-

July 18, 2026

-

BySteffy A

Section 111A and 112A of the Income Tax Act: STCG and LTCG Tax Rules

Introduction

Section 111A and Section 112A of the Income-tax Act, 1961 governed the taxation of eligible short-term and long-term capital gains arising from equity shares, equity-oriented mutual funds, and units of business trusts. Section 111A applied to eligible short-term capital gains, while Section 112A applied to eligible long-term capital gains.

From 1 April 2026, the corresponding provisions are contained in Section 196 and Section 198 of the Income-tax Act, 2025. Sections 111A and 112A remain relevant for transactions, returns, assessments, and other matters governed by the Income-tax Act, 1961.

This article explains the earlier provisions under Sections 111A and 112A and their corresponding treatment under Sections 196 and 198 of the Income-tax Act, 2025.

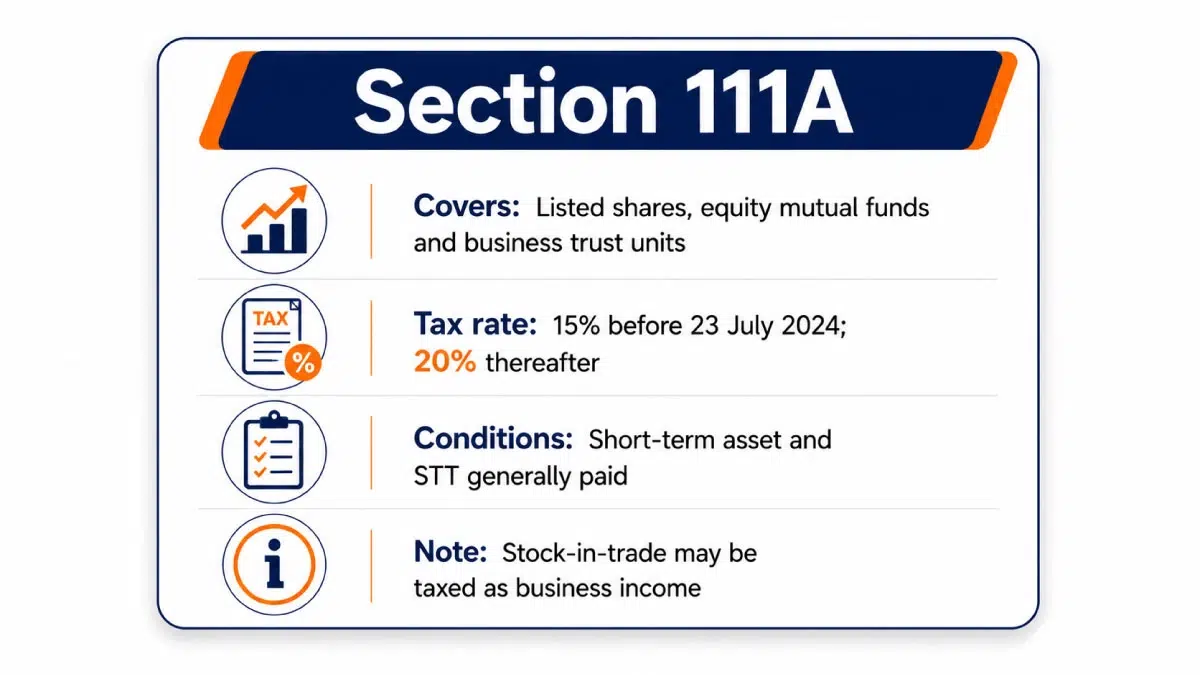

What is Section 111A of the Income Tax Act?

Section 111A of the Income Tax Act provides a concessional tax rate on eligible short-term capital gains arising from the transfer of specified equity securities. It generally covers listed equity shares, units of an equity-oriented mutual fund, and units of a business trust where the prescribed STT conditions are satisfied.

