-

July 15, 2026

-

BySteffy A

Section 10AA of the Income Tax Act: SEZ Deduction Guide

Introduction

Section 10AA of the Income Tax Act provides deduction benefits to eligible businesses operating in Special Economic Zones (SEZs). This section was introduced to promote exports, attract investment, and support businesses engaged in manufacturing or providing services from SEZ units.

From April 1, 2026, the corresponding SEZ deduction provisions are contained in Section 144 of the Income-tax Act, 2025. Section 144 broadly continues the deduction framework applicable to eligible SEZ units, subject to the prescribed conditions. The deduction is available on eligible export profits.

This blog explains the meaning of Section 10AA, eligibility criteria, deduction period, calculation method, SEZ reinvestment reserve rules, and the consequences of not using the reserve amount as required.

What Is Section 10AA of the Income Tax Act?

Section 10AA of the Income Tax Act provides deduction benefits to eligible businesses operating in Special Economic Zones (SEZs). It allows eligible SEZ units to claim deduction on export profits, subject to prescribed conditions. The main purpose of this section is to promote exports, attract investment, create employment, and support businesses engaged in manufacturing or providing services from SEZ units.

A Special Economic Zone (SEZ) is a designated area in India established to promote exports by providing businesses with tax incentives and simplified regulatory procedures. SEZs are developed to encourage export-oriented business activity, improve trade balance, attract investment, generate jobs, and ensure better administrative support for businesses.

Note: From April 1, 2026, the corresponding SEZ deduction provisions are contained in Section 144 of the Income tax Act, 2025.

Who Is Eligible for Deduction under Section 10AA?

The deduction is not restricted to one particular business structure. It may be claimed by an assessee that qualifies as an “entrepreneur” under Section 2(j) of the Special Economic Zones Act, 2005 and derives eligible profits from a qualifying SEZ unit. The assessee may be a company, LLP, partnership firm, individual or another legally recognised person, provided all statutory conditions are satisfied.

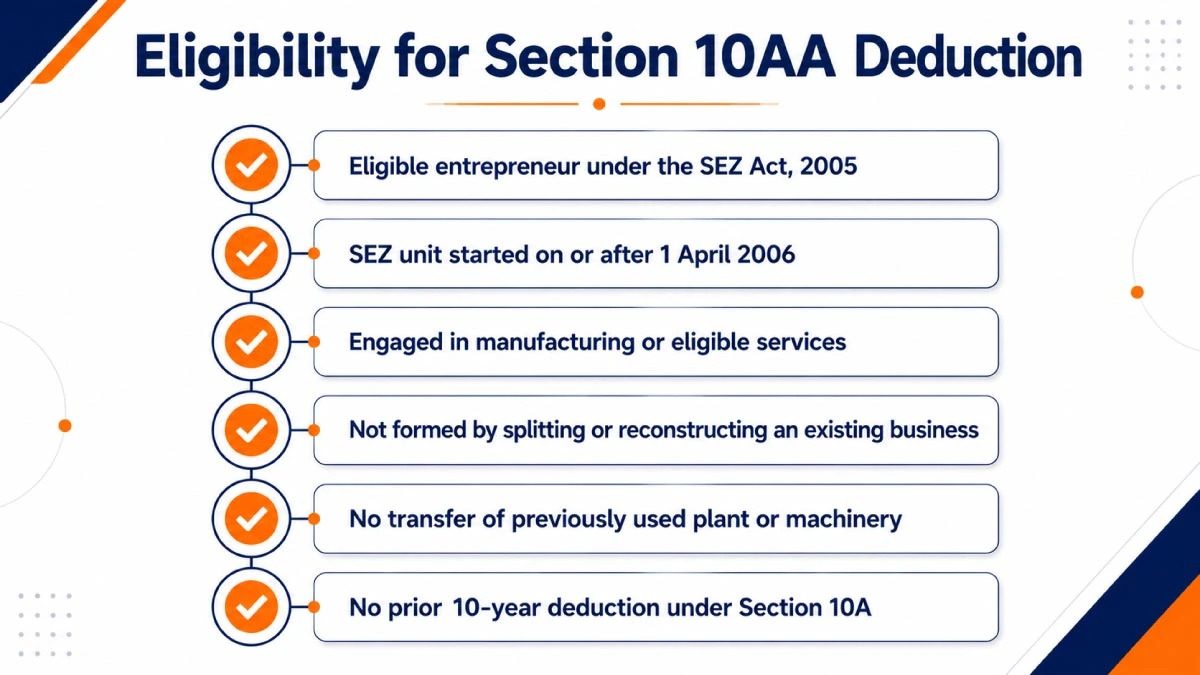

Eligibility Criteria for Deduction under Section 10AA

To claim deduction under Section 10AA of the Income Tax Act, the following conditions should be fulfilled:

- The entrepreneur must be covered under Section 2(j) of the Special Economic Zones Act, 2005.

