-

July 22, 2026

-

BySteffy A

TDS on Non Residents Under Section 195 in India Explained

Introduction

The government collects tax at the source of income through TDS. The meaning of TDS on non residents in simple terms is the deduction of a specific percentage of tax during the making of payments particularly those cross-border.Also, It applies to other payments like interest, royalty, fees on technical services and other incomes subject to tax in India. In this paper, we describe TDS on payment to non-residents made under Section 195.

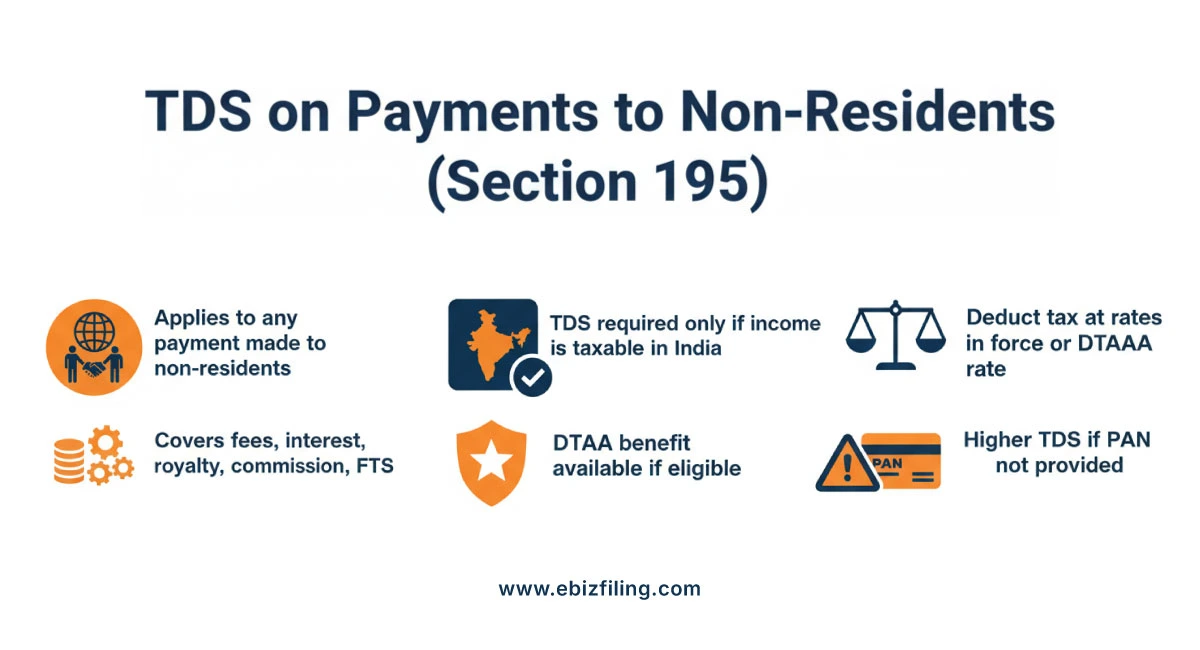

Knowledge of TDS on non residents regulations in Section 195

Section 195 is applicable to any individual, Hindu Undivided Family (HUF), partnership firm, limited liability partnership (LLP), Indian or foreign company, government, bank or any other legal person that pays payments to a non-resident, other than payment of salaries, provided that the income is subject to taxation under the Act.

Whereas, Some of the payments covered by the provision are interest, dividends, royalty, technical services fees, and even capital gains. that mean, most important income should be taxable in India. Although the payer may not have a taxable presence in India, they might have to deduct TDS on non residents payments.

Who is a Non-Resident?

It is crucial to know who is considered to be a non-resident under the Income Tax Act, 1961 before knowing about TDS on non residents payments.

An individual is considered a non- resident when he fails to meet the residence requirements laid down in Section 6 of the Act. Although such basic conditions need to stay in India for 182 days or 60 days and 365 days, there are also significant exceptions of Indian citizens who leave India to work and persons of Indian origin who visit India and cases of deemed residence.

Thus, residential status must be closely decided with reference to the facts of a particular case.

Provisions of TDS on Payment of Any Other Sum to a Non-Resident

Section 195 provides that the TDS on non residents payments is subject to the provisions of the Income Tax Act, 1961. It stipulates that any individual who pays money to a non-resident must reduce the tax at source in case the income is liable to tax in India.

The provision of any other sum is very broad and includes professional fees, commission, brokerage, interest, royalty and fees on technical services as long as it is taxable in India.

Not all cases have a fixed rate of TDS of 30 percent. It is deductible at the rates applicable, at either the Income Tax Act rates or relevant Double Taxation Avoidance Agreement, whichever is more favorable to the non-resident.

In case the non-resident fails to furnish a Permanent Account Number (PAN), increased TDS on non residents could be charged according to Section 206AA, to the same extent as applicable and under judicial interpretations.

TDS on Non Residents Rates

|

Nature of Income |

TDS Rate |

|

Interest income |

20% |

|

Dividend income |

20% |

|

Royalty |

20% |

|

Fees for technical services |

20% |

|

Long-term capital gains |

12.5% |

|

Short-term capital gains (specified cases) |

20% |

|

Any other income |

30% |

Note:

These are commonly applicable base rates for TDS on non residents. The final TDS rate includes the applicable surcharge and 4 percent health and education cess. If a DTAA exists, the non-resident can choose the lower treaty rate. However, they must meet eligibility conditions and provide the required documentation to claim this benefit.

Why Choose Ebizfiling for TDS Compliance?

At Ebizfiling, we assist businesses to deal with complicated TDS requirements on non-resident remittances with clarity and precision.

- Special advice on applicability of Section 195.

- Tax planning and evaluation of DTAA.

- Help with the filing of Form 15CA and Form 15CB.

- Proper calculation and record keeping of TDS.

- Assistance with notices and compliance.

- End-to-end compliance management.

Final Thoughts

TDS on non residents payment under Section 195 is a subject that needs close consideration of the taxability, rate and benefits of treaties. Companies need to realize that the regulations are not necessarily that simple, and they can be subject to fines or reimbursement of costs in case of wrong deduction. In order to be compliant, they ought to ensure that they keep the right records and use the right TDS rates. Businesses should consult professionals to avoid errors and ensure compliance.

Suggested Reads:

TDS on payment to Non-Resident Sportsmen

Tax withholding on Foreign Payments- TDS on Foreign Payments

Section 194O of Income Tax Act

Frequently Asked Questions

1. When does Section 195 provide that TDS is required?

TDS under Section 195 applies only when the payment made to a non-resident is taxable in India. The payer must first determine the taxability of the income, as not all foreign payments are subject to TDS. Proper evaluation helps avoid compliance issues and penalties.

2. What is the rate of TDS on foreign payments?

TDS on non-residents is generally deducted at 20% under Section 195. However, DTAA benefits may allow a lower rate depending on eligibility. The final rate also includes applicable surcharge and 4% cess, and treaty provisions should always be checked before deduction.

3. How is TDS calculated on NRI property transactions?

TDS on property transactions involving non-residents is ideally calculated on capital gains. However, buyers often deduct TDS on the total sale value due to uncertainty in gain calculation. A lower deduction certificate can help ensure accurate TDS computation.

4. What is the effective TDS rate?

The effective TDS rate includes the base rate along with surcharge and a 4% health and education cess. The final rate varies depending on the recipient’s status and must be calculated on a case-by-case basis.

5. Is TDS applicable on services rendered outside India?

TDS may not apply if services are rendered entirely outside India, provided the income is not taxable in India. Section 195 requires careful evaluation of taxability based on the specific facts of each case.

6. Can TDS be reduced or avoided?

TDS on non-residents can be reduced by claiming DTAA benefits or obtaining a lower deduction certificate from the tax authority. Proper documentation is required to avail these benefits and avoid excess tax deduction.

7. What are the consequences of incorrect TDS deduction?

Incorrect TDS deduction may lead to interest, penalties, and disallowance of expenses. It can also result in notices from the tax department, increasing the compliance burden on the payer.

8. Do non-residents need a PAN for TDS?

In the absence of PAN, TDS may be deducted at a higher rate. However, DTAA benefits may still be available if supported by documents such as a Tax Residency Certificate and Form 10F. Having PAN simplifies compliance and refund processes.

9. What are the compliance steps under Section 195?

Compliance includes deducting TDS at the correct rate at the time of payment or credit, depositing the tax within prescribed timelines, and filing returns. Forms 15CA and 15CB may also be required for foreign remittances.

10. What is the importance of DTAA in TDS?

DTAA helps non-residents reduce tax liability by allowing them to apply more beneficial tax rates. Proper documentation is required to claim treaty benefits, which helps avoid double taxation on cross-border income.

File TDS Returns

Quickly file error-free TDS Returns with EbizFiling. This ensures seamless credit to the deductee. Prices Starting INR 999/-.

About Ebizfiling -

Reviews

Akshay shinde

23 Apr 2019Excellent service…

August 1, 2026 By Steffy A

Section 153 of the Income Tax Act, 2025: Interest Deduction Introduction Section 153 of the Income tax Act, 2025 allows eligible individuals and HUFs to claim a deduction on interest from specified deposits. The limit is ₹10,000 for non-senior individuals/HUFs […]

July 31, 2026 By Steffy A

Section 123 of the Income tax Act, 2025: ₹1.5 Lakh Deduction Limit Introduction Section 123 of the Income Tax Act, 2025 allows individuals and Hindu Undivided Families to claim a deduction for specified investments and payments. It broadly continues the […]

July 31, 2026 By Steffy A

Section 186 of the Income Tax Act, 2025: Cash Receipt Limit Introduction Section 186 of the Income Tax Act, 2025 restricts a person from receiving ₹2 lakh or more through cash or any other non-permitted mode. The restriction applies based […]