For eligible transfers made on or after 23 July 2024, short-term capital gains under Section 111A are generally taxable at 20%. The earlier rate of 15% generally applied where the transfer took place before 23 July 2024. Applicable surcharge and health and education cess are charged separately.

The security must generally be held as a capital asset. If shares or securities are held as stock-in-trade, the resulting income may be treated as business income instead of capital gains.

Assets Covered under Section 111A

Section 111A generally applies to short-term capital gains arising from the transfer of:

- Listed equity shares in a company

- Units of an equity-oriented mutual fund

- Units of a business trust

- The prescribed holding period and STT conditions must also be satisfied.

Section 111A Tax Rate

|

Date of transfer |

Tax rate |

|

Before 23 July 2024 |

15% |

| On or after 23 July 2024 |

20% |

Note: For gains governed by the Income-tax Act, 2025 from 1 April 2026, refer to the corresponding provisions of Section 196.

Conditions for Taxation under Section 111A

To claim taxation under Section 111A, the following conditions must generally be satisfied:

- The gain must arise from the transfer of an eligible equity share, equity-oriented mutual-fund unit, or business-trust unit.

- Also, the asset must qualify as a short-term capital asset.

- The security should be held as a capital asset and not as a stock-in-trade.

- STT should generally have been paid on the transfer.

- The transaction must satisfy the other prescribed conditions under the Income-tax Act.

Certin transactions undertaken on a recognised stock exchange located in an International Financial Services Centre may receive specified treatment even where STT is not paid, subject to the prescribed conditions.

Basic Exemption Limit and Section 111A

A resident individual or HUF may generally adjust the unutilised basic exemption limit against eligible short-term capital gains covered under Section 111A, subject to the applicable provisions.

After the adjustment, the remaining eligible short-term capital gain is taxed at the applicable special rate.

The availability of rebate must be checked separately according to the relevant tax year, applicable tax regime, and governing legislation. For periods governed by the Income-tax Act, 1961, the relevant rebate provision is Section 87A. For Tax Year 2026-27 onward under the Income-tax Act, 2025, the corresponding rebate provision is Section 156.

Taxpayers should not assume that the entire tax payable on special-rate capital gains will automatically qualify for rebate.

