payable to a specified fund.

No TDS was required where the income was exempt under Section 10(4D) of the Income tax Act, 1961. This rule applied at the earlier of credit or payment.

Therefore, the 10% rate applicable to a specified fund was separate from the 20% rate generally applicable to an FII.

Is TDS Under Section 196D the Final Tax?

TDS deducted under Section 196D was not necessarily the final tax liability of the FII or FPI.

The final tax liability depends on:

- The nature and amount of income;

- The rates prescribed under Section 115AD;

- Capital gains earned during the year;

- DTAA benefits;

- Exempt income;

- Tax already deducted; and

- Other applicable provisions.

The tax deducted can generally be claimed as credit while determining the final tax payable.

Is an FII Required to File an Income Tax Return?

Deduction of TDS under Section 196D did not automatically remove the income tax return filing requirement of an FII or FPI. Return filing depended on Section 139, the investor’s legal status, the nature and amount of taxable income, and other applicable provisions. A foreign company may generally be required to use the income tax return prescribed for companies.

Therefore, return-filing eligibility must be examined separately in each case.

Section 196D Under the Income tax Act, 2025

The Income tax Act, 2025, came into force on 1 April 2026. For the tax year 2026-27 and subsequent tax years, the corresponding TDS provision is contained in Section 393(2), Table Serial Number 15.

It provides a 20% TDS rate on covered securities income paid to a Foreign Institutional Investor. A lower DTAA rate may apply where the treaty is applicable and the required residency certificate is furnished.

The corresponding tax-rate provision for securities income and capital gains of Foreign Institutional Investors is Section 210 of the Income tax Act, 2025. Section 210 prescribes separate rates for securities income, short-term capital gains, and long-term capital gains.

Capital gains payable to an FII are specifically listed as a case where TDS is not required under the corresponding no-deduction table.

TDS Return Filing Assistance from Ebizfiling

Ebizfiling provides professional assistance with TDS return filing for businesses, deductors, and foreign payment transactions. Our team can help with:

- Identifying the correct TDS provision and applicable rate;

- Preparing and filing the relevant TDS return;

- Reviewing PAN, payment, and deduction details;

- Checking DTAA-related documents for payments to non-residents;

- Assisting with TDS certificates and compliance documentation.

Conclusion

Section 196D of the Income Tax Act provided for TDS at 20% on specified securities income paid to Foreign Institutional Investors. A lower DTAA rate could apply where the investor satisfied the treaty requirements and furnished the prescribed documents.

The provision did not require TDS on capital gains from the transfer of covered securities. However, such capital gains could still be taxable under Section 115AD. TDS should also not be treated as final tax, and income tax return requirements must be examined separately.

For tax years beginning on or after 1 April 2026, the corresponding provisions must be read under Sections 393 and 210 of the Income tax Act, 2025.

Frequently Asked Questions

1. Which securities income was covered under Section 196D of the Income Tax Act?

Section 196D of the Income Tax Act applied to income earned by a Foreign Institutional Investor from securities referred to under Section 115AD. It generally covered dividend and other securities income, except income from units referred to under Section 115AB and interest specifically governed by Section 194LD. Capital gains were excluded from TDS under Section 196D(2).

2. What was the Section 196D TDS rate for Foreign Institutional Investors?

The basic Section 196D TDS rate was 20% on covered securities income paid or credited to a Foreign Institutional Investor. However, a lower DTAA rate could apply when the investor satisfied the treaty conditions and furnished the required tax residency documents.

3. Was TDS deducted on capital gains earned by an FII under Section 196D?

No. TDS under Section 196D of the Income Tax Act was not required on capital gains arising from the transfer of securities referred to under Section 115AD. However, the capital gains could still be taxable in India at the applicable short-term or long-term capital gains rate.

4. Does payment of Securities Transaction Tax provide an exemption under Section 196D?

Payment of Securities Transaction Tax did not independently create a general exemption from TDS under Section 196D of the Income Tax Act. Capital gains were outside the TDS requirement because of the specific wording of the provision, although the gains could remain taxable under the relevant capital gains provisions.

5. Is interest income of an FII always subject to 20% TDS under Section 196D?

No. Interest covered under Section 194LD was subject to a separate concessional TDS provision and was not governed by the general 20% rate under Section 196D of the Income Tax Act. The nature of the security and the applicable section must be checked before deducting tax.

6. When was TDS under Section 196D required to be deducted?

TDS was required to be deducted at the earlier of the date on which the covered income was credited to the account of the FII or the date on which the payment was made through any mode.

7. What documents are required to claim a lower DTAA rate under Section 196D?

An FII claiming a lower DTAA rate generally needs to furnish a valid Tax Residency Certificate and other prescribed information or declarations. The deductor should also examine the applicable treaty article, beneficial ownership conditions and the investor’s eligibility before applying the reduced rate.

8. What was the TDS rate on income paid to a specified fund under Section 196D(1A)?

Section 196D(1A) prescribed a separate TDS rate of 10% on covered securities income paid to a specified fund. No tax was required to be deducted where the income was exempt under Section 10(4D) of the Income-tax Act, 1961.

9. Can Ebizfiling assist with TDS return filing for payments covered under Section 196D?

Yes. Ebizfiling can assist deductors with identifying the applicable TDS provision, reviewing the Section 196D of the Income Tax Act TDS rate, preparing the relevant TDS return and checking PAN, payment and deduction details before filing. The team can also assist with TDS certificates and correction returns where required.

10. Can Ebizfiling help an FII claim DTAA benefits and TDS credit in India?

Yes. Ebizfiling can assist FIIs, FPIs and foreign entities with reviewing DTAA eligibility, checking Tax Residency Certificate documentation and filing the applicable income tax return to report Indian income and claim available TDS credit. The final eligibility depends on the investor’s legal status, income and supporting documents.

File TDS Returns

Quickly file error-free TDS Returns with EbizFiling. This ensures seamless credit to the deductee. Prices Starting INR 999/-.

About Ebizfiling -

Reviews

Amruta Thalange

15 Oct 2020Dev Desai

19 Nov 2021Loves their services

Kalla swathi

09 Apr 2022Excellent service indeed.. I appreciate the entire team for incorporating my company very well

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]