-

July 1, 2026

-

BySteffy A

Form 66 of the Income Tax Act: MAT Filing & Applicability

Introduction

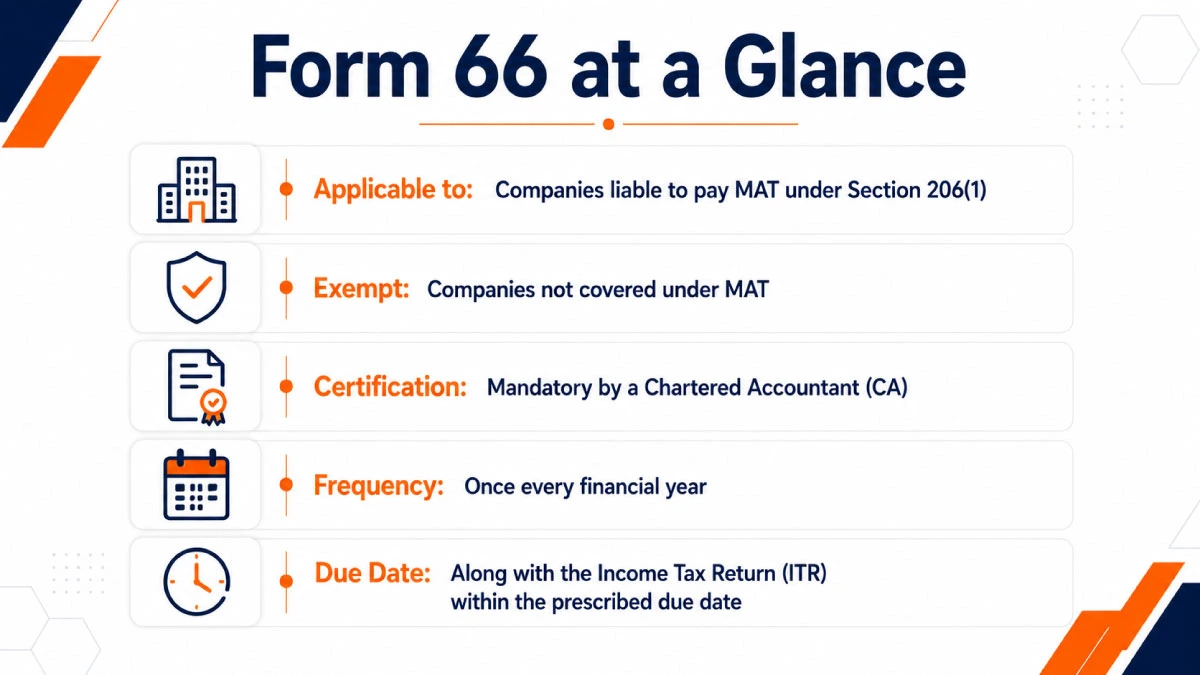

Form 66 of the Income Tax Act is the prescribed report for Minimum Alternate Tax (MAT) under Section 206(1) of the Income Tax Act, 2025. It corresponds to the earlier Form 29B prescribed under the Income-tax Rules, 1962, which has been renumbered as Form 66 under the Income-tax Rules, 2026. Companies liable to pay MAT must obtain this report from a Chartered Accountant before filing their Income Tax Return.

If your company is liable to pay MAT, this guide explains who needs to file Form 66, the due date, required documents, and the filing process under the Income Tax Act, 2025.

What is Form 66 of the Income Tax Act, 2025?

Form 29B of the Income Tax Act has been renumbered as Form 66 of the Income Tax Act, 2025. Although the form number has changed, businesses continue to use it for the same purpose. Under Rule 137 of the Income-tax Rules, 2026, Form 66 is used to report Book Profit and MAT under Section 206(1).

Book Profit: It is the profit shown in a company’s profit and loss account, adjusted by specified additions and deductions under Section 206.

Minimum Alternate Tax (MAT): MAT ensures that companies having book profits pay a minimum amount of tax even when deductions significantly reduce their normal tax liability.

