-

July 15, 2026

-

BySteffy A

Section 144 of the Income Tax Act 2025: SEZ Unit Deduction

Introduction

Section 144 of the Income Tax Act 2025 continues the deduction available to eligible Special Economic Zone units under Section 10AA of the Income-tax Act, 1961. It applies where an SEZ entrepreneur would have remained eligible for the deduction under Section 10AA had the earlier Act not been repealed. The deduction amount and the remaining eligible period continue to be determined according to Section 10AA.

In this blog, we will understand the applicability, eligibility conditions, and deduction framework under Section 144 of the Income Tax Act 2025.

What is Section 144 of the Income Tax Act, 2025?

Section 144 of the Income Tax Act 2025 continues the deduction available to eligible SEZ units under Section 10AA of the Income-tax Act, 1961. It allows an eligible SEZ entrepreneur to claim a deduction from export profits for the remaining tax years for which the benefit would have been available under Section 10AA had the earlier Act not been repealed.

The amount of deduction and the remaining eligible period are determined according to Section 10AA. Section 144 does not provide a fresh deduction period or restart the original 15-year benefit cycle.

Difference Between Section 10AA and Section 144

|

Basis |

Section 10AA |

Section 144 |

|

Effective law |

Income-tax Act, 1961 | Income-tax Act, 2025 |

| Provision | SEZ unit deduction provision |

Continuation provision for eligible deductions available under Section 10AA |

|

Applicable units |

Eligible SEZ units satisfying the conditions prescribed under Section 10AA | Eligible SEZ units continuing to satisfy the prescribed conditions |

| Deduction benefit | Deduction on eligible export profits of an SEZ undertaking |

Continuation of the deduction for the remaining eligible period |

|

Eligible activities |

Manufacturing or production of articles or things, or provision of services | Same eligible activities continue to be covered |

| Calculation method | Calculated using the export-profit formula prescribed under Section 10AA |

Deduction computation continues under the corresponding framework |

|

Benefit period |

Available for the eligible deduction period under Section 10AA |

Available only for the balance of the eligible deduction period |

Requirements for Claiming Section 144 Deduction

To claim deduction under Section 144 of the Income Tax Act 2025, the assessee must fulfill the eligibility conditions that were earlier applicable under Section 10AA of the Income Tax Act, 1961.

The conditions include:

- The entrepreneur should be covered under Section 2(j) of the Special Economic Zones Act, 2005.

- SEZ unit should have begun manufacturing, producing articles or things, or providing eligible services.

- Also, the SEZ unit should not be form ed by splitting up or reconstruction of an existing business.

- The undertaking should not be formed by transferring previously used machinery or plant to the new business, except to the extent permitted under the conditions and explanations applicable to Section 10AA.

A unit that has already exhausted the maximum deduction period available under Section 10A for the same undertaking cannot begin a fresh deduction period under Section 144.

Documents Required for Claiming Section 144 Deduction

Eligible SEZ units should maintain proper records to establish their eligibility, export turnover, business profits and deduction computation. Depending on the nature of the business and applicable requirements, the documents may include:

- SEZ Letter of Approval and other applicable SEZ approval or registration documents;

- SEZ approval and commencement documents;

- Export invoices;

- Export turnover records;

- Bank Realisation Certificates or other evidence of receipt of export proceeds.;

- Financial statements;

- Books of account relating to the eligible SEZ undertaking;

- Income-tax return;

- Prescribed audit or accountant’s report, where applicable;

- Special Economic Zone Re-investment Reserve Account details, where applicable; and

- Records showing the acquisition and use of new plant or machinery from the reserve amount.

The documents should clearly support the eligibility of the unit, the amount of export profits claimed and compliance with the applicable deduction conditions.

Deduction Calculation Under Section 144 of the Income Tax Act 2025

The deduction under Section 144 of the Income Tax Act 2025 is calculated using the same formula that was applicable under Section 10AA of the Income Tax Act, 1961.

Eligible export profit = Profits of the business of the SEZ undertaking × Export turnover of the SEZ undertaking ÷ Total turnover of the SEZ undertaking

The deduction is available only on profits derived from the export of eligible goods, articles, things, or services.

Deduction Period Under Section 144

Since the amount is calculated according to Section 10AA, the applicable deduction structure remains:

|

Eligible period |

Deduction |

|

First five consecutive years |

100% of eligible export profits |

| Next five consecutive years |

50% of eligible export profits |

|

Further five consecutive years |

Up to 50%, subject to transfer to and utilisation of the prescribed SEZ reserve |

However, under Section 144, an assessee can claim only the remaining portion of this period. It cannot restart the 15-year cycle.

