-

August 3, 2026

-

BySteffy A

Form 10F Filing Without PAN for Non-Residents in India

Introduction

From 1 April 2026, Form 41 under the Income-tax Act, 2025 serves the purpose previously fulfilled by Form 10F for non-residents claiming DTAA benefits on income earned from India. Eligible taxpayers must submit the prescribed declaration along with a valid Tax Residency Certificate (TRC) to avail lower tax rates and avoid higher TDS. Non-residents without PAN can also file the form electronically through the Income Tax e-Filing Portal, subject to eligibility.

In this blog, we’ll explain what Form 10F Filing is, who needs to file it, how non-residents can file it without PAN, and how it helps in claiming DTAA benefits in India.

What is Form 10F Filing?

Non-residents who wish to claim benefits under tax treaties are required to submit their Tax Residency Certificate (TRC) along with a self-certified Form 10F. This form allows the non-residents to avail of the relief from TDS on income generated in India. As per the provisions of the Income Tax Act, 1961, non-residents can claim benefits of tax treaties only if they furnish a valid TRC. If the TRC does not contain all the necessary information, then the non-residents are required to file Form 10F.

Why is Form 10F Filing Important?

- Form 10F Filing helps non-residents claim DTAA Benefits India on income earned from India.

- It allows eligible taxpayers to avail lower TDS rates under applicable tax treaties.

- The form supports the Tax Residency Certificate (TRC) when all prescribed details are not available in the certificate.

- Filing the form helps avoid higher tax deductions and ensures compliance with Indian tax laws.

- It serves as documentary evidence of the taxpayer’s foreign tax residency status.

Information Required for Form 10F Filing

- PAN (where applicable under Indian tax laws)

- Nationality (for individuals) or country of incorporation/registration (for entities)

- Tax Identification Number (TIN) or equivalent tax identification number issued by the country of residence

- Period for which tax residency applies

- Residential or registered address in the country of residence

Can Form 10F Be Filed Without PAN?

Eligible non-residents who are not required to obtain a PAN in India can register on the Income Tax e-Filing Portal using the non-resident registration facility and submit Form 10F (or Form 41, where applicable) electronically. However, where a PAN is required under Indian tax laws, the taxpayer should provide the PAN while filing.

Basic details: Name, date of incorporation, tax identification number, and country of residence.

Key person details: Name, date of birth, tax identification number, and designation.

Contact details: Primary and secondary mobile numbers and email IDs, and postal address.

Attachments: ID proof, address proof, and a copy of your Tax Residency Certificate (TRC). The ID and address proofs must be valid documents in your country of residence.

On successful verification of these details, you will receive a user ID on your registered email ID, through which you can log in to the Income Tax Portal.

You can then upload Form 10F electronically after submitting your TRC and verifying it via OTPs.

