-

July 23, 2026

-

BySteffy A

Confused About ITR Forms? A Simple Guide for AY 2026-27

Why Choosing the Right ITR forms Matters?

Filing ITR forms is confusing, especially when you are not sure about which one is right for you. As per recent filing trends choosing the right ITR form helps avoid delays or notices from the Income Tax Department. For the year 2026-27, updated rules have made correct selection even more important. In this article, we will explain different ITR forms in a simple, easy and practical way.

Classification of ITR form

Income Tax Return (ITR) is a report that is submitted to the taxation authority detailing the income earned by a taxpayer and the tax owed. The Income Tax Department has developed eight various forms of ITR, each being applicable to a particular group of taxpayers. The form to be used depends on such aspects as the type of income, the total earnings, and the type of filer, be it an individual, Hindu Undivided Family (HUF), or a company.

To meet the tax requirements, taxpayers should submit their ITRs before the deadline and within the period. Correctly filling in the needed ITR forms implies proper taxpaying, avoiding legal fines, and enhancing financial transparency.

In the case of filing income tax returns in India, one of the most baffling things to the tax payers is the identification of the required ITRs. The Income Tax Department has added numerous forms of ITRs based on the nature of the person, source of income and complexity of finances. When you file the incorrect form, you might end up causing complications, delays or even rejection of your return.

All the ITR forms are formulated to a certain category. Salaried employees, such as those in the case of ITR-1, often use ITR-1, whereas capital gains might need ITR-2. Likewise, there are numerous forms that are used by business owners and professionals, including ITR-3 and ITR-4. These types of categorization can make you file your return correctly and prevent compliance problems.

For more clarity, below is a quick reference table of all ITR form :

|

ITR forms |

Applicable To |

Income Limit |

Type of Income Allowed |

Not Applicable For |

| Individuals | Up to ₹50 lakh |

Salary, 1 house property, interest income |

Capital gains, business income, foreign assets | |

| Individuals, HUFs | No limit |

Capital gains, multiple house properties, foreign income |

Business or professional income | |

| Individuals, HUFs | No limit |

Business or professional income |

Not for those without business income | |

| Individuals, HUFs, Firms (except LLP) | Up to ₹50 lakh |

Presumptive income (44AD, 44ADA, 44AE) |

Foreign income, LLPs, capital gains (some cases) | |

| Firms, LLPs, AOP, BOI | No limit |

Business and other income |

Individuals and companies | |

| Companies | No limit |

All income except exempt u/s 11 |

Charitable/religious trusts | |

| Trusts, NGOs, Institutions | No limit |

Income under sections 139(4A–4F) |

Regular taxpayers | |

| Individuals, HUFs, Firms, Companies | No specific limit |

To update previously filed or missed returns |

Cannot be used to claim a refund or reduce tax liability |

How to File ITR forms?

The process of filling in your income tax return (ITR) involves a few simple steps and understanding the key can lead to proper reporting and prevent problems in future.

- Find the right ITR forms : Choose the appropriate ITR forms, which depend on your income sources, including salary, business, or capital gains.

- Calculate your income and taxes : Calculate your total income out of all sources and your tax payable after deductions.

- Access the Income Tax Portal : Log in to the official portal of income tax e-filing and fill in your PAN.

- Complete and Submit the form : Complete and verify all the information that is needed and then online your ITR forms.

- Confirm your return : Once your return is submitted, confirm your return with Aadhaar OTP, net banking or by mailing a signed ITR-V to CPC.