- The SEZ unit must have begun manufacturing or producing articles or things, or providing services, during the previous year relevant to an assessment year beginning on or after April 1, 2006 but before April 1, 2021. In practical terms, eligible operations must generally have commenced before April 1, 2020, subject to the applicable statutory conditions.

- The SEZ unit must not be formed by splitting up or reconstructing an existing business.

- The unit should not be formed by transferring previously used plant or machinery beyond the limit permitted under the applicable provisions.

- The total deduction period available to an undertaking under the related tax-holiday provisions cannot exceed the prescribed overall period. A unit cannot obtain a fresh deduction cycle under Section 10AA after exhausting the benefit available for the same undertaking under the earlier applicable provision.

Deduction Rate under Section 10AA of the Income Tax Act

The deduction under Section 10AA of the Income-tax Act is available for a specified period beginning with the year in which the eligible SEZ unit starts manufacturing or producing articles or things, or providing services.

|

Time period |

Deduction rate |

|

First 5 consecutive assessment years |

100% of eligible export profits |

| Next 5 consecutive assessment years |

50% of eligible export profits |

|

Further 5 consecutive assessment years |

Deduction limited to the lower of 50% of eligible export profits or the amount transferred to the Special Economic Zone Reinvestment Reserve Account and utilised according to the prescribed conditions. |

How Is the Section 10AA Deduction Calculated?

The deduction under Section 10AA of the Income Tax Act is calculated using the following formula:

Eligible export profit = Profits of the business of the SEZ undertaking × Export turnover of the SEZ undertaking ÷ Total turnover of the SEZ undertaking

Here, export turnover means the consideration received in, or brought into, India for export of goods, articles, things, or services by the SEZ unit. However, export turnover does not include freight, telecommunication charges, insurance expenses for delivery outside India, or expenses incurred in foreign exchange for providing services outside India.

Use of SEZ Reinvestment Reserve

To claim deduction for the further five-year period under Section 10AA of the Income Tax Act, the eligible amount must be transferred to the Special Economic Zone Reinvestment Reserve Account. The following conditions should be followed:

The amount transferred to the reserve must be used for acquiring new plant or machinery for the purposes of the eligible business, and the acquired asset must be put to use within the prescribed period.

The new plant or machinery must be acquired and put to use before the expiry of three years following the end of the year in which the reserve was created.

Until the acquisition of the new plant or machinery, the reserve amount may be used for the business purposes of the undertaking, subject to the prescribed restrictions.

However, the reserve amount cannot be used for distribution of dividends or profits, remittance of profits outside India, or creation of assets outside India.

Consequences of Not Using SEZ Reinvestment Reserve

If the amount credited to the Special Economic Zone Reinvestment Reserve Account is not used for purchasing new plant and machinery within the prescribed time, it will be treated as taxable business income in the year immediately following the expiry of the prescribed three-year period.

If the reserve amount is used for any purpose other than the prescribed purpose, it will be treated as taxable business income in the year in which the amount is used for a non-permitted purpose.

Reporting Requirements for Section 10AA Deduction

A taxpayer claiming deduction under Section 10AA should maintain separate and reliable records for the eligible SEZ undertaking. The records should support the profits of the undertaking, export turnover, total turnover, export proceeds and reserve utilization.

Under the earlier framework, the prescribed accountant’s report in Form 56F must be obtained and furnished within the applicable timeline. The report contains details of the eligible unit, nature of business, commencement date, turnover, export proceeds, and deduction claimed.

From April 1, 2026, taxpayers should follow the corresponding reporting form and procedural requirements prescribed under the Income-tax Act, 2025.

Ebizfiling Support for SEZ Tax Compliance

Ebizfiling helps SEZ units, exporters, companies, and firms manage Section 10AA deduction and related income tax compliance.

Ebizfiling helps businesses with:

- Review of eligibility for Section 10AA deduction

- Export profit calculation support

- ITR filing assistance with CA

- SEZ Reinvestment Reserve compliance

- Tax documentation support

With professional guidance, businesses can claim eligible deductions correctly and avoid errors in reporting or reserve utilization.

Conclusion

Section 10AA of the Income Tax Act provides a phased deduction for eligible export profits earned by qualifying units operating in Special Economic Zones. The deduction is available for up to 15 consecutive years, subject to the commencement cut-off, SEZ approval, business-formation restrictions and other prescribed conditions.

