-

July 21, 2026

-

BySteffy A

Section 194C of the Income Tax Act: TDS on Contractor Payments

Introduction

Section 194C of the Income Tax Act governed tax deducted at source, or TDS, on payments made to resident contractors for carrying out contractual work. It also covered subcontract arrangements because the term “contract” included a subcontract.

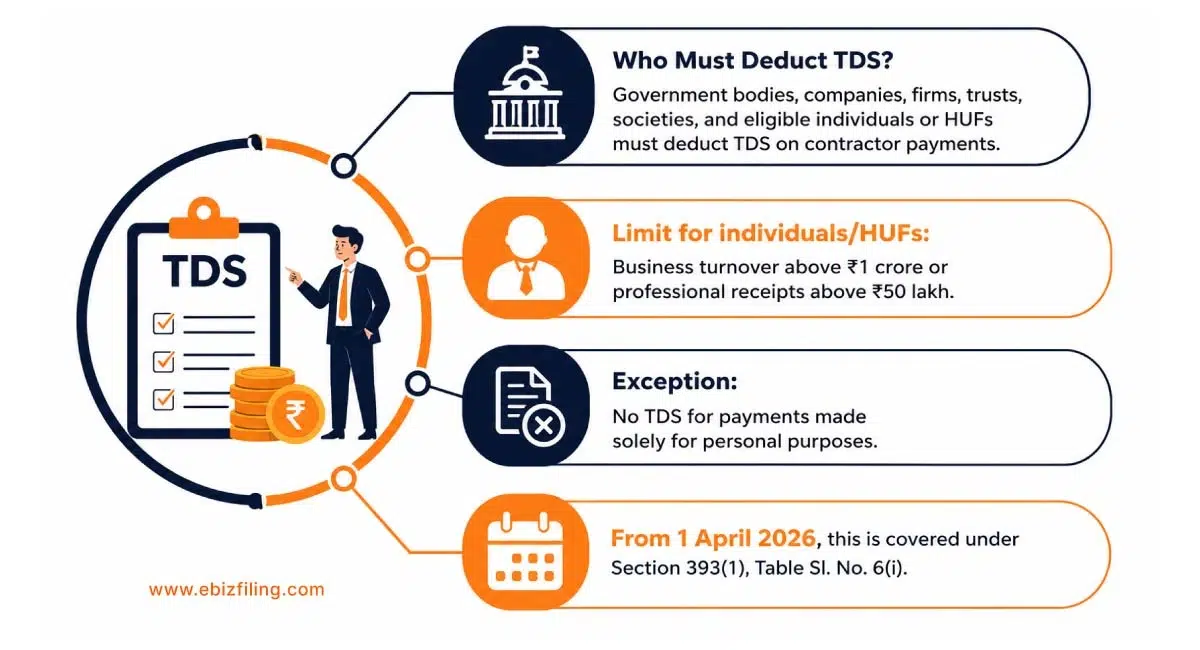

Section 194C applied under the Income-tax Act, 1961 to contractor payments credited or paid up to 31 March 2026. For payments credited or paid on or after 1 April 2026, the corresponding provision is Section 393(1), Table Serial No. 6(i) of the Income-tax Act, 2025. The Income Tax Department has clarified that the applicable contractor-payment rates and monetary limits remain unchanged under the new Act.

This article explains the applicability of Section 194C of the Income Tax Act, TDS rates, payment limits, exemptions, contractor and subcontractor payments, and TDS certificate requirements.

Meaning of Section 194C of the Income Tax Act

Under Section 194C of the Income Tax Act, a person responsible for paying a resident contractor for carrying out any work under a contract was required to deduct TDS.

TDS was required to be deducted at the earlier of the following:

- When the amount was credited to the contractor’s account; or

- When the payment was made in cash, by cheque, draft, bank transfer, or any other mode.

Where the amount was credited to a suspense account or any other account in the payer’s books, it was treated as a credit to the contractor’s account. TDS could therefore become applicable even if the amount had not yet been paid to the contractor.

Under the Income-tax Act, 2025, the same credit-or-payment principle applies to contractor payments under Section 393. A credit to a suspense account or another account is also treated as a credit to the payee.