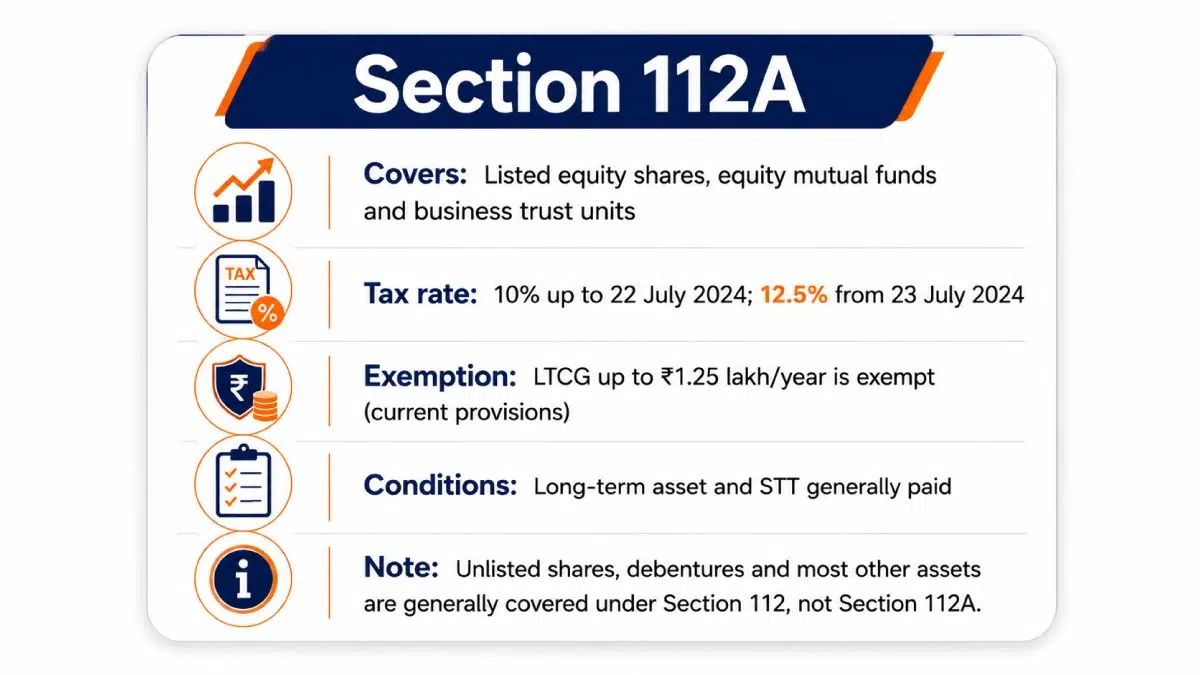

What is Section 112A of the Income Tax Act?

Section 112A provides a concessional tax rate on eligible long-term capital gains arising from specified equity-related assets. It generally applies to listed equity shares, units of an equity-oriented mutual fund, and units of a business trust where the prescribed STT conditions are satisfied.

For eligible transfers made on or after 23 July 2024, aggregate long-term capital gains exceeding ₹1.25 lakh during the financial year are generally taxable at 12.5%. For transfers made before 23 July 2024, the applicable rate was generally 10%. However, for FY 2024-25, the amended aggregate annual threshold of ₹1.25 lakh applies to total gains covered under Section 112A, including transfers made before and after.

Section 112A applies only to specified equity-related assets. Unlisted shares, debentures, and other capital assets are generally governed by Section 112 or another applicable provision.

How Is Section 112 Different from Section 112A?

Section 112 generally covers long-term capital gains arising from assets that are not specifically covered under Section 112A, such as certain unlisted shares, immovable property, debentures, and other capital assets. Section 112A specifically covers eligible long-term capital gains from listed equity shares, equity-oriented mutual funds, and units of business trusts where the prescribed STT conditions are satisfied.

Assets Covered under Section 112A

Section 112A generally covers long-term capital gains arising from:

- Listed equity shares in a company

- Units of an equity-oriented mutual fund

- Units of a business trust

The Income Tax Department’s Schedule 112A reporting guidance also identifies these assets for reporting long-term capital gains where STT has been paid.

You can also read our guide on Income Tax Rules for Equity Share Trading to understand how investment, delivery-based trading, and business income from shares may be taxed.

Section 112A Tax Rate and Aggregate Threshold

|

Applicable period |

Tax rate |

Aggregate annual threshold |

|

Financial years before FY 2024-25 |

10% | ₹1 lakh |

| FY 2024-25: transfers before 23 July 2024 | 10% |

₹1.25 lakh for aggregate Section 112A gains |

|

FY 2024-25: transfers on or after 23 July 2024 |

12.5% | ₹1.25 lakh for aggregate Section 112A gains |

| FY 2025-26 under the Income-tax Act, 1961 | 12.5% |

₹1.25 lakh |

|

Tax Year 2026-27 onward under Section 198 |

12.5% |

₹1.25 lakh |

The ₹1.25 lakh exemption is an aggregate annual threshold and not a separate exemption for every transaction.

Applicable surcharge and health and education cess are charged separately.

Conditions for Taxation under Section 112A

The following conditions generally apply:

- The asset must be a listed equity share, equity-oriented mutual-fund unit, or business-trust unit.

- The asset must qualify as a long-term capital asset.

- STT should generally be paid on the transfer.

- In the case of equity shares, STT should generally have been paid on acquisition and transfer, subject to notified exceptions.

- The capital gain must be reported in the applicable ITR schedules.

- Chapter VI-A deductions cannot generally be claimed directly against income taxable at the special rate under Section 112A.

The availability of a rebate under Section 87A against tax payable on Section 112A gains depends on the relevant tax year, tax regime, and applicable statutory position.