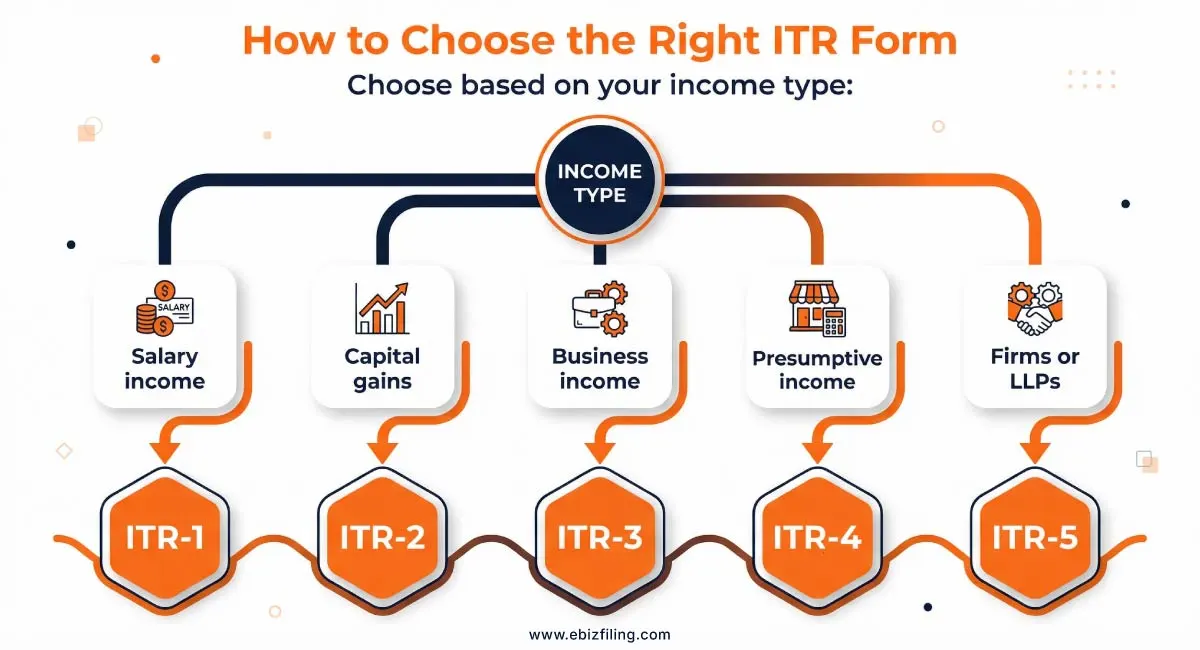

Select the Right ITR forms

Choosing the right form of ITR is a crucial step of the tax filing process. It is a common mistake among taxpayers to choose a form that fits conveniently instead of the form that they qualify to file, and this can result in mistakes and warnings or even rejection of a return. You need to understand your revenue and financial activities of the year first before presuming. When a choice of which form to take is clear, then it is much easier to make a selection.

Here’s an easy method to decide:

- If you earn only salary and basic interest income

You can file ITR-1 (Sahaj). This form is suitable for salaried individuals with income up to ₹50 lakh, having income from one house property and other sources like interest. It is the simplest form but comes with strict eligibility conditions. - If you have investments or capital gains

You should use ITR-2. This applies if you earn from the sale of shares, mutual funds, property, or have multiple house properties. It is also required if you have foreign income or assets. - If you run a business or are involved in trading

You must file ITR-3. This includes business owners, professionals, freelancers, and individuals involved in stock trading such as futures and options. This form captures detailed business income and expenses. - If you opt for presumptive taxation

You can file ITR-4 (Sugam). This is suitable for small businesses and professionals who declare income under Sections 44AD, 44ADA, or 44AE. However, this form is only valid if your income is within specified limits and you do not have complex income sources. - If you are a firm or LLP

You need to file ITR-5. This form is meant for partnership firms, LLPs, and other similar entities, and not for individual taxpayers.

When you are doubtful about your eligibility, it is always better to use a more complete form over a simpler one. Filing a somewhat more complex form is better to selecting the wrong one and then facing compliance issues.

Real Case Example

A salaried employee earning ₹18 lakh filed ITR-1 but also had mutual fund gains. Since capital gains are not allowed in ITR-1, the return was flagged.

The taxpayer had to revise the return using ITR-2, which delayed the refund and increased compliance work.

Thus , always match your income type with the correct ITR form.

How Ebizfiling Helps You Choose the Right ITR forms?

Ebizfiling simplifies the process of choosing the appropriate ITR forms by directing you based on your income and eligibility.

- Ebizfiling assists you in selecting the relevant ITR forms based on your income type, decreasing the possibility of rejection.

- We help in translate complex ITR forms facts into simple English so you can easily comprehend your eligibility.

- Our professionals will walk you through the filing procedure to ensure accuracy and compliance with tax requirements.

- We reduce errors by carefully evaluating your information and picking the suitable form.

- Ebizfiling saves you time by handling the technical issues while keeping you stress-free.

Suggested Read :

A Simple guide on Major Income tax forms Renumbered

ITR Filing Online vs Tax Consultant

ITR-3 Form Filing AY 2026-27: Process and Eligibility

Final Thoughts

To be able to file taxes successfully, one should choose the appropriate form of ITR. Even minor errors during selection of the form can result in the delays or notices of the Income Tax Department. Before you turn in your return, always think of investigating your sources of revenue. When you are in doubt, it is a good idea to have professional assistance, and that would make the process painless and error-free.