Who Was Required to Deduct TDS Under Section 194C?

Section 194C of the Income Tax Act did not apply to every person making a contractor payment. The payment was required to be made under a contract between the contractor and a specified person.

Specified persons included:

- The Central Government or a State Government;

- A local authority;

- A statutory corporation;

- A company;

- A cooperative society;

- Certain housing or development authorities;

- A registered society;

- A trust;

- A university or specified educational institution;

- A foreign government, foreign enterprise, or body established outside India;

- A partnership firm; and

- Certain individuals, HUFs, associations of persons, and bodies of individuals.

An individual, HUF, AOP, or BOI was generally covered where the previous year’s turnover exceeded ₹1 crore in the case of business or gross receipts exceeded ₹50 lakh in the case of a profession. However, an individual or HUF was not required to deduct TDS where the contractor payment was made exclusively for personal purposes.

From 1 April 2026, Section 393(1), Table Serial No. 6(i) uses the term “designated person” for the payer responsible for deducting TDS on contractor payments.

Where an individual or HUF was not covered by the regular Section 194C requirements, a contractor or professional payment exceeding ₹50 lakh could attract TDS under Section 194M. From 1 April 2026, the corresponding provision is Section 393(1), Table Serial No. 6(ii) of the Income-tax Act, 2025.

What Is Considered “Work” for Contractor TDS?

For Section 194C of the Income Tax Act applicability, the expression “work” included:

- Advertising;

- Broadcasting and telecasting, including programme production;

- Carriage of goods or passengers by any mode other than railways;

- Catering;

- Supply of labour for carrying out work; and

- Manufacturing or supplying a product according to a customer’s specifications by using material purchased from that customer or its associate.

The provision did not generally cover the manufacture or supply of a product where the contractor purchased the required material from an unrelated person.

Payments covered as professional services, technical services, royalty, or other specified payments under Section 194J were also excluded from the definition of “work” under Section 194C of the Income Tax Act.

TDS on Payments to Subcontractors

Section 194C of the Income Tax Act also covered payments made under subcontract arrangements because the statutory definition of “contract” included a subcontract.

Therefore, where a person covered by the provision paid a resident subcontractor for carrying out the whole or part of the contractual work, TDS was required to be deducted at the time of credit or payment, whichever occurred earlier.

The TDS rate depended on the legal status of the subcontractor. It was not automatically 1% merely because the payment was made to a subcontractor.

TDS Rates for Contractors Under Section 194C of the Income Tax Act

The applicable TDS rates were:

|

Status of contractor or subcontractor |

TDS rate |

|

Individual or HUF |

1% |

|

Company, partnership firm, LLP, AOP, BOI, or any other person |

2% |

| PAN not furnished or invalid |

20% |

Where PAN was not furnished, tax was required to be deducted at the higher of the rate under the relevant provision, the rates in force, or 20%. For an ordinary contractor payment, this generally resulted in TDS at 20%.

The same basic rates and monetary limits apply under Section 393(1), Table Serial No. 6(i) of the Income-tax Act, 2025.

Section 194C Threshold Limit

TDS on payment to contractors was subject to two separate monetary limits.

Single-payment limit

TDS was not required where a single sum credited or paid to the contractor did not exceed ₹30,000.

However, the annual aggregate limit also had to be considered.

Annual aggregate limit

TDS became applicable where the total amount credited, paid, or likely to be credited or paid to the contractor during the financial year exceeded ₹1,00,000.

Therefore, TDS was required in either of the following situations:

- A single payment exceeded ₹30,000; or

- Aggregate payments during the year exceeded ₹1,00,000, even if each individual payment was ₹30,000 or less.

These limits have been retained under Section 393(1), Table Serial No. 6(i).

Cases Where TDS Is Not Deductible

1. Payments remain within both monetary limits

TDS is not required where:

- No single payment exceeds ₹30,000; and

- Total payments during the year do not exceed ₹1,00,000.

If either limit is crossed, the deductor must examine and apply the TDS requirement.

2. Payment is made for personal purposes

An individual or HUF is not required to deduct TDS where the contractor payment is made exclusively for the personal purposes of the individual or a member of the HUF.

