-

June 24, 2026

-

BySteffy A

TDS and TCS new changes from April 1st 2026

Introduction to TDS and TCS New Changes

The Income Tax Act 2025 introduces major TDS and TCS new changes effective from April 1, 2026, restructured the entire tax deduction system in India. With amended section numbers, updated forms, and simplified TDS and TCS rates, the new framework aims to make compliance more structured clear and simpler.

And these TDS and TCS new changes also clear up uncertainties in areas not addressed under the Income Tax Act. Knowing these changes will help you to handle tax collected at source and deductions in a better way, to keep your business away from risks and non-compliance.

TDS and TCS Forms Have Changed: What You Need to Use Now

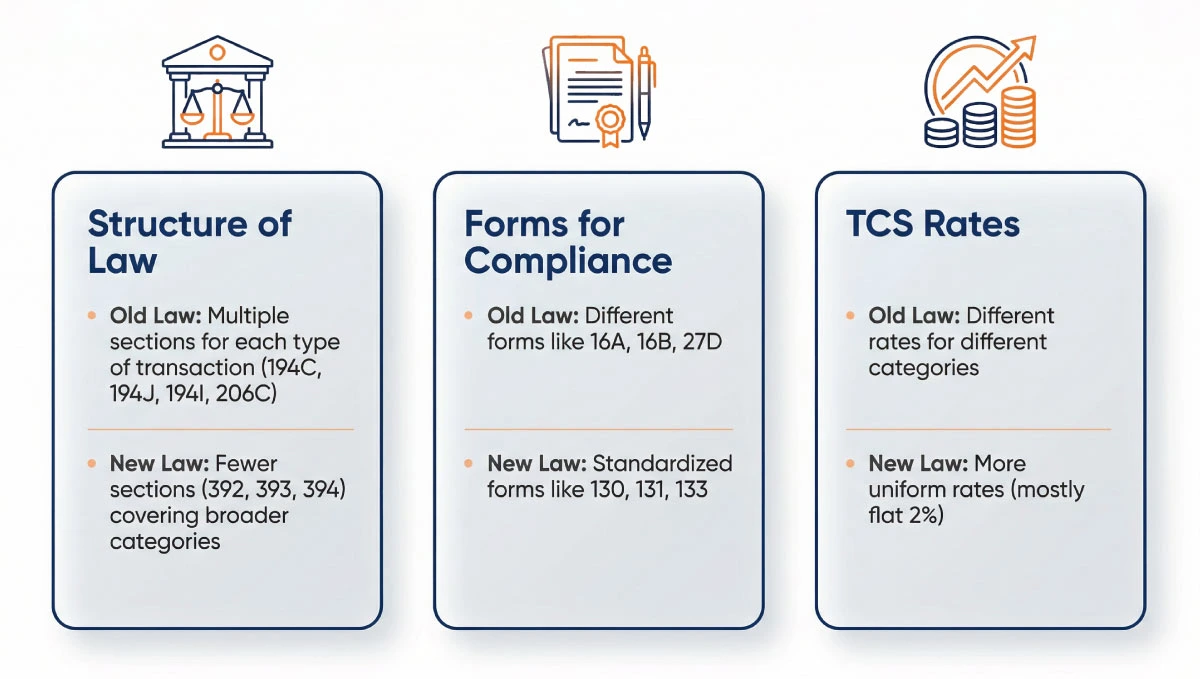

From 1 April 2026, TDS and TCS new changes under the Income Tax Act 2025 have made compliance simpler and more organized. Previously, multiple forms like 16A, 16B, and 27D created confusion in the tax deduction system. Now, there are uniform TDS and TCS forms like 130, 131, 132 and 133 which makes filing TDS and TCS easier.

For instance, Form 131 can be used for most non-salary TDS, whereas Form 133 can be used for Tax Collected at Source. These TDS and TCS new changes reduce complexity, enhance clarity and assist businesses to file without mistakes.

Major changes applicable from 1st April 2026

Understand the major TDS and TCS new changes applicable from April 1st 2026 for better compliance.