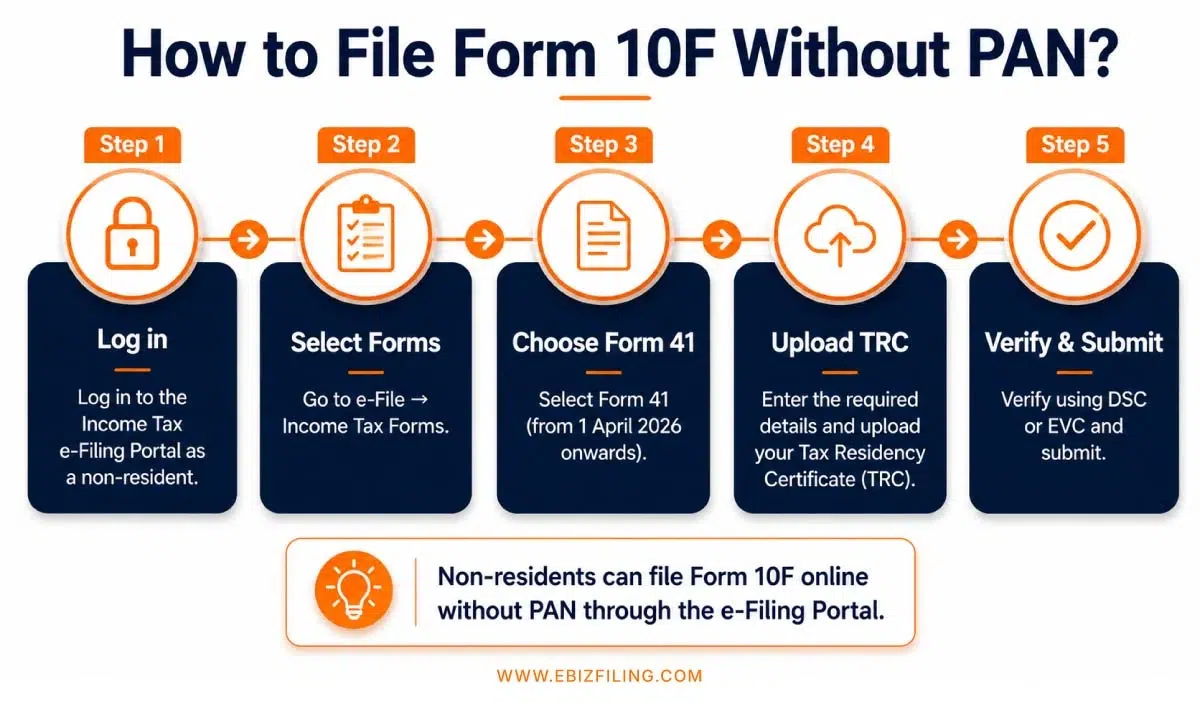

How to File Form 10F Without PAN?

Form 10F must be submitted through the Non-resident e-filing account on the income tax e-filing portal. The non-resident assessee (deductee) must submit the Form via the e-filing site by following the steps listed below.

- Visit the portal to access your income tax portal account.

- Select “Income Tax Forms” from the e-file tab, and then click “File Income Tax Forms.”

- In the drop-down menu, choose “Persons not dependent on any Source of Income (Source of Income is not essential)”

- For filings from 1 April 2026 onwards, select Form 41 under the Income-tax Act, 2025. For earlier periods where applicable, Form 10F may still be referenced under the previous law

- Click on “Continue” after selecting the relevant Assessment Year (AY) in the tab.

- The assessee would have to provide the necessary information and must also include a copy of the TRC (Tax Residence Certificate).

- According to Rule 131 of the IT Rules, It can be signed using either a digital signature (generally if the return of income is required to be provided under a digital signature) or an electronic verification code.

Form 41 Update Under the Income-tax Act, 2025

From 1 April 2026, Form 41 under the Income-tax Act 2025 serves the purpose previously fulfilled by Form 10F for claiming DTAA benefits. Non-residents claiming DTAA benefits should follow the updated filing requirements prescribed under the new law. While Form 10F was used under the earlier Income Tax Act, 1961, Form 41 now serves the same purpose of supporting treaty benefit claims by non-resident taxpayers. Form 41 can be filed online through the Income Tax e-Filing Portal under e-File then Income Tax Forms, and then Form 41. Non-residents registered without PAN can also access the filing facility through their Non-Resident User ID.

Form 10F Compliance Support by Ebizfiling

Ebizfiling helps non-residents and foreign entities complete Form 10F (now Form 41) filing accurately to claim DTAA benefits and avoid higher TDS deductions in India.

Services Provided by Ebizfiling :

- Form 10F / Form 41 Filing

- TRC Review & Verification

- DTAA Benefit Assistance

- Non-Resident Tax Compliance Support

- Income Tax Portal Registration Assistance

- Documentation Review & Filing Support

Need assistance with Form 10F Filing or Form 41 filing? Contact Ebizfiling’s experts for end-to-end support and timely compliance.

Conclusion

Form 10F Filing helps non-residents claim DTAA benefits and avoid higher TDS on income earned from India. By submitting the form along with a valid Tax Residency Certificate (TRC), eligible taxpayers can access treaty benefits and comply with Indian tax laws5, and non-residents should follow the updated filing requirements while claiming treaty benefits.

Frequently Asked Questions

1. Is Form 10F (or Form 41 from 1 April 2026) mandatory for claiming DTAA benefits in India?

Yes, non-residents seeking DTAA benefits must furnish a valid Tax Residency Certificate (TRC) and the prescribed declaration. For periods from 1 April 2026 onwards, Form 41 serves the purpose previously fulfilled by Form 10F.

