-

July 20, 2026

-

BySteffy A

TDS on Payment under Specified Agreements: Section 194M

Introduction

TDS on payment under specified agreements applies to certain high-value payments made by an individual or Hindu Undivided Family to a resident contractor, professional, commission agent or broker. The purpose of TDS is to collect tax at the time income is credited or paid and provide the recipient with corresponding tax credit.

Under the Income-tax Act, 1961, these payments were governed by Section 194M. With effect from 1 April 2026, the corresponding provision has been renumbered as Section 393(1), Table Serial No. 6(ii) of the Income-tax Act, 2025. The corresponding provision continues to prescribe a TDS rate of 2% and a threshold of ₹50 lakh.

This article explains the applicability, threshold, rate, payment procedure, due dates and consequences of non-compliance relating to TDS on payment under specified agreements.

What is Section 194M of the Income Tax Act?

TDS on Payment under Specified Agreements was governed by Section 194M of the Income-tax Act, 1961. It required an individual or HUF to deduct TDS on specified payments made to a resident when the aggregate amount exceeded ₹50 lakh during a financial year.

The provision applied where the individual or HUF was not otherwise required to deduct tax under the regular provisions relating to contractor payments, professional fees, commission, or brokerage.

Section 194M was introduced to bring certain high-value payments made by individuals and HUFs within the TDS framework. The TDS rate was originally 5% and was reduced to 2% with effect from 1 October 2024.

From 1 April 2026, TDS on Payment under Specified Agreements is covered by Section 393(1), Table Serial No. 6(ii) of the Income-tax Act, 2025.

Applicability of TDS on Payment under Specified Agreements

TDS on payment under specified agreements applies when all the following conditions are satisfied:

- The payer is an individual or Hindu Undivided Family.

- The payer is an individual or HUF who is not required to deduct tax under the regular provisions applicable to contractor payments, commission or brokerage, or professional fees.

- The recipient is a resident.

- The payment relates to contractual work, professional services, commission, or brokerage.

- The aggregate amount paid or credited during the year exceeds ₹50 lakh.

The ₹50 lakh limit is checked based on the aggregate eligible payments made to the recipient during the relevant year.

Once the total eligible amount exceeds ₹50 lakh, TDS is generally required on the entire eligible amount and not merely on the amount exceeding ₹50 lakh.

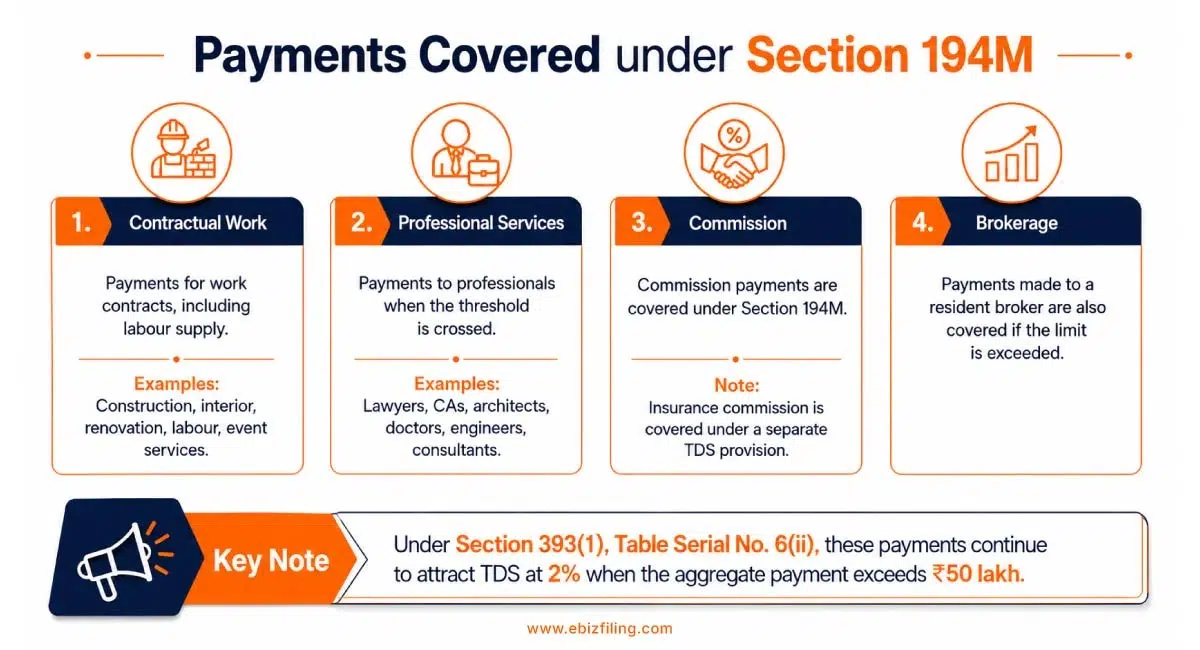

Payments Covered under Section 194M and Section 393(1)

The following payments are covered under TDS on Payment under Specified Agreements:

1. Contractual Work

Payments made for carrying out any work under a contract are covered. The term also includes the supply of labour for carrying out the work.