Form 29B vs Form 66: What has changed?

|

Particulars |

Form 29B |

Form 66 |

|

Applicable Law |

Income Tax Act, 1961 |

Income Tax Act, 2025 |

|

Income-tax Rules |

Income-tax Rules, 1962 |

Income-tax Rules, 2026 |

|

Form Number |

Form 29B |

Form 66 |

|

Relevant Rule |

Rule 40B |

Rule 137 |

|

Relevant Section |

Section 115JA, Section 115JAA, Section 115JB |

Section 206(1) |

|

Purpose |

Report for computation of Book Profit and Minimum Alternate Tax (MAT) |

Report for computation of Book Profit and Minimum Alternate Tax (MAT) |

|

Filing Requirement |

Chartered Accountant (CA) Certification Required |

Chartered Accountant (CA) Certification Required |

Applicability of Form 66 of the Income Tax Act, 2025

Form 66 applies to companies liable to pay MAT under Section 206(1) of the Income Tax Act, 2025. The points below cover who needs to file Form 66, the due date, and the certification requirements.

Who is required to file Form 66?

Companies covered under Section 206(1) must obtain Form 66 from a practicing Chartered Accountant before filing their Income Tax Return. It is a report obtained from a Chartered Accountant certifying that the computation of Book Profit and the corresponding MAT liability is in accordance with the provisions of the Act and Rules.

Due date for furnishing Form 66

Form 66 of the Income Tax Act is to be filed annually, along with the Income Tax Return (ITR) of the company.

|

Event |

Due Date |

|

Furnishing Form 66 (electronically signed by CA) |

On or before the prescribed due date for furnishing the audit report under the Income Tax Act, 2025. |

|

Due date (where tax audit is applicable) |

31 October of the relevant Assessment Year |

Structure of Form 66

Form 66 of the Income Tax Act comprises the following sections:

Report under Section 206(1), which is essentially in the nature of certification by a Practicing Chartered Accountant.

The report comprises mainly five parts, as mentioned below:

Part A – General Information: Name, address, PAN, contact details of the company, tax year, and accounting year followed.

Part B – Book Profit Details: Information about Net Profit as per the Profit & Loss Account, details and effect of changes adopted (if any) in the accounting policies during the year, followed by adjustments to Book Profit as per Section 206(1)(c).

Part C – Transition Amount: Computation of transition amount as per Section 206(1)(t).

Part D – MAT Computation: Final computation of Book Profit and the Minimum Alternate Tax payable as per the type of assessee company.

Part E – Auditor’s Certification: Certification by the Practicing Chartered Accountant regarding the computation of Book Profit as per the statutory provisions.

How to Prepare and File Form 66 Online

A practicing Chartered Accountant prepares Form 66 after computing the company’s Book Profit and MAT liability under Section 206(1). The report certifies the computation of Book Profit and MAT liability and is filed electronically through the Income Tax e-Filing portal. Before submission, the company should ensure that all financial information, statutory adjustments, and supporting documents are complete and consistent with the Income Tax Return.

Details and Documents Required

The following documents and details are required for filing Form 66:

- Audited Financial Statements (Profit & Loss Account and Balance Sheet)

- Computation of total income and Book Profit under Section 206(1)

- Details of adjustments made to arrive at Book Profit

- Tax audit details, wherever applicable.

- Digital Signature Certificate (DSC) of both the Chartered Accountant and the company

- PAN and registration details of the company

Form 66 of the Income Tax Act Filing Process

- Preparation of Report: Chartered Accountant computes Book Profit under Section 206(1) and prepares Form 66 using the prescribed utility on the e-Filing portal.

- Digital Signature by CA: The Chartered Accountant verifies and digitally signs Form 66 using the registered DSC.

- Submission by the Company: The company accepts the report in its e-Filing account before filing the Income Tax Return.

- Linking with ITR: Once accepted, the acknowledgement number of Form 66 is automatically linked with the Income Tax Return.

- Processing by CPC: After submission, the Income Tax Department verifies the details furnished in Form 66 along with the Income Tax Return.

Simplify Corporate Tax Compliance with Ebizfiling

Ebizfiling helps businesses stay updated with changing tax and regulatory requirements under the Income Tax Act, 2025.

How we can assist you:

- Guidance on corporate tax compliance requirements

- Support with statutory documentation

- Assistance in understanding regulatory changes

- Access to experienced tax and compliance professionals

- Reliable resources on Income Tax and MCA compliances

If your company is liable to pay Minimum Alternate Tax (MAT), our experts can help you with documentation, CA coordination, and timely filing.