How TDS and TCS Changes in 2026 Affect Your Business

TDS and TCS new changes under the Income Tax Act 2025 will remarkably impact businesses and professionals from April 1, 2026. Updated sections, forms, and TDS and TCS new rates need system upgrades and process changes. While initial adjustments may create confusion, these TDS and TCS reforms simplify the tax deduction system and improve compliance efficiency in the long run.

TDS and TCS changes: Old vs New Income Tax Act 2025 Comparison Table

| Category | Old Section | New Section | Old Form | New Form | Threshold (Old / New) | Old Rate | New Rate |

| Contract Payments | Section 194C | Section 392 | Form 16 (Annual Certificate) | Form 130 (Annual Certificate) | ₹30,000 single payment / ₹1,00,000 aggregate (same in new law) | 1% (Individual/HUF), 2% (Others) | 1% (Individual /HUF), 2% (Others) |

| Professional/Technical Services | Section 194J | Section 393 | Form 16A (Non-Salary) | Form 131 (Non-Salary) | ₹30,000 per financial year (same in new law) | 10% | 10% |

| Rent Payments | Section 194I | Section 394 | Form 16A (Non-Salary) | Form 131 (Non-Salary) | ₹2,40,000 per financial year (same in new law) | 10% (or 2% for land/plant as applicable) | 10% (or 2% for land/plant as applicable) |

| Manpower Supply Services | Not explicitly covered under 194C | Section 392 (explicitly included) | Form 16A (Non-Salary) | Form 131 (Non-Salary) | ₹30,000 single payment / ₹1,00,000 aggregate | Not applicable | 1% (Individual/HUF), 2% (Others) |

| NRI Property Purchase | Section 194IA | Section 392 (PAN-based) | Form 16B (Property TDS) | Form 132 (Property TDS – PAN-based) | ₹50 lakh property value (same in new law) | 1% (without PAN: 20%) | 1% (PAN-based, no TAN needed) |

| Return Forms (All TDS) | Form 24Q / 26Q / 27Q | Form 138 / 140 / 139 | Form 24Q / 26Q / 27Q | Form 138 / 140 / 139 | Not threshold based | Varied | Varied |

| Alcoholic Liquor (TCS) | Section 206C(1) | Section 394 (TCS) | Form 27D (TCS Certificate) | Form 133 (TCS Certificate) | No threshold – applicable from first sale/receipt | 1% | 2% (Flat) |

| Scrap (TCS) | Section 206C(1) | Section 394 (TCS) | Form 27D (TCS Certificate) | Form 133 (TCS Certificate) | No threshold – applicable from first sale/receipt | 1% | 2% (Flat) |

| Coal / Lignite / Iron Ore (TCS) | Section 206C(1) | Section 394 (TCS) | Form 27D (TCS Certificate) | Form 133 (TCS Certificate) | No threshold – applicable from first sale/receipt | 1% | 2% (Flat) |

| Tendu Leaves (TCS) | Section 206C(1) | Section 394 (TCS) | Form 27D (TCS Certificate) | Form 133 (TCS Certificate) | No threshold – applicable from first sale/receipt | 5% | 2% (Flat) |

| LRS – Education & Medical (TCS) | Section 206C(1G) | Section 394 (TCS) | Form 27D (TCS Certificate) | Form 133 (TCS Certificate) | Above ₹10 lakh (as per your table; same in new law) | 5% (above ₹10L) | 2% (Flat) |

| Overseas Tour Packages (TCS) | Section 206C(1H) | Section 394 (TCS) | Form 27D (TCS Certificate) | Form 133 (TCS Certificate) | No threshold / applies on the package amount | 5% (up to ₹10L), 20% (above ₹10L) | 2% (Flat) |

TDS and TCS new changes Penalties: What It Can Cost You

- TDS and TCS new changes (effective 1 April 2026) can be costly.

- If TDS is not deducted, interest is 1% per month.

- If deducted but not deposited, interest is 1.5% per month.

- Failure to file returns attracts ₹200 per day penalty.

- According to the Income Tax Act 2025, non-compliance with TDS can disallow expenses, leading to higher tax payments.

- Failure to adhere to the tax deduction system and TCS may also invite reassessment or fines.

Let Ebizfiling Handle Your Tax Compliance

The TDS and TCS new changes under the Income Tax Act 2025 give a more streamlined tax deduction system that makes TDS and TCS compliance simpler and minimizes errors in the future.