Holding Period for Section 111A and 112A

Listed equity shares, equity-oriented mutual-fund units, and specified listed business-trust units are generally treated as short-term capital assets when held for 12 months or less.

They are generally treated as long-term capital assets when held for more than 12 months.

The applicable holding period should be checked according to the asset type and relevant legal provisions.

Difference Between Section 111A and 112A

|

Basis |

Section 111A |

Section 112A |

|

Nature of gain |

Short-term capital gain | Long-term capital gain |

| Eligible assets | Specified equity shares, equity-oriented fund units, and business-trust units |

Specified equity shares, equity-oriented fund units, and business-trust units |

|

General holding period |

12 months or less | More than 12 months |

| Rate before 23 July 2024 | 15% |

10% |

|

Rate from 23 July 2024 |

20% | 12.5% |

| Separate exemption threshold | No separate annual threshold |

Aggregate annual threshold of ₹1.25 lakh for qualifying LTCG |

|

STT condition |

Generally required on transfer | Generally required as prescribed on acquisition and transfer |

| Loss treatment | Short-term capital loss may generally be adjusted against eligible STCG or LTCG |

Long-term capital loss may generally be adjusted only against LTCG |

|

ITR reporting |

Schedule Capital Gains | Schedule Capital Gains and Schedule 112A, where applicable |

| Provision under the Income-tax Act, 2025 | Section 196 |

Section 198 |

Read our detailed guide on Short-Term Capital Gain Tax (STCG) and Long-Term Capital Gain Tax on Shares to understand the applicable tax rates, holding periods, exemptions, and reporting requirements.

Example of Tax Calculation under Section 111A

Suppose a taxpayer earns an eligible short-term capital gain of ₹2,00,000 from listed equity shares transferred after 23 July 2024.

Calculation:

₹2,00,000 × 20% = ₹40,000

The base tax under Section 111A would be ₹40,000. Applicable surcharge and cess would be charged separately.

Example of Tax Calculation under Section 112A

Suppose a taxpayer earns eligible long-term capital gains of ₹3,00,000 during the financial year.

Calculation:

- Total LTCG: ₹3,00,000

- Less: Exemption limit: ₹1,25,000

- Taxable LTCG: ₹1,75,000

- Tax at 12.5%: ₹21,875

The base tax under Section 112A would be ₹21,875. Applicable surcharge and cess would be charged separately.

These are simplified examples and do not consider adjustments against the basic exemption limit, loss set-off, rebate, surcharge, cess, or other income.

Read our detailed guide on Capital Gains Tax to understand the tax treatment of short-term and long-term capital gains, applicable rates, exemptions, and reporting requirements.

Need Expert Assistance with Capital Gains ITR Filing?

Capital gains from equity shares, mutual funds, and other securities require accurate classification, tax computation, and reporting in the appropriate ITR schedules.

Ebizfiling provides Income Tax Return Filing support for individuals and businesses earning capital gains incomecapital gains capital gains . Our experts can assist with reviewing transaction statements, classifying short-term and long-term gains, computing the applicable tax liability, and reporting the details in the relevant ITR schedules.

Ebizfiling can assist you with:

- Income Tax Return Filing

- Capital gains computation support

- Review of broker and mutual-fund statements

- Income Tax Notice Assistance

- Tax consultation and compliance support

Get professional assistance from Ebizfiling for accurate capital gains reporting and Income Tax Return Filing.

Conclusion

Section 111A and 112A play an important role in determining the tax liability on eligible short-term and long-term capital gains arising from specified equity-related securities. Under the Income-tax Act, 2025, these provisions are renumbered as Section 196 and Section 198, respectively. Taxpayers should carefully verify the asset type, holding period, STT conditions, applicable tax rate, exemption threshold, and ITR reporting requirements before filing their return.