Examples may include payments made to:

- Construction contractors

- Interior contractors

- Renovation contractors

- Labour contractors

- Event management service providers

2. Professional Services

Payments made for professional services may also attract TDS when the prescribed threshold is crossed.

These may include payments to:

- Lawyers

- Chartered accountants

- Architects

- Doctors

- Engineers

- Management consultants

- Technical consultants

3. Commission

Commission payments are covered, except insurance commission governed by a separate TDS provision.

4. Brokerage

Payments made to a resident broker for specified services may also be covered when aggregate payments exceed ₹50 lakh.

Under Section 393(1), Table Serial No. 6(ii), TDS on Payment under Specified Agreements continues to apply to contractual work, professional services, commission and brokerage at a rate of 2%.

Are Personal Payments Covered?

Yes. The provision is not limited to business or professional payments. It may also apply where an individual makes a high-value payment for a personal purpose.

For example, an individual may engage:

- A contractor to construct a residential house

- An architect to design a personal property

- An interior designer to renovate a home

- A lawyer for personal legal services

- A broker for a specified personal transaction

If the total eligible payment to the resident recipient exceeds ₹50 lakh during the year, the individual may be required to deduct TDS.

Therefore, personal payments should not be treated as automatically excluded from the provision.

When Is the Provision Not Applicable?

TDS under this provision may not apply in the following cases:

- The recipient is a non-resident.

- The aggregate eligible payment does not exceed ₹50 lakh.

- The payment is not for contractual work, professional services, commission, or brokerage.

- The individual or HUF is already required to deduct tax under the regular provisions relating to contractors, commission or brokerage, or professional fees.

- The transaction is covered by a separate withholding tax section.

Payments to non-residents are not covered by the PAN-based challan-cum-statement meant for resident recipients. Separate TDS provisions may apply to such payments.

TDS Rate and Time of Deduction

The current rate of TDS is 2%.

TDS must be deducted at the earlier of:

- The date on which the amount is credited to the account of the recipient; or

- The date on which the payment is made.

- Payment may be made through cash, cheque, bank transfer, or any other mode.

- A higher rate may apply where the recipient does not furnish a valid PAN or furnishes an incorrect PAN.

Example

Suppose an individual credits ₹60 lakh to the account of a resident contractor on 10 May 2026 for constructing a residential house.

Since the credit occurs after 1 April 2026 and the aggregate payment exceeds ₹50 lakh, Section 393(1), Table Serial No. 6(ii) applies.

TDS amount:

₹60,00,000 × 2% = ₹1,20,000

The individual may pay the balance amount to the contractor after deducting the applicable TDS.

Procedure under the Income-tax Act, 1961

For transactions governed by Section 194M under the earlier law, the deductor was required to:

- Deduct TDS at 2%.

- Deposit the tax through Form 26QD.

- File Form 26QD within 30 days from the end of the month in which TDS was deducted.

- Download and issue Form 16D to the recipient.

- Issue Form 16D within 15 days from the due date of Form 26QD.

A TAN was not required because Form 26QD was a PAN-based challan-cum-statement.

Procedure for Tax Year 2026–27 Onwards

From 1 April 2026, TDS on Payment under Specified Agreements is governed by Section 393(1), Table Serial No. 6(ii) of the Income-tax Act, 2025. The related forms and rules have also been restructured.

|

Earlier provision, form or rule |

From 1 April 2026 |

|

Section 194M |

Section 393(1), Table Serial No. 6(ii) |

| Form 26QD |

Form 141, Schedule C |

|

Form 16D |

Form 132 |

| Rule 30(2C) and Rule 31A(4B) |

Rules 218(3) and 219(5) |

|

Rule 31(3B) |

Rule 215 |

Forms 26QB, 26QC, 26QD, and 26QE have been combined into the consolidated Form 141. Contract payments, professional fees, commission and brokerage covered by Section 393(1), Table Serial No. 6(ii), must be reported through Schedule C of Form 141.

Form 141 is a PAN-based challan-cum-statement and must be filed electronically within 30 days from the end of the month in which TDS is deducted. The deductor is not required to obtain a TAN.

After Form 141 has been filed and successfully processed, the deductor must generate or download Form 132 from the portal prescribed by the Income Tax Department. The certificate may be authenticated manually or digitally and must be issued to the recipient within 15 days from the due date for filing Form 141.

Taxpayers can also refer to the complete guide on new TDS and TCS forms under the Income Tax Act to understand the revised form numbers applicable from 1 April 2026.