2. What is the difference between Form 10F and a Tax Residency Certificate (TRC)?

A Tax Residency Certificate (TRC) is issued by the tax authority of the taxpayer’s country of residence. Form 10F is a self-declaration that provides additional information when certain prescribed details are not available in the TRC.

3. What happens if Form 10F is not filed?

If Form 10F is not submitted when required, the taxpayer may not be able to claim DTAA benefits. As a result, income earned from India may be subject to higher TDS rates under domestic tax provisions.

4. Can Ebizfiling help with Form 10F Filing for non-residents?

Yes, Ebizfiling assists non-residents, foreign companies, LLPs, and other overseas entities with Form 10F Filing requirements. Our team helps review the Tax Residency Certificate (TRC), prepare the required documentation, and guide taxpayers through the filing process to claim DTAA benefits in India.

5. Which types of income commonly require Form 10F Filing?

Form 10F is commonly required when non-residents receive royalty income, interest income, dividends, fees for technical services, consultancy fees, or other taxable income from India and wish to claim treaty benefits.

6. Can Form 10F Filing help reduce TDS in India?

Yes, Form 10F Filing supports a taxpayer’s claim for DTAA benefits. When submitted along with a valid TRC, it may allow the payer to apply the lower treaty tax rate instead of the higher domestic TDS rate.

7. Is a Tax Identification Number (TIN) mandatory for Form 10F Filing?

In most cases, taxpayers are required to provide a Tax Identification Number (TIN) or a similar identification number issued by their country of residence. This helps establish tax residency for treaty purposes.

8. What common mistakes does Ebizfiling help taxpayers avoid during Form 10F Filing?

Ebizfiling helps taxpayers avoid common filing errors such as submitting an incomplete Tax Residency Certificate (TRC), providing incorrect Tax Identification Number (TIN) details, selecting the wrong tax residency period, or missing required supporting documents. Correct filing helps ensure smoother processing and timely access to DTAA benefits.

9. Can NRIs receive income tax notices for not filing Form 10F?

Failure to furnish Form 10F when required may result in denial of DTAA benefits, application of higher tax withholding rates, or scrutiny during tax assessments. Non-residents claiming treaty benefits should ensure that Form 10F, along with a valid Tax Residency Certificate (TRC), is submitted correctly and within the applicable timelines. They should also comply with applicable NRI Income Tax Return Filing requirements in India to avoid unnecessary notices and tax disputes.

10. What instructions should taxpayers follow while filing Form 10F?

Taxpayers should ensure that the information provided in Form 10F matches the details mentioned in their Tax Residency Certificate (TRC). They should also verify their Tax Identification Number (TIN), residential address, nationality or country of incorporation, and the applicable tax residency period before submission. Any mismatch between Form 10F and supporting documents may lead to delays in claiming DTAA benefits or higher TDS deductions.

File Income Tax Returns

File your ITR with EbizFiling at INR 1199/- only.

About Ebizfiling -

Reviews

Ashrith Akkana

19 Apr 2022I took import export certificate from the ebizfiling. They have done the work on time.. Thank you for making my import export certificate in time 😊

Neeta Vakhariya

09 Mar 2018Delighted to work with them. Very efficient and hardworking staff.

Janvi Seth

14 May 2018I wanted to register my business on E-commerce and my colleague suggested me Ebizfiling. I am glad we made the right choice of choosing them.

August 11, 2026 By Steffy A

Section 156 of the Income Tax Act, 2025: Rebate Rules and Limits Introduction Section 156 of the Income Tax Act, 2025 provides an income tax rebate for resident individuals who satisfy the prescribed income conditions. The provision applies from 1 […]

August 10, 2026 By Steffy A

Form 140 Filing: Due Dates, Documents and Process Introduction Form 140 filing is a quarterly TDS compliance requirement for persons who deduct tax from specified non-salary payments made to resident deductees. Form No. 140 replaces Form No. 26Q under the […]

August 7, 2026 By Steffy A

Section 140 of the Income Tax Act, 2025: Startup Deduction Introduction Section 140 of the Income Tax Act, 2025 allows eligible startups to claim a 100% deduction on profits from their eligible business for three consecutive tax years within the […]