Ebizfiling can help you to deal with these TDS and TCS new changes with its expertise in TDS return filing, compliance and notice management to ensure compliance and save you from penalties and fines; so you can focus on your business.

Suggested Reads:

Income Tax Rules 2026

Professional Tax notice: Explained

Income Tax Clearance certificate: Explained

Section 194N: TDS on Cash Withdrawal Rules & Limits

Final Thoughts

In short, the TDS and TCS new changes is applicable from April 1, 2026, will make the process simpler and more efficient. It plays an important part for businesses to know about changes in sections, forms and dates of TDS payment to avoid harsh penalties.

Also, early preparation helps in smooth functioning and effective tax planning. Finally, staying ahead of the curve not only minimizes risks, but also ensures the efficiency and integrity of the tax deduction system.

Frequently Asked Questions

1. What are the new TDS and TCS rates that are applicable from April 2026?

From April 2026, there are fewer rates for TCS, with some falling under a flat 2% rate. TDS rates remain generally unchanged, but are simplified making it less confusing for taxpayers to apply the correct rates.

2. How to file TDS return online in 2026?

TDS return filing is required online, in the new forms and changed sections under the new law. This includes entering, validating, and filing data on the income tax portal with adherence to deadlines to avoid penalties.

3. How can Ebizfiling help with TDS and TCS new changes compliance?

Ebizfiling assists companies to comply with the TDS and TCS new changes by managing proper deductions, timely filing of returns, and the new forms. It provides professional assistance and ongoing compliance monitoring to ensure you don’t incur penalties and are in line with the new tax rules.

4. What is the due date for TDS and TCS new changes return filing?

Normally TDS and TCS returns are filed quarterly with due dates for each quarter. Filing on time is crucial as late filing attracts interest and penalty, and can also impact the tax credit to taxpayers.

5. What happens if TDS is not deducted or deposited?

The non-deduction and non-deposit of TDS attracts interest and penalties, and may also result in dis-allowance of expenses at the time of tax computation. This also means higher tax liability, and possibly notices or scrutiny from the tax authorities.

6. What are TDS and TCS new changes forms introduced?

The new legislation has standardized forms, like 130, 131, 132 and 133, in place of multiple forms. This helps to avoid confusion with multiple forms, and implies uniform, clear and effective TDS and TCS compliances.

7. Is TAN required under the TDS and TCS new changes system?

TAN is still used for most TDS compliances, but some transactions, such as real estate transactions, now emphasize more on PAN-based systems. This simplifies things for individuals, but companies still need to keep their TANs updated for regular filing.

8. How to avoid penalties in TDS and TCS new changes compliance?

No penalties will be levied if a business is timely in deducting at the correct rate, keeping records and filing returns. The help of a professional, like Ebizfiling, can help stay compliant and avoid errors or omissions.

9. Who is responsible for TDS and TCS compliance?

The persons responsible for making certain payments or transactions are businesses, professionals, and individuals. They are required to deduct or collect tax (as the case may be) and deposit it on time for compliance with the Income Tax Act.

10. Can I revise my TDS return after filing?

TDS returns can be revised if there are errors. It’s important to correct errors as soon as possible to avoid mismatches and penalties. Ebizfiling can assist in this and filing revised returns.

Don’t Miss the New TDS & TCS Updates

Learn the latest updates and file correctly under the revised tax provisions.

About Ebizfiling -

July 22, 2026 By Steffy A

Section 332 of the Income Tax Act 2025: NPO Registration Introduction Section 332 of the Income Tax Act 2025 provides the registration framework for eligible non-profit organizations in India. It applies to public trusts, registered societies, Section 8 companies, universities, […]

July 21, 2026 By Steffy A

Section 201 of the Income Tax Act 2025: Tax Rate & Eligibility Introduction Section 201 of the Income Tax Act 2025 provides a concessional tax regime for eligible domestic manufacturing companies. It allows qualifying companies to pay income tax at […]

July 21, 2026 By Steffy A

Section 397 of the Income Tax Act, 2025: Compliance and Reporting Introduction Section 397 of the Income Tax Act, 2025 lays down the main compliance and reporting requirements related to tax deducted at source and tax collected at source. It […]