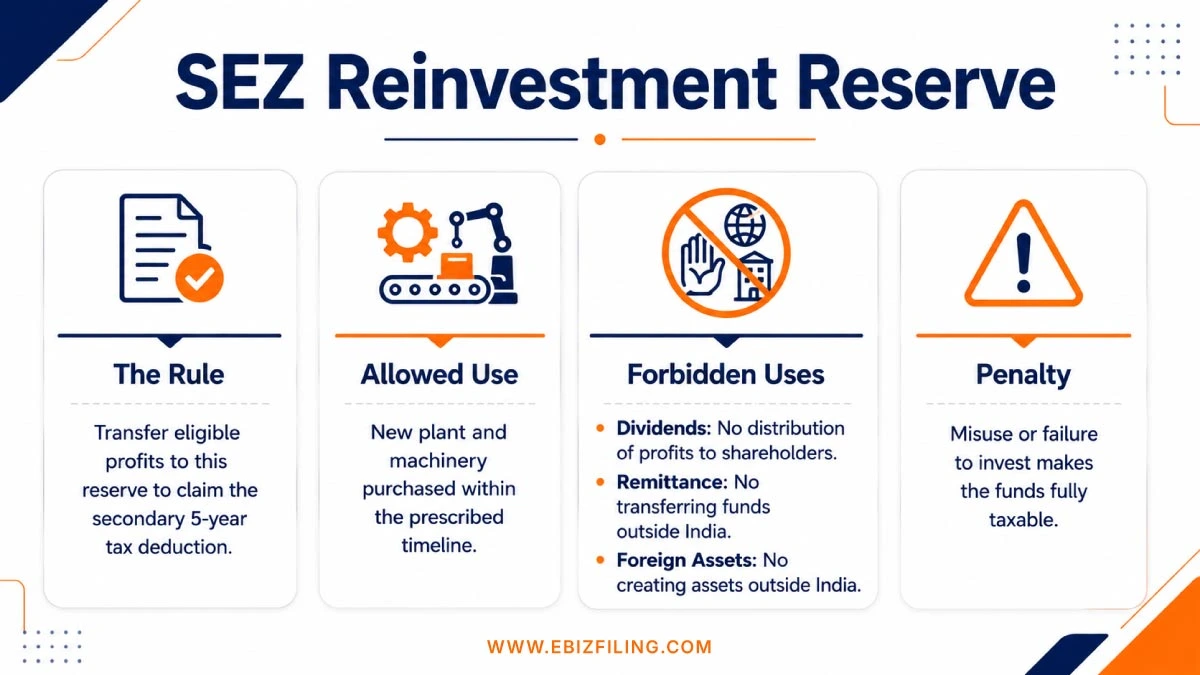

SEZ Reinvestment Reserve Account Under Section 144

To claim the reserve-linked deduction during the final five-year period, the eligible amount must be transferred to the Special Economic Zone Reinvestment Reserve Account. The deduction for this period is restricted to the lower of 50% of eligible export profits or the amount transferred to the reserve and utilised according to the prescribed conditions.

The amount credited to the reserve must be used for purchasing eligible new plant or machinery within three years. The relevant acquisition, withdrawal, and put-to-use details must be reported in Form 33, where applicable.

The amount cannot be used for:

- Distribution of dividends or profits

- Remittance of profits outside India

- Creation of assets outside India

Impact of Section 144 on Existing SEZ Units

The introduction of Section 144 under the Income Tax Act, 2025 continues the deduction benefit available to eligible SEZ units.

The provision ensures continuity of the earlier Section 10AA framework by:

- Continuing deduction on eligible export profits

- Maintaining the existing deduction computation method.

- Allowing deduction only for the remaining eligible tax years

Existing units should also review the key changes introduced under the Income Tax Act, 2025 to understand other renumbered provisions.

Section 144 in Case of Amalgamation or Demerger

The following treatment applies where an eligible undertaking is transferred under a qualifying amalgamation or demerger before the expiry of its deduction period:

- The benefits of Section 144 of the Income Tax Act 2025 cease to be available for an amalgamating or demerged company.

- The amalgamated or resulting company can continue to claim the deduction for the remaining eligible period as if the amalgamation or demerger had not taken place, subject to the prescribed conditions.