For example, an individual engaging a contractor for purely personal residential work may fall under this exclusion, subject to the facts and nature of the arrangement.

3. Payment is made to an eligible goods carriage contractor

TDS is not required on payments made to a contractor engaged in plying, hiring, or leasing goods carriages where:

- The contractor owns ten or fewer goods carriages at any time during the year;

- The contractor provides a valid PAN;

- The contractor provides the prescribed declaration; and

- The payer reports the prescribed particulars to the Income Tax Department.

PAN alone is not sufficient. The prescribed declaration must also be obtained, and the reporting requirement must be followed.

4. Lower or nil deduction certificate

A contractor may apply for a certificate authorizing deduction of tax at a lower rate or without deduction where the estimated tax liability justifies such treatment. Under the Income-tax Act, 1961, the application was made in Form 13 under Section 197. From 1 April 2026, the application must be made in Form 128 under Section 395(1) of the Income-tax Act, 2025. The payer should apply the lower or nil rate only after receiving and verifying a valid certificate.

TDS on Material Supplied by the Customer

Special rules applied where a contractor manufactured or supplied a product according to the customer’s requirements by using material purchased from the customer or its associate.

Where the material value was shown separately in the invoice, TDS was deducted on the invoice value excluding the separately stated material value.

Where the material value was not shown separately, TDS was deducted on the entire invoice value.

Due Date for Issuing the TDS Certificate

For contractor payments governed by the Income-tax Act, 1961, the deductor was required to issue a quarterly TDS certificate in Form 16A.

Form 16A was required to be issued within 15 days from the due date for furnishing the relevant quarterly TDS statement.

From 1 April 2026, Form 16A has been replaced by Form 131 under the Income-tax Rules, 2026. Form 131 is also required to be issued within 15 days from the due date for filing the quarterly TDS statement.

|

Quarter |

Period |

Due date for issuing Form 16A/Form 131 |

|

Quarter 1 |

April to June | 15 August |

| Quarter 2 | July to September |

15 November |

|

Quarter 3 |

October to December | 15 February |

| Quarter 4 | January to March |

15 June following the relevant year |

The official guidance for Form 131 confirms these quarter-wise issuance dates.

Deductors should also monitor the applicable TDS return due dates, as Form 131 can be generated only after the relevant quarterly TDS statement has been filed and processed.

Form 140 for Contractor TDS Statements

For resident contractor payments under the Income-tax Act, 1961, the quarterly TDS statement was generally filed in Form 26Q.

From 1 April 2026, Form 26Q has been renumbered as Form 140. Form 140 is the quarterly statement for tax deducted on payments other than salary, including applicable payments to resident contractors.

For resident contractor payments, Form 131 can be generated through the TRACES portal only after the quarterly TDS statement in Form 140 has been filed and processed.

Ebizfiling Support for TDS Return Filing

Ebizfiling assists businesses, contractors, and deductors with TDS return filing and contractor-payment reporting.

Our support includes:

- Preparation and filing of the applicable quarterly TDS statement;

- Verification of PAN, challan, payment, and deduction details;

- Reporting of contractor and subcontractor payments;

- Assistance with generating the applicable TDS certificate; and

- Filing correction statements where errors are identified.

Need assistance with TDS return filing? Ebizfiling can help you prepare Form 140, verify contractor-wise deductions and generate Form 131 after processing of the quarterly statement.

Conclusion

Section 194C of the Income Tax Act governed TDS on payments credited or paid to resident contractors up to 31 March 2026. The payer was required to examine the nature of the work, the status of the contractor, the applicable payment limits, the timing of credit or payment, PAN details, and available exclusions before deducting tax.

For payments credited or paid on or after 1 April 2026, TDS on contractor payments is governed by Section 393(1), Table Serial No. 6(i) of the Income-tax Act, 2025. The basic TDS rates and monetary limits remain unchanged, but deductors must use the new section and form references while depositing and reporting TDS.

Frequently Asked Questions

1. If every contractor invoice is below ₹30,000 but annual payments exceed ₹1,00,000, is TDS applicable?

Yes. TDS under Section 194C of the Income Tax Act becomes applicable where aggregate payments to the contractor during the year exceed ₹1,00,000, even if each individual invoice is ₹30,000 or less.