Frequently Asked Questions

1. Who is eligible to be presumed to be a taxation system when filling in ITR-4?

Any individual, Hindu Undivided Family (HUF) and partnership firm (except LLP) may choose to follow the presumed-to-be a taxation scheme under Section 44AD, 44ADA or 44AE. This plan is primarily designed to suit small businesses and those who have a gross income of up to 50 lakh. It enables taxpayers to declare income at a constant percentage without keeping detailed books of accounts, and tax filing is easier and quicker.

2. What would be my ITR in case I have capital gains?

You must complete ITR-2 in case you have an income to capital gains like the sale of shares, mutual funds, or property. The form is particularly targeted at those individuals and HUFs whose income is not based on business income but rather on capital gains. Even when you have a personal income lower than 50 lakh, it is not allowed to file ITR-1.

3. What is the difference between ITR-1 and ITR-2?

ITR-1 is to individuals, whose sources of income are straight forward, i.e. the salary, property (one house) and interest income not more than 50 lakh. ITR 2, on the other hand, is used in case of the income which is more complex such as the capital gains, multiple houses or foreign income. The main difference is the nature and sophistication of the income that is reported in each form.

4. Which ITR form(s) is to be completed by a salaried employee(s)?

Most of the salaried workers can submit ITR-1 (Sahaj) as long as they do not earn more than ₹50 lakh and it is a mix of salary, house property and interest. However, when a salaried individual has other income like capital gains or foreign assets, he or she will be required to file ITR-2 instead.

5. What are the forms of income that is ineligible in ITR-1?

Capital gains, company or profession income, multiple residential properties, international income, or agricultural income above ₹5,000 cannot be claimed under ITR-1. In this case, you will need to choose another ITR forms, i.e., ITR-2 or ITR-3, according to your income level.

6. Does ITR-1 have any changes in the house property schedule?

Yes, recent updates have enhanced the reporting under house property to be more detailed. Taxpayers are now likely to be expected to include more details in their tax returns including details about tenants or the interest elements of loans in a more straightforward manner. These reforms will enhance transparency and proper reporting of house property income.

7. Will it be possible to prepare ITRs in the past four annual years now?

No, you are not usually free to prepare returns of the previous four assessment years. The Income Tax Department however permits filing a revised return (ITR-U) within a given period which is normally not more than 2 years after the completion of the appropriate assessment year. Ebizfiling facilitates employee to make corrections on missed filings or to report more income.

8. What are the other Chapter VI-A deductions which is necessary in the ITR-1 of a year 2025-26?

Taxpayers may need to disclose in more detail in AY 2025-26 to claim deductions in Chapter VI-A, such as in Sections 80C, 80D and 80G. This includes specification of nature of investments or expenses claimed. This will result in better verification and reduce claims of false deductions.

9. What Kind of ITR can be used in the case of Non-Residents?

ITR-2 is usually filed by non-residents who do not have a business income, and ITR-3 by those who have a business income or professional income in India. The decision will be based on the type of income generated in India. Non-residents should report the foreign assets properly and any foreign income, where it exists.

10. What can Ebizfiling do to assist in choosing the appropriate ITR forms AY 2026-27?

The right ITR forms AY 2026-27 may be somewhat confusing, particularly when you have more than one source of income. Ebizfiling will assist you in profile analysis of your income and will also help you in choosing the right ITR forms so as to avoid mistakes or rejection. Their professionals will make sure that everything is properly reported and recorded according to the most recent.

Tax Consultancy Services

Simplify Taxes, Maximize Savings

About Ebizfiling -

July 23, 2026 By Steffy A

Section 202 of the Income Tax Act, 2025: Tax Slabs and Rules Introduction Section 202 of the Income Tax Act 2025 contains the provisions governing the new tax regime for individuals, Hindu Undivided Families, Associations of Persons, Bodies of Individuals, […]

July 22, 2026 By Steffy A

Section 332 of the Income Tax Act 2025: NPO Registration Introduction Section 332 of the Income Tax Act 2025 provides the registration framework for eligible non-profit organizations in India. It applies to public trusts, registered societies, Section 8 companies, universities, […]

July 21, 2026 By Steffy A

Section 201 of the Income Tax Act 2025: Tax Rate & Eligibility Introduction Section 201 of the Income Tax Act 2025 provides a concessional tax regime for eligible domestic manufacturing companies. It allows qualifying companies to pay income tax at […]