Frequently Asked Questions

1. Can Section 111A and 112A apply to the same taxpayer in one financial year?

A taxpayer may earn both eligible short-term and long-term capital gains during the same financial year. Short-term gains may be taxed under Section 111A, while qualifying long-term gains may be taxed under Section 112A, subject to the applicable conditions.

2. Does switching between equity mutual fund schemes attract tax under Section 111A or Section 112A?

A switch from one mutual-fund scheme to another is generally treated as a redemption from the existing scheme and a new investment in the other scheme. The resulting gain may fall under Section 111A or Section 112A depending on the holding period and prescribed conditions.

3. How are bonus shares and rights shares taxed under Section 111A and 112A?

The sale of bonus shares and rights shares may be covered under Sections 111A or 112A where the shares qualify as eligible securities and the applicable holding-period and STT conditions are satisfied. Their cost of acquisition and holding period must be calculated according to the relevant provisions.

4. How are SIP investments taxed under Section 111A and 112A?

Each SIP instalment is treated as a separate investment for capital gains purposes. The holding period and gain must therefore be calculated separately for each instalment or unit redeemed.

5. What is the current tax rate under Section 111A of the Income Tax Act?

For eligible transfers made on or after 23 July 2024, short-term capital gains covered under Section 111A are generally taxed at 20%. The earlier rate of 15% generally applied to transfers completed before that date.

6. What is the current exemption limit under Section 112A?

The aggregate annual threshold for qualifying long-term capital gains is ₹1.25 lakh. For Tax Year 2026-27 onward, the corresponding provision is Section 198 of the Income-tax Act, 2025.

7. Can NRIs be taxed under Section 111A and 112A?

NRIs may be covered subject to their residential status, the nature and location of the asset, STT conditions, applicable non-resident provisions, and any relief available under the relevant DTAA.

8. Can short-term capital losses be set off against gains taxable under Section 112A?

A short-term capital loss may generally be adjusted against eligible short-term or long-term capital gains. However, a long-term capital loss may generally be adjusted only against long-term capital gains.

9. Which documents should be maintained for Section 111A and 112A transactions?

Taxpayers should maintain broker contract notes, demat statements, mutual-fund statements, purchase records, sale records, and capital gains reports. These documents help support the transactions reported in the Income Tax Return.

10. How can Ebizfiling help with Section 111A and 112A capital gains reporting?

Ebizfiling can assist taxpayers with reviewing investment statements, classifying short-term and long-term gains, applying the relevant tax rates, calculating tax liability, and reporting capital gains in the appropriate Income Tax Return schedules.

ITR filing

Filing of Income Tax return is necessary if you have earned any income. File your ITR with EbizFiling

About Ebizfiling -

Reviews

Nisha Swaroop

11 Oct 2019It was fantastic working with EbizFiling. They are friendly and supportive. Everything done smoothly and on timely basis. I would love to work with them again.

Ratnesh Mishra

19 Nov 2021Awesome work done by this team especially Ms Aishwarya and Mr Deepak....They followed everything on time and service cost was very competitive... Looking forward working with these awesome guys👏👏👏😍

DEEPAK BAGRA

08 Sep 2018I find the service, working approach and commitments very professional. Their progress updates are commendable. I really liked working with them.

July 18, 2026 By Steffy A

Section 196 and 198 of the Income Tax Act 2025: STCG and LTCG Introduction Sections 196 and 198 of the Income-tax Act, 2025 prescribe special tax rates for eligible short-term and long-term capital gains arising from specified equity-related assets. Section […]

July 18, 2026 By Steffy A

The concept of Form 168 of Income Tax Act Explained The Form 168 of Income Tax Act is the Annual Information Statement prescribed under the Income-tax Rules, 2026. It provides taxpayers with a consolidated view of TDS, TCS, tax payments, […]

July 17, 2026 By Steffy A

TDS and TCS Compliance Calendar August 2026: Key Due Dates Introduction The TDS and TCS Compliance Calendar August 2026 highlights all the important due dates for depositing tax deducted or collected in July 2026, issuing TDS certificates, and completing statutory […]