2. Is the Section 194C threshold calculated separately for each contractor?

Yes. The limits are generally monitored contractor-wise. The deductor should examine both the amount of each payment and the aggregate payments made or likely to be made to that contractor during the year.

3. Which TDS rate applies to a sole proprietorship contractor?

A sole proprietorship does not have a separate legal identity from its individual proprietor. Therefore, the TDS rate is generally 1% where the payee’s status and PAN confirm that the contractor is an individual. A rate of 2% generally applies where the contractor is a company, partnership firm, LLP, AOP, BOI, or another non-individual person.

4. Is TDS required on an advance paid to a contractor?

Yes. TDS under Section 194C of the Income Tax Act is deducted at the time of credit or payment, whichever occurs earlier. Therefore, an advance payment may attract TDS even where the work has not yet been completed.

5. Is TDS applicable when the contractor’s amount is credited to a suspense account?

Yes. A credit to a suspense account or any other account in the payer’s books is treated as a credit to the contractor’s account. Therefore, TDS under Section 194C of the Income Tax Act must be considered at the time of such credit, even if the payment has not yet been made.

6. How is TDS calculated when the contract includes material supplied by the customer?

Where the material value is separately stated in the invoice, TDS is deducted on the invoice amount excluding that material value. Where it is not stated separately, TDS is deducted on the complete invoice value.

7. Can a goods carriage contractor claim exemption merely by providing PAN?

No. Under Section 194C of the Income Tax Act, the contractor must satisfy the goods-carriage ownership condition and furnish both the prescribed declaration and PAN. The payer must also report the required particulars to the Income Tax Department.

8. Can Form 131 be issued before filing the quarterly TDS statement?

No. For resident contractor payments, Form 131 can be generated through the TRACES portal only after the relevant quarterly TDS statement in Form 140 has been filed and processed. Therefore, the deductor cannot issue a valid Form 131 before filing the applicable Form 140.

9. How can an incorrect PAN, TDS rate, or challan entry be corrected?

After the original Form 140 has been processed by CPC-TDS, the deductor may file a correction statement containing the correct PAN, TDS rate, challan, payment, or deduction details. The correction statement must be filed within two years from the end of the tax year in which the original statement was required to be furnished. Ebizfiling can assist with TDS return filing and revision where the original statement contains an incorrect PAN, challan, rate, payment amount or deduction entry.

10. What information is required for TDS return filing for contractors?

TDS return filing for contractors generally requires the contractor’s legal name, PAN, legal status, payment or credit amount, date of payment or credit, applicable TDS provision and rate, amount of tax deducted, date of tax deposit, challan details, and contractor-wise deduction records. Ebizfiling can assist with reviewing these details and preparing and filing the applicable quarterly TDS statement.

TDS Returns

Quickly file error-free TDS Returns with EbizFiling. This ensures seamless credit to the deductee.

About Ebizfiling -

Reviews

Chandrashekhar Nimmalwar

28 Oct 2020(Translated by Google) Ebizfiling has a company providing support for time period service and proper guidance. It is my personal experience at present. Chandrashekhar Nimmalwar. Today Aas Family Foundation (Original) ईबिज फायलीग की सेवा समय अवधि कार्य प्रणाली एव उचित मार्गदर्शन के लिए सहायता प्रदान कम्पनी है।यह मेरा वर्तमान में नीजी अनुभव है। चन्द्रशेखर निममलवार। आज आस परिवार फाउंडेशन

Jaan Hazarika

04 Apr 2022Harish Ji and his team are so quick to forming my PVT LTD company .... I got my Company Incorporated Before my expected time ... I am So glad and Want to see flourish this company more in near future .. Once again Thankyou ebizfilling and all team members ..... ❤️❤️

Kartar Singh Sandil

09 Mar 2018Your working team is genius. Thanks.

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]

August 7, 2026 By Steffy A

Section 134 of the Income Tax Act, 2025: Rent Deduction Rules Introduction Section 134 of the Income Tax Act, 2025 allows eligible assessees to claim a deduction for rent paid for residential accommodation occupied as their own residence. It applies […]

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]