Eligible units may claim a 100% deduction during the first five years, a 50% deduction during the next five years and a reserve-linked deduction during the final five years. The final-phase deduction is subject to the amount transferred to and properly utilised from the Special Economic Zone Reinvestment Reserve Account.

Frequently Asked Answers

1. Can a normal business outside an SEZ claim deduction under Section 10AA?

No, Section 10AA deductions are available only to eligible units operating in a Special Economic Zone. A normal business located outside an SEZ cannot claim this deduction, even if it is engaged in export activity.

2. Is Section 10AA deduction allowed on domestic sales made by an SEZ unit?

No. Section 10AA applies to the eligible export profits of the SEZ undertaking. Profits attributable to domestic tariff area sales do not qualify merely because they are earned by the same SEZ unit. The statutory formula allocates eligible business profits according to the ratio of export turnover to total turnover.

3. From which year does the deduction under Section 10AA start?

The deduction starts from the assessment year relevant to the previous year in which the eligible SEZ unit begins manufacturing or producing articles or things, or providing services. The consecutive deduction period is counted from that year.

4. Can an SEZ unit claim a 100% deduction for all 15 years?

No. A 100% deduction is available only for the first five consecutive assessment years. For the next five years, 50% of eligible export profits may be claimed. For the final five years, the deduction is linked to the amount transferred to and properly utilised from the Special Economic Zone Reinvestment Reserve Account, subject to the prescribed limit.

5. What is the formula for Section 10AA deduction calculation?

The deduction is calculated as: Profit of the SEZ unit × Export Turnover of the SEZ unit / Total Turnover of the SEZ unit. This formula apportions the business profits of the eligible undertaking according to the proportion of its export turnover to its total turnover.

6. Why is the Special Economic Zone Reinvestment Reserve Account important?

The Special Economic Zone Reinvestment Reserve Account is important for claiming deduction during the further five-year period. The eligible amount must be transferred to this reserve and used mainly for purchasing new plant and machinery within the prescribed time.

7. What happens if the reserve amount is used for dividend distribution?

If the amount credited to the Special Economic Zone Reinvestment Reserve Account is used for dividend distribution or profit distribution, it will not be treated as proper utilization. Such amount may become taxable as business income in the year of wrong utilization.

8. Can an SEZ unit formed by transferring old machinery claim Section 10AA deduction?

A unit formed by transferring previously used plant or machinery beyond the permitted limit may not qualify for the deduction. The eligibility must be examined according to the applicable conditions and prescribed threshold.

9. How can Ebizfiling help SEZ units with Section 10AA compliance?

Ebizfiling can help SEZ units review eligibility, calculate export profit, check deduction limits, maintain tax documentation, and support income tax return filing. This helps businesses claim Section 10AA of the Income Tax Act deduction correctly and avoid reporting errors.

10. What is the new section number for Section 10AA under the Income Tax Act, 2025?

From April 1, 2026, the corresponding SEZ deduction provisions are contained in Section 144 of the Income-tax Act, 2025. Eligible SEZ units should use the applicable section reference according to the relevant period while preparing tax computations, documentation and compliance records.

ITR filing

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling

About Ebizfiling -

Reviews

Dhairya Lalan

23 Apr 2022Amazing team. They had a word with me post working hours and solved all my queries related to tax consultancy. I highly recommend the services.

Shailesh Charel

08 Aug 2018So far it's been an amazing experience, I haven't got in touch with anyone after I started using services from EBizfilling. Suhani & Pratima is great at Client Servicing. They were always there for on-demand help. Keep Growing

Swapnil Jani

17 Aug 2017We are very happy with the support and service provide by Ebizfiling. I will surely recommend them to my family and friends.

July 20, 2026 By Steffy A

Form 131 of Income Tax Act: Applicability and Process Introduction Form 131 of Income Tax Act is a TDS certificate for tax deducted from specified income other than salary. The deductor issues it to the deductee as proof that tax […]

July 18, 2026 By Steffy A

Section 196 and 198 of the Income Tax Act 2025: STCG and LTCG Introduction Sections 196 and 198 of the Income-tax Act, 2025 prescribe special tax rates for eligible short-term and long-term capital gains arising from specified equity-related assets. Section […]

July 20, 2026 By Steffy A

The concept of Form 168 of Income Tax Act Explained The Form 168 of Income Tax Act is the Annual Information Statement prescribed under the Income-tax Rules, 2026. It provides taxpayers with a consolidated view of TDS, TCS, tax payments, […]