Ebizfiling Support for Section 144 Compliance

Ebizfiling helps SEZ units understand eligibility under Section 144, calculate eligible export profits, prepare tax documentation, and file Business Income Tax Returns while ensuring compliance with the Income Tax Act, 2025.

Our support includes:

- SEZ deduction eligibility review

- Export profit calculation assistance

- Income tax return filing support

- Tax documentation and compliance assistance

Ebizfiling can assist with eligibility review, export profit calculation, and Business Income Tax Return filing.

Conclusion

Section 144 of the Income Tax Act 2025 continues the deduction framework that was earlier available under Section 10AA of the Income-tax Act, 1961, ensuring uninterrupted tax benefits for eligible SEZ units. Eligible SEZ units should ensure that they satisfy the prescribed conditions, correctly compute export profits, maintain the required reserve where applicable, and comply with the provisions of the Income Tax Act, 2025 to continue to claim deduction under Section 144.

Frequently Asked Questions

1. What is the purpose of Section 144 of the Income Tax Act 2025 for SEZ units?

Section 144 of the Income Tax Act 2025 continues the deduction framework earlier available under Section 10AA of the Income Tax Act, 1961. It allows eligible SEZ units to claim a deduction on profits derived from the export of articles, things, or services for the remaining eligible period.

2. Who is eligible to claim deduction under Section 144 of the Income Tax Act 2025?

An entrepreneur covered under Section 2(j) of the Special Economic Zones Act, 2005 may claim the deduction only if the SEZ undertaking would have remained eligible under Section 10AA of the Income-tax Act, 1961. Merely holding an SEZ approval does not independently establish eligibility.

3. What are the eligibility conditions for claiming Section 144 SEZ deduction?

The undertaking must satisfy the conditions that applied under Section 10AA. Among other requirements, it should not be formed by splitting up or reconstructing an existing business or by transferring previously used plant or machinery, except to the extent permitted under the applicable statutory conditions.

4. How is the deduction under Section 144 of the Income Tax Act 2025 calculated?

The deduction is calculated by multiplying the profit of the SEZ unit by its export turnover and dividing the result by its total turnover. Only profits attributable to eligible export activities qualify for deduction.

5. Do eligible SEZ units need to submit a fresh application under Section 144?

Section 144 does not prescribe a fresh eligibility application merely because the governing law has changed. However, the assessee must continue to satisfy the Section 10AA conditions and furnish the applicable return, reports, and reserve-related particulars, including Form 33 where required.

6. Can a new SEZ unit claim the full 15-year deduction?

No. Section 144 of the Income Tax Act 2025 does not automatically grant a fresh 15-year deduction period. The benefit is available only for the remaining period that would have been available under Section 10AA.

7. Can a reconstructed SEZ unit claim deduction?

An SEZ unit formed by splitting up or reconstructing an existing business does not qualify, subject to the statutory exceptions and prescribed conditions.

8. What is the purpose of the SEZ Reinvestment Reserve Account under Section 144?

The SEZ Reinvestment Reserve Account is relevant to the deduction available during the further five-year period. The credited amount must be used to purchase eligible new plant or machinery within three years. The prescribed particulars must be furnished in Form 33 where applicable.

9. When can deduction claimed under Section 144 become taxable?

If the reserve is not utilised within the prescribed period, or is used for a prohibited purpose, the relevant amount may be treated as taxable business income in accordance with the Section 10AA framework. Tax treatment depends on the nature and timing of the non-compliance.

10. How can Ebizfiling help businesses with Section 144 compliance?

Ebizfiling helps eligible SEZ units review their remaining deduction period, calculate eligible export profits, prepare supporting records, file the applicable income-tax return, and comply with Form 33 and reserve-related requirements.

Maximize Your Tax Benefits

Ensure accurate Income Tax Return filing while claiming eligible deductions with expert assistance.

About Ebizfiling -

July 15, 2026 By Steffy A

Company Compliance Calendar August 2026: Key Due Dates Introduction The Company Compliance Calendar August 2026 provides a complete overview of important corporate compliances that companies should monitor during the month under the Companies Act, 2013. In this blog, you will […]

July 13, 2026 By Steffy A

Form 79 under the Income Tax Act 2025: Investment Fund Filing Guide Overview Form 79 under the Income Tax Act is a statement used by investment funds to report income paid or credited to unit holders. It is furnished under […]

July 10, 2026 By Steffy A

Form 130 under the Income Tax Act for Salary TDS Certificate Introduction Form 130 under the Income Tax Act is the new TDS certificate for salary, pension, and specified senior citizen interest income. It replaces Form 16 from Tax Year […]