Consequences of Non-Compliance

Failure to comply with TDS may result in:

- Interest for delay in deducting tax

- Interest for delay in depositing the deducted amount

- Late filing fees for delayed submission of the challan-cum-statement

- Penalty for failure to deduct or deposit TDS

- Difficulty for the recipient in claiming TDS credit

- Tax notices or compliance proceedings

An incorrect PAN may prevent the TDS credit from appearing in the recipient’s tax records. It may also result in the application of a higher TDS rate.

The deductor should therefore verify the recipient’s PAN, payment amount, date of deduction and transaction category before filing the applicable form.

Get Professional TDS Filing Support from Ebizfiling

Compliance with TDS on Payment under Specified Agreements requires correct identification of the applicable provision, accurate TDS calculation and timely filing of the prescribed form.

Ebizfiling can assist with:

- TDS applicability, rate and threshold review

- Form 141 filing and TDS payment support

- Form 132 download and issuance guidance, along with Form 141 correction support

- Assistance with PAN errors, delayed filings and TDS notices

Use Ebizfiling’s TDS Return Filing Service to calculate the applicable tax, file Form 141 within the due date and complete your TDS compliance accurately.

Conclusion

TDS on payment under specified agreements applies to high-value payments made by specified individuals and HUFs to resident contractors, professionals, commission agents and brokers. The provision becomes applicable when aggregate eligible payments exceed ₹50 lakh during the year, and tax must be deducted at 2%. Personal payments may also fall within its scope.

Under the earlier Income-tax Act, 1961, this requirement was governed by Section 194M, Form 26QD and Form 16D. From 1 April 2026, it is governed by Section 393(1), Table Serial No. 6(ii), Form 141 and Form 132. Proper and timely compliance helps prevent interest, fees, penalties and TDS credit-related issues.

Frequently Asked Questions

1. Who must deduct TDS on payment under specified agreements?

TDS must be deducted by an individual or HUF making covered payments to a resident contractor, professional, commission agent or broker where the payer is not already required to deduct TDS under the regular provisions and the aggregate payment exceeds ₹50 lakh.

2. What is the Section 194M threshold limit?

The Section 194M threshold limit is ₹50 lakh during a financial year. The limit is calculated on the aggregate amount paid or credited to a resident recipient for covered services during the year.

3. Is TDS deducted only on the amount exceeding ₹50 lakh?

No. Once the aggregate eligible payment exceeds ₹50 lakh, TDS is generally deducted on the entire payment amount and not only on the portion exceeding ₹50 lakh.

4. What is the Section 194M TDS rate?

The TDS rate under Section 194M was 5% up to 30 September 2024 and 2% from 1 October 2024. The corresponding provision under Section 393(1), Table Serial No. 6(ii), also prescribes a rate of 2%.

5. Does TDS under Section 194M apply to personal house construction?

Yes. TDS on Payment under Specified Agreements may apply when an individual pays more than ₹50 lakh to a resident contractor, architect or interior designer for constructing, renovating or designing a personal residential property.

6. Is TDS applicable on professional fees paid to a lawyer or architect?

Yes. TDS on professional fees may apply where payments made to a resident lawyer, architect, doctor, engineer, consultant or other specified professional exceed ₹50 lakh during the year.

7. Does Section 194M cover commission or brokerage payments?

Yes. TDS on commission or brokerage is covered when an eligible individual or HUF makes aggregate payments exceeding ₹50 lakh to a resident. Insurance commission is generally covered by a separate TDS provision.

8. What was the due date for filing Form 26QD under Section 194M?

Form 26QD under Section 194M was required to be filed within 30 days from the end of the month in which TDS was deducted. The Form 16D TDS certificate had to be issued within 15 days from the due date of Form 26QD.

9. What provision applies in place of Section 194M from 1 April 2026?

From 1 April 2026, TDS on Payment under Specified Agreements is governed by Section 393(1), Table Serial No. 6(ii) of the Income-tax Act, 2025. Form 26QD has been replaced by Schedule C of Form 141, while Form 16D has been replaced by Form 132. Ebizfiling can assist with identifying and filing the applicable TDS form.

10. What are the consequences of non-compliance with the TDS provisions?

Failure to deduct, deposit or report TDS may result in interest, late filing fees, penalties, tax notices and problems in granting TDS credit to the recipient. Ebizfiling can help with TDS calculations, delayed filings, correction statements and notice-related compliance.

File TDS Returns

Quickly file error-free TDS Returns with EbizFiling. This ensures seamless credit to the deductee. Prices Starting INR 999/-.

About Ebizfiling -

Reviews

Amit Tripathi

01 Jun 2018Easy and Fast Thanks for the Help, Very Nice Services will contact for other services too.

Devang Panchal

09 Sep 2018They helped me with my company’s name change and I was quite satisfied with the way they served me. I am surely coming back to you in case of any compliance problem.

Karthik D

19 Apr 2022Excellent service by the Ebizfiling team while started my companies. They also helped very well with the GST registration and compliance.

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]