You can also explore our Online CA Consultation for ITR service for personalized tax guidance.

Conclusion

Form 66 of the Income Tax Act is the prescribed report for companies liable to pay Minimum Alternate Tax (MAT) under Section 206(1) of the Income Tax Act, 2025.Companies liable to pay MAT under Section 206(1) should obtain Form 66 from a Chartered Accountant, verify the computation of Book Profit, and file it within the prescribed due date to ensure smooth Income Tax Return processing and compliance.

Frequently Asked Questions

1. When should a company obtain Form 66 of the Income Tax Act?

Companies liable to pay MAT should obtain Form 66 before filing their Income Tax Return. The report must be prepared and certified by a practicing Chartered Accountant and accepted through the Income Tax e-Filing portal within the prescribed timeline.

2. Is Form 66 filing mandatory for every company?

No. Form 66 filing is mandatory only for companies that are liable to pay Minimum Alternate Tax (MAT) under Section 206(1) of the Income Tax Act, 2025. If MAT provisions do not apply to your company, filing Form 66 is generally not required.

3. Can Form 66 filing online be completed without a Chartered Accountant?

Form 66 filing online requires certification by a practicing Chartered Accountant. The CA prepares, verifies, and digitally signs the report before it is accepted by the company on the Income Tax e-Filing portal and linked with the Income Tax Return (ITR).

4. What happens if a company does not file Form 66 when it is applicable?

Failure to furnish Form 66 where applicable may affect the processing of the Income Tax Return and may result in consequences under the Income Tax Act, 2025.

5. Can Form 66 be filed without calculating Book Profit?

The primary purpose of Form 66 of the Income Tax Act is to certify the computation of Book Profit and the corresponding Minimum Alternate Tax (MAT) liability under Section 206(1). Without calculating Book Profit as prescribed, Form 66 cannot be prepared or furnished.

6. Can a company revise Form 66 after it has been submitted?

If any error is identified after submission, the company should consult its Chartered Accountant and follow the revision or correction process, if permitted, on the Income Tax e-Filing portal.

7. Does Form 66 need to be filed every year?

Yes. If a company is liable to pay MAT during a financial year, Form 66 is required for the relevant assessment year. Since MAT applicability is determined annually, companies should review their tax position each year before filing their Income Tax Return.

8. What are the common mistakes to avoid while filing Form 66 online?

While Form 66 filing online, companies should avoid errors such as incorrect Book Profit computation, omission of statutory adjustments, mismatch with audited financial statements, incorrect PAN details, or delays in obtaining the Chartered Accountant’s certification. Ebizfiling helps businesses understand these requirements and complete the filing process with greater accuracy.

9. What details should be verified before submitting Form 66 under the Income Tax Act?

Before submitting Form 66 under the Income Tax Act, companies should verify their audited financial statements, Book Profit computation, MAT calculation, tax audit details, PAN, and supporting documents. Accurate information helps ensure smooth processing of the Income Tax Return and reduces the possibility of notices due to mismatches.

10. What documents should be kept ready before filing Form 66 under the Income Tax Act?

Before filing Form 66, keep audited financial statements, Book Profit computation, the tax audit report, PAN details, and valid DSCs ready. If you need assistance, Ebizfiling can help you understand the documentation and filing requirements.

File Your Income Tax Return with Expert Assistance

Our tax experts help individuals and businesses file Income Tax Returns accurately, on time, and in compliance with applicable tax laws.

About Ebizfiling -

July 23, 2026 By Steffy A

Section 202 of the Income Tax Act, 2025: Tax Slabs and Rules Introduction Section 202 of the Income Tax Act 2025 contains the provisions governing the new tax regime for individuals, Hindu Undivided Families, Associations of Persons, Bodies of Individuals, […]

July 22, 2026 By Steffy A

Section 332 of the Income Tax Act 2025: NPO Registration Introduction Section 332 of the Income Tax Act 2025 provides the registration framework for eligible non-profit organizations in India. It applies to public trusts, registered societies, Section 8 companies, universities, […]

July 21, 2026 By Steffy A

Section 201 of the Income Tax Act 2025: Tax Rate & Eligibility Introduction Section 201 of the Income Tax Act 2025 provides a concessional tax regime for eligible domestic manufacturing companies. It allows qualifying companies